Australian banks have reported increasing net income and profit for their 2017 activities on the back of strong wealth management performance.

ANZ announced that its profit after tax for the full year that ended on September 30, 2017 was A$6.41bn (US$5.02bn), up 12% from A$5.7bn as compared to the same period last year. Additionally, the bank's cash profit reached A$6.94bn, up 18% from A$5.9bn on an annual basis. ANZ's common equity tier 1 capital ratio was 10.6% up 96 basis points. Return on equity increased 159 basic points to 11.9% with cash earnings per share up 17% to 237.1 cents.

The bank's full year operating income went down 1% on an annual basis from A$20.5bn to A$20.2bn. ANZ's net interest also decreased 1% from A$15bn to A$14.8bn.

Additionally, the Group announced that it had agreed to sell its retail and wealth businesses in Singapore, Hong Kong, China, Taiwan and Indonesia to Singapore's DBS Bank. As a result of the sale agreement, the group recognised a $324m charge to software, goodwill and fixed assets as well as providing for costs associated with the sale with a $14 million gain recognised in relation to the sale. 'The remaining businesses in Taiwan and Indonesia will transition in early 2018,' said the bank, in a statement. 'The transfer of Vietnam Retail to Shinhan Bank Vietnam will also be completed in early 2018.'

Macquarie Group reported net operating income of A$5.4bn for the half year that ended on September 20, 2017, indicating an increase of 3% from A$5.2bn as compared to the same period last year. Net operating expenses, on the other hand, went down 1% to A$3.6bn. Profit attributable to ordinary equity holders went up 19% on an annual basis, from A$1.05bn to A$1.25bn.

Macquarie Asset Management, Corporate and Asset Finance and Banking and Financial Services generated a combined net profit contribution for the half-year that ended on September 30, 2017 of $A2.1bn, up 28% on the prior corresponding period. The group's revenue from its asset and wealth management was A$1.7bn, 22% of total revenue from external customers.

For the period between January 1 and December 31, 2017, Macquarie Group issued a total of six structured products worth A$42m.

National Australia Bank saw an increase of 2.7% in net operating income, from A$17.4bn to A$17.9bn. Also, net interest income saw an increase of 1.8%, from A$12.9bn to A$13.2bn. Operating expenses went up 2.6% on an annual basis, from A$7.4bn to A$7.6bn. The group's net profit decreased 3.8%, from A$6.4bn to A$6.2bn. Cash earnings, on the other hand, went up 2.5%, from A$6.4bn to A$6.6bn.

The group's net profit from its consumer banking and wealth business increased 4.3%, from A$1.56bn to A$1.6bn. Additionally, net operating income of the consumer banking and wealth reached A$5.4bn, up 2.1% as compared to the same period last year.

Westpac reported net profit of A$7.9bn for the full year that ended on September 30, 2017, up 7% from A$7.4bn in the previous period. Net interest income was A$15.5bn, up 2% from A$15.1bn in 2016. Similarly, the group's non-interest income went up from A$5.8bn to A$6.3bn, indicating an increase of 8% on an annual basis, 'due to a A$279m gain associated with the sale of shares in BT Investment Management Limited (BTIM), a rise in trading income of A$78m and the impact of volatility in economic hedges of A$140m.' 'These increases were partly offset by provisions for customer refunds and payments and lower wealth management income,' was said in a statement. Operating expenses increased 2%, from A$9.2bn in teh 2016 financial year to A$9.4bn in the last financial year.

In 2017, Asic released a number of regulatory reports with the goal of improving the work of the industry. In April, Asic published a report of its review on financial advice in Australia, identified a number of potential deficiencies with regard to monitoring and dealing with non-compliant investment and financial advice in the country. The review targeted Australia's top five financial advisory institutions, including AMP, ANZ, CBA, NAB and Westpac, and is aimed at lifting standards and processes.

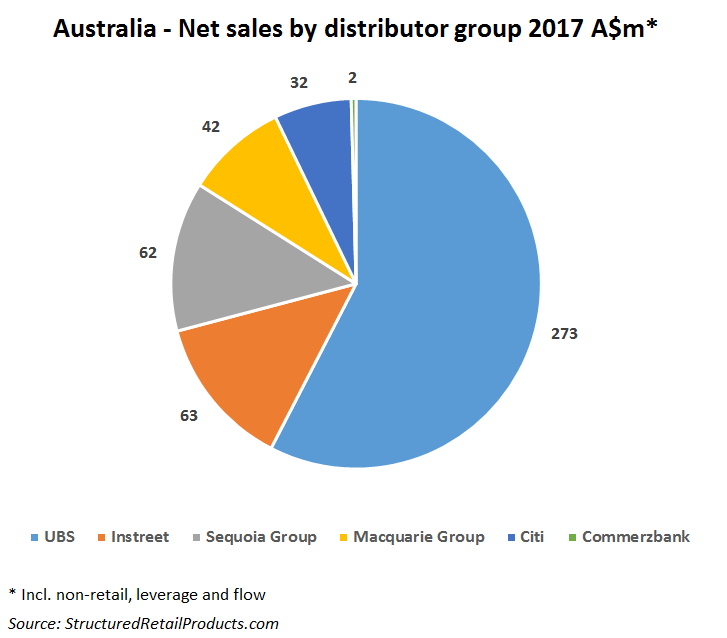

In the domestic structured products market, year-to-date, total net estimated sales on the market for structured products in Australia decreased by 52% compared to the same period in 2016 and by 70% compared to 2015.

UBS remains the leader, with net sales of A$274m in 2017, year-to-date, down 21.9% on the year. Compared to 2016, Instreet and Sequoia Group were the only distributors in Australia with increasing net sales, of 21% and 78%, respectively. The net sales of Macquarie remained unchanged, while Citi's net sales decreased drastically by 93%, year-on-year.

Click in the links to access the quarterly reports: ANZ, Macquarie Group, NAB, Westpac.

Related stories:

Tribunal upholds Asic ban on Credit Suisse banker for trading in 'mini' warrants

We offer a greater range of warrant types than our competitors, Citi

The focus is on growing AUM not on proliferation of products, ASX