Firms like UBS, Bank of America (BofA) and JP Morgan have incentives to shave the returns on their indexes so that payments these firms make under the structured products they issued are reduced at maturity, according to a study released on Friday by Securities Litigation and Consulting Group (SLCG).

The study, Structured Products and the Mischief of Self Indexing, written by Craig McCann (pictured) and Mike Yan principals at SLCG, and Geng Deng, formerly of SLCG and currently a vice president at Wells Fargo, points at the increasing use of indexes created by brokerage firms to determine payoffs to structured products.

The SLCG report traces the evolution of structured products from their origin as a source of financing for operating companies in the 1980s to a source of riskless profits for brokerage firms. According to the report, brokerage firms now issue structured products linked to indexes they create rather than linked to independent indexes from independent index providers such as Standard & Poor's. SLCG illustrates the potential conflicts of interest created by proprietary volatility indexes although the conflicts are present in other proprietary index based investments as well.

'Issuing and underwriting structured products linked to proprietary indexes has led investment banks to mischief,' stated the study.

In the late 1980s and early 1990s, equity-linked notes were issued by operating companies in financial distress, according to the study. 'Early equity-linked notes were also used by corporations and wealthy investors to "monetize" highly appreciated stock positions, shedding risk and deferring taxes,' stated the research. 'Later in the 1990s, investment banks switched from underwriting reverse convertibles and tracking securities issued by operating companies like Citicorp and Reynolds Metals Linked to their own stock to issuing and underwriting structured products linked to unrelated publicly traded companies.'

The study also highlights that this change in the role of investment banks led to a dramatic proliferation of new structured product issuances and 'ever more complicated payoff structures' since the investment banks were no longer limited to underwriting securities other companies wanted to issue.

According to Dr Mike Yan, one of the authors of the report, recent US Securities & Exchange Commission (SEC) settlements with UBS over its V10 Currency Index and with Bank of America over its VOL Index reflect awareness of the harm caused to investors by self-indexing.

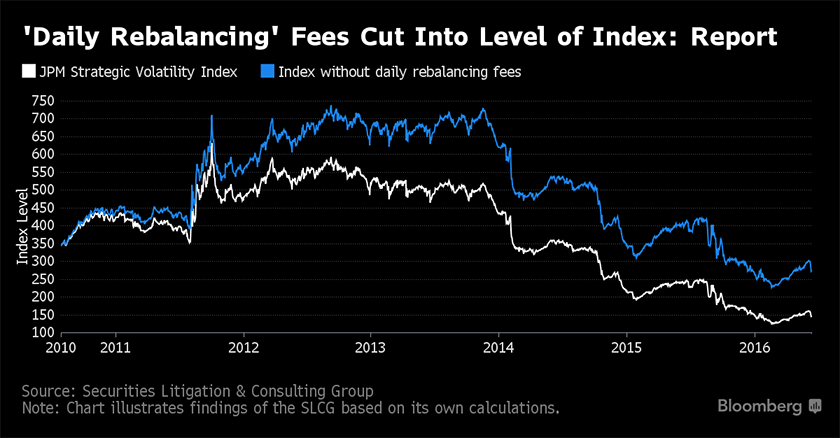

'UBS and Bank of America were not the only firms that built phantom "trading costs" into their indexes - trading costs not built into the Standard and Poor's indexes other brokerage firms use to determine their structured products' payoffs,' Dr. Craig McCann pointed out. 'JP Morgan's Strat VOL related structured products is another example of the spurious complexity firms build into these indexes making regulatory oversight more difficult and allowing issuers to deceptively sell structured products.'

The report also states that because the way these proprietary indexes were calculated banks were able to lower the amounts they would have to pay out to investors of its structured products, and because the products linked to those indexes were issued before the SEC began requiring issue date fair value disclosures and so it was also virtually impossible for investors to know that structured products linked ot those indexes were worth less than alternatives from other providers.

'When brokerage firms include hypothetical trading costs in their proprietary indices - costs that are absent from third-party indices - they make comparison of disclosed costs at the structured product level uninformative,' concluded the study. 'Even when issuers are required to report issue date values, those values are uninformative if the issuer can value a structured product based on an index that includes significant hypothetical costs but assume for purposes of calculating an estimated value that the index was going to be calculated with no trading costs thereby significantly inflating the value of the structured product.'

This mischief, however, would not have been possible if issuers linked to indexes provided by third-party vendors who had no interest in the payoffs from structured products linked to their indexes, according to the research.

UBS and JP Morgan declined to comment. BofA did not return calls requesting comment by press time.

Click in the link to download a PDF of the study.

UBS hit by US$15m SEC fine involving sale of rev convs to retail investors

US state regulators include SPs in top enforcement targets

Finra to examine suitability obligations and sales practices