Sales and issuance of structured products in the four Nordic markets showed contrasting fortunes during the first nine months of 2017, according to SRP data. While volumes in Sweden were down 24% compared to the same period in 2016, sales in Denmark, Norway and Finland increased by 53%, 23% and 2%, respectively. When it came to issuance, Denmark, with an increase of 31% and Norway, with a 7% increase, showed signs of recovery while the number of newly issued products in both Sweden and Finland was 20% down on the first nine months of 2016.

SRP reviews the data and the financial results of the top five structured products manufacturers in the Nordics.

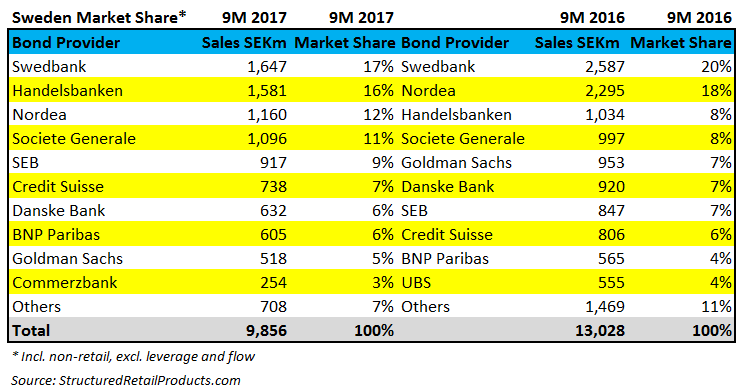

Swedbank was only active in the Swedish market where the bank was the number one provider with a share of 17% of the market in the first nine months of 2017. The bank sold 83 structured products worth SEK1.6bn (€169m) between January 1 and September 30, 2017, down from 105 products with combined sales of SEK2.6bn during the same period last year, according to SRP data. To put in perspective how much sales volumes have fallen in Sweden: five years ago, during the first nine months of 2012, Swedbank issued 135 products with a sales volume of SEK5.2bn, a decrease of almost 70% compared to the same period in 2017.

The vast majority of Swedbank's products in 9M2017 were linked to equities (77), including 43 products linked to a share basket; 26 were linked to a single index; and eight to an index basket. The remaining products were linked to foreign exchange rates and credit (three products each). Swedbank's best-selling product during the period was Spax Världen Max 716B, a seven-year capital protected note linked to a basket of 18 shares which sold SEK110.9m during the investment period.

As at September 30, 2017, Swedbank had SEK911.8bn debt securities in issue, including SEK14.7bn worth of structured retail bonds, according to the bank's interim report.

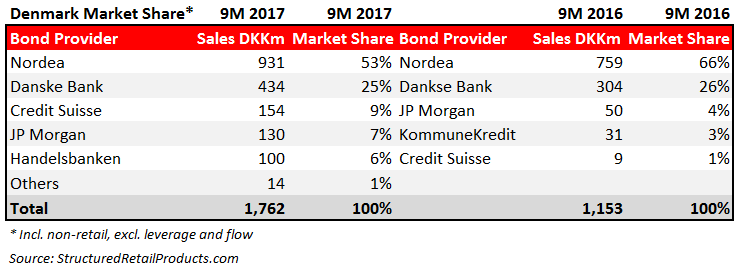

Nordea was the only manufacturer of structured products active in all four Nordic markets during 9M2017, according to SRP data. Nordea's sales were down across Sweden and Finland, although both Denmark and Norway recorded an increase in volumes. In Sweden the bank issued 36 structured products worth a combined SEK1.2bn during the first nine months of 2017, down from 52 products with a sales volume of SEK2.3bn in the same period last year while in Finland Nordea aggregated sales of €35m from 12 products (9M 2016: €82m from 24 products). In Denmark sales, at DKK931m (€125m) - from six products - were up 23% on last year (9M 2016: DKK759m from nine products) and in Norway, 16 products worth NOK359m (€25m) were sold during the first nine months of 2017 (9M 2016: NOK321m from 15 products).

Nordea reported €183bn debt securities in issue at the end of the third quarter of 2017, down from €191bn at the end of 3Q2016. The bank issued €3bn in long-term funding in the third quarter (excluding Danish covered bonds and subordinated notes), of which approximately €900m represented issuance of covered bonds from Nordea Hypotek while a €2bn dual tranche (four-year and 10-year tenor) senior unsecured bond was issued from Nordea Bank AB during the third quarter. The long-term funding portion of total funding was approximately 81% at the end of September, according to the bank.

'Despite increasing geopolitical risks and imbalances in the economy, we continue to see synchronised growth in our home markets,' said Casper von Koskull (pictured), CEO, Nordea. 'Margins remain stable, although we have not seen the usual pick-up in demand for corporate advisory services after the summer. Costs developed according to plan and credit quality improved as expected.'

Handelsbanken was active in Sweden and Denmark during the first nine months of 2017. In Sweden, the bank issued 66 structured products worth SEK1.6bn - distributed, among other, via Erik Penser, Garantum, Skandia and Strukturinvest - which translated in a 16% share of the market (against 43 products and SEK1bn in 9M2016). In Finland, year-on-year sales were also down, with €3m collected from four products (compared to four products and €9m in the first semester of last year) while in Denmark the bank was the issuing party for one product which sold DKK100m.

Handelsbanken reported net savings in Sweden in its mutual funds amounted to SEK16.1bn during the first three quarters of 2017, corresponding to a market share of 13.7%. Net savings in the bank's mutual funds elsewhere in the Nordic region were SEK5.4bn in the same period. Total net savings in the group's funds amounted to SEK15bn. The total fund volume, including exchange-traded funds (ETFs), increased by 14% from the beginning of the year to SEK485bn (9M 2016: SEK425bn) while total assets under management (AUM) rose during the same period by 11% to SEK599bn (9M 2016: SEK542bn), according to the bank's interim report.

SEB was the fifth most active issuer in Sweden and the joint most active in Finland (together with Danske Bank) during the first nine months of 2017, which translated in a market share of 9% in Sweden and 25% in Finland. The bank did not issue structured products in both Denmark and Norway. In Sweden, SEB issued 58 structured products worth SEK917m (compared to 85 products and SEK847m in 9M2016), with the distributors including Erik Penser, Garantum, Länsförsäkringar Bank, Skandia and Strukturinvest.

In Finland, SEB sold 38 products (€115m) via Alexandria, FIM Pankki, SP Kapitaali and UB Omaisuudenhoito, against 37 products and €72m during the first nine months of 2016. The bank's best-selling structure in Finland was SEB Pankki Kuponki, a five-year MTN linked to the Eurostoxx Banks index which sold €24.8m.

For the third quarter, the effect from structured products offered to the public was approximately SEK205m (compared to SEK195m in the second quarter and SEK510m in the third quarter of 2016) in equity related derivatives and a corresponding effect in debt related derivatives of minus SEK75m (2Q2017: -SEK95m, 3Q 2016: -SEK395m), according to the bank. At the end of September 2017 the total outstanding amount for debt securities issued stood at SEK659.4bn compared to SEK668.8bn at the end of June 2017 and SEK705bn at the end of September 2016.

Danske Bank issued structured products in Finland, Sweden and Denmark in the first nine months of 2017. In Finland, the bank shared top spot with SEB as the main provider of structured products, acquiring a share of 25% of the market (€115m) from 46 products which were distributed via Alexandria, Evli, FIM and UB (9M2016: €140m from 60 products). In Sweden the bank was the issuing party behind 39 products (SEK632m) which were distributed via Erik Penser, Garantum and Strukturinvest (9M2016: SEK920m from 44 products).

In its domestic market Denmark, Danske's sales volumes increased by almost 43% in 9M2017. The bank sold nine structured products worth DKK434m (€58m) in the first nine months of the year compared to four products with combined sales of DKK304m during the same period in 2016.

Danske reported trading portfolio assets and trading portfolio liabilities increased from net assets of DKK31.4bn at the end of 2016 to net assets of DKK59.1bn at the end of September 2017 as a result of fluctuations in the market value of the derivatives portfolio. In the first nine months of 2017, issuance of covered bonds, senior bonds and additional tier 1 capital totalled DKK47bn. Due to higher-than-expected deposit inflows, the expected funding need was lowered from DKK70-90bn to DKK 55-70bn, according to the bank.

Click the link to view the full interim report 2017 for Danske Bank, Handelsbanken, Nordea, SEB and Swedbank.

Related stories:

Sweden structured products market needs to suggest Q&A for Mops, SRP Nordics

Having good savings is very important in today's society, SRP Nordics

The Nordic market can learn from the rest of the regions, SRP Nordics