A group of investors who lost most of the money they had invested in structured products issued by Deutsche Bank and linked to Portugal Telecom credit have collaborated to produce a press release, announcing that they had approached Macedo Vitorino & Associados to represent them in a suit against the German bank. Their claim is two-pronged: the notes were sold as capital guaranteed, and a material change had taken place when the underlying was changed when Oi, a Brazilian company acquired PT.

"Deutsche Bank is aware of some comments in the press about these possible claims but has not received any official claim in respect to this product," said Nuno Almeida-Leal, head of product management, Deutsche Bank Portugal. "In our opinion, it is the fact that the risk is 100% linked to Portugal Telecom and the amount of the loss that has affected such a well-known name in the market, what has created so much [media] attention with regards to this specific issue," said Leal.

No lawsuit has been filed, according to Rita Carvalho, head of public relations & communications at Macedo Vitorino & Associados. "It seems premature to say that the matter will lead to lawsuits. In other cases, our advice was for clients to discuss a settlement with the banks involved and to seek the intervention of regulators when appropriate. It is not possible to determine the amount of the damages at this point."

Oi filed for bankruptcy in June, which was determined as a credit event by the International Swaps and Derivatives Association (Isda) on June 21, 2016. The investors said that Deutsche returned only 12.56% of the capital from the db Rendimento Portugal Telecom Finance 2020 income notes they had bought.

The company had a huge amount of debt that was only increasing year by year, according to analysts. "From 2011 to 2016, the debt-to-equity ratio grew from 38.5% to 415.5%, where the industry ratio in 2016 is around 140.43%, so Oi had a ratio three times bigger," said Artur Patricio, sales and derivatives analyst in Caixa Geral de Depositos. "The second major concern that affected the deal was the default of Rio Forte bonds of which PT held about €900m. This default by Rio Forte was the deal breaker between PT and Oi."

Altice showed an interest in buying part of the operation of PT in 2004, and part of the debt of PT was out of this deal between Oi and Altice as well as the default bond of Rio Forte, which was transferred to a vehicle (called Pharol and quoted in the PSI 20 local equity index) that was created and held those debts, part of which were transferred to the Oi balance sheet, further increasing the debt of Oi. Most of the credit-linked notes that were issued by banks included these bonds as collateral that were transferred to Oi balance sheet, according to Patricio.

"The issuers that have credit-linked notes with 100% capital guarantee will have to reimburse the holders, at least paying them the par amount, especially if we are talking about deposits," said Patricio "When the issuers did their hedging after selling such products, they should have accounted for such possibilities, or at least rebalanced their hedges after all the events between PT and Oi. Clients bought something that clearly states they would receive at least their capital back at the end of the period, regardless of what happen to the underlings."

The product from Deutsche is a typical capital-at-risk credit-linked note, with flip flop coupons offering 4.5% fixed per annum for the first year and a floating coupon linked to three-month Euribor, with a cap at 5.5%. "The notes are a special purpose vehicle (SPV) which has a Portugal Telecom bond as collateral and a fixed-to-floater swap to change the payoff from fixed- to variable rate," said Leal. "They were classified as risk 4 out of 9 for levels of complexity and risk 5 out of 5 for levels of risk, due to the fact that the issue had a long maturity and that Portugal Telecom was classified below investment grade at the time of the issue," he said.

The product was first launched in August 2013, when the Portuguese Telecom was one of the most valuable and liquid Portuguese incumbents, according to Leal. "There was a lot of demand for the name in the market, as was the case for EDP, Galp, REN, etc. as investors were looking to lock-in spread on good quality Portuguese corporates.

"The main issue with this specific product is that the risk is 100% related to Portugal Telecom. As such, with the credit event announced, investors faced an unwind of the SPV and a loss of approximately 88%. This is the result of the sale of collateral and unwind of the fixed to floater swap," said Leal.

The SPV was unwound and the proceeds were paid back to the clients on the August 3, according to Leal. "From the bank's perspective there is little that can be done given the tremendous loss caused by the restructuring process of Oi, although the bank will naturally continue to follow this issue closely and to provide any assistance necessary to its affected clients," said Leal.

"Most investors don't understand credit-linked notes, especially those that have bought those instruments over the counter," said Patricio. "There are two main types of investor: qualified investors and, let's say, normal investors (those that usually invest their money in deposits or certificates). The qualified investors clearly understand those investments and know how to take advantage of them. However, normal investors, who don't have much experience of investing, often buy instruments they don't understand, which is the main reason for the crisis in the first place."

The marketing brochures are quite clear about capital being returned, according to local bankers. "I don't know how the product was sold, but I don't really believe that people read these brochures," said the local banker. "For instance, you go to buy a telephone, but you do not read everything that you sign. The same is true for structured products. You can always say that you do not understand." Leal disagreed: "The documentation provided by Deutsche Bank for this product was completely transparent, which was reflected in the key investor information document (KIID), and explained, in detail, when the notes could be redeemed early, including in case of a credit event.

"A dedicated section [...] disclosed to investors a set of scenarios, including the worst scenario possible, in what it was mentioned a total loss of capital and remuneration," said Leal. "In relation to the change of debt ownership, Deutsche Bank was not involved in any of the transactions and the only thing it could do was to reflect these corporate actions as they appeared, which the bank did of course," said Leal.

Deutsche Bank did not produce any marketing materials apart from those approved by the local regulator (Local KIID) and the approval of the issue for public distribution in Portugal was conducted in the same manner as all other issues the bank put in the market and "all the required disclosures and disclaimers were adequately made", according to Leal. "The bank placed this product in line with local procedures established by law and regulation, nothing unusual in this regard."

The effect on the investment market in Portugal is bigger than usual, despite the high number of defaults in such a small market, according to Patricio. "The Portuguese market saw BPN bank collapse, then BPP (a smaller bank), then BES, then Banif and, later, the transfer of the senior bonds of Novo Banco to the bad bank that was created to absorb the bad assets of BES."

When markets are going up, investors are usually aggressive, understand the market and know all the risks without any expectations that the markets will turn, according to the local banker. "Each person has a profile," said the local banker. "It would be better if people stick more to their profile. If I am conservative, if I want to put someone into an aggressive portfolio, I will just put a bit of it in more risk assets, not everything just because the market is going up."

The amount of PT-linked structured products issued in the last three years amounts to $1,740m, 79% of which was sold in Portugal, 18.5% in Spain and the remaining 2% in the DACH region (Germany, Austria and Switzerland), Finland, Italy and Belgium: 67% of the products are wrapped as notes with the rest divided between structured deposits and funds; $166m of the products still live are capital protected, $41m are partially protection and $464m are not protected, according to SRP data.

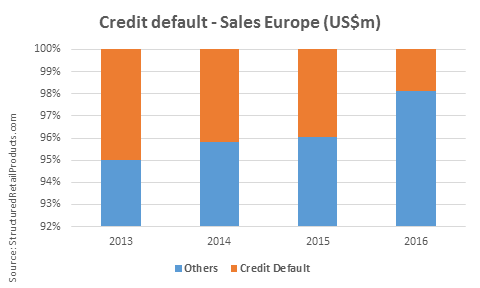

Since 2013, there was a decline in the sales volume of credit-linked products in Europe, from $4,840m in 2013, to $3,973m in 2015, according to SRP data.

BaFin moves to ban retail distribution of CLNs

Cashed up Asian private banks prepared to offer leveraged CLNs

DB staffers under investigation for buying CLNs to hedge bank's own balance sheet