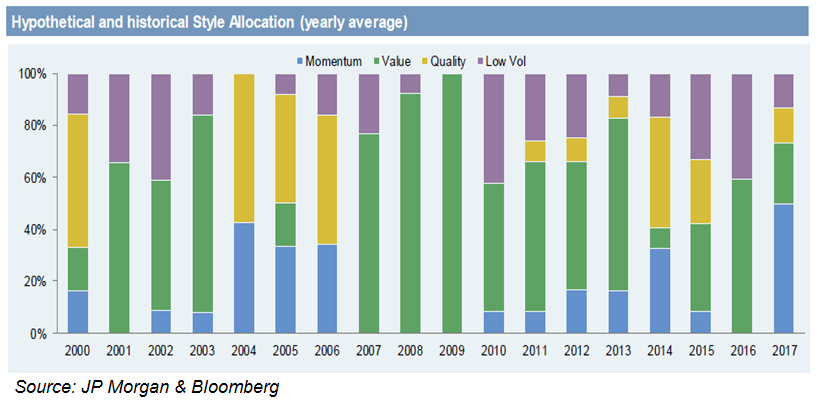

2017 was the year of the momentum, according to allocation data of the S&P Economic Cycle Factor Rotator Index (Rotator index). The index, jointly developed by S&P Dow Jones Indices and JPMorgan, was launched in August 2016 and aims to help investors avoid the hustle and bustle of moving their funds from one style to another as economic sentiment changes. There is a single risk-controlled index dedicated to each of the four strategies - momentum, value, quality, and low volatility - but all indices are bundled under the roof of the Rotator index.

"Working with S&P means that we can use their breadth of indices to construct innovative strategies, in this particular example, four S&P style indices," said Julien Chuard (pictured), executive director, responsible for investible indices in JP Morgan's equity derivatives structuring team. A healthy share of fixed income, represented by the S&P 5-Year US Treasury Note Futures Excess Return Index, and cash is also thrown into the portfolio mix.

As an investment vehicle based on a dynamic allocation, the Rotator index aims at both a performance, superior to that of larger US equity benchmarks on a risk-adjusted basis, and an efficient allocation between equity, fixed income, and cash assets depending on prevailing market uncertainty, Chuard explained. "Thanks to its style rotation feature [...], the index is well positioned to capture US equity upside, while providing principal protection in a note or certificate of deposit (CD) wrapper." The trigger of the rebalancing between momentum, value, quality and low-volatility/high-dividend styles are the signals for economic activity from the Chicago Fed National Activity Index (CFNAI), which is comprised as a weighted average of 85 monthly US economic indicators.

Expansionary and recovery phases correspond to momentum and value investing, while economic slow-down and contraction drive funds towards quality and low volatility stocks. Seeing as the S&P 500's fear indicator - the Vix index - showed confidence in equity throughout all of 2017 and dropped to an all-time low in November, two thirds of the year the Rotator spent in the "growth" department, yielding a return of 11% by year-end. According to JP Morgan, this trend was cultivated on a background of accelerating global growth and reflationary macroeconomic data.

"The boost in the US stock market since Donald Trump's election for president in November 2016 was sustained by strong corporate earnings over the past year and further fueled by the business-friendly tax reform promoted by the Trump administration," said Chuard. That added up to the superior performance of the growth styles over low-volatility/high-dividend, which are more prone to monetary policy vehicles, such as interest rates. "Changes in accounting policies and corporate governance, and innovation processes could also affect style rotation," he added.

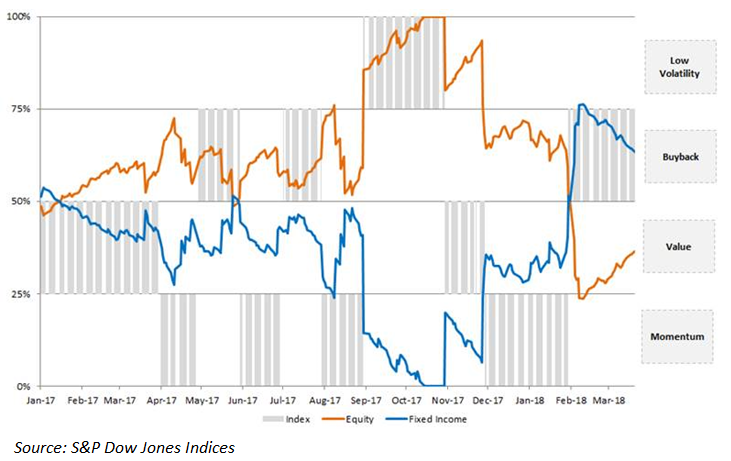

Indeed, after Fed's rate hike in December and the return of volatility early February, the index had to adapt to the new, riskier conditions. The fixed income share rose to 75%, while equity was shifted from momentum to buyback (quality) stocks. This strategy was carried on in March with the equity-bond ratio rebalancing to approximately 35% to 65% (there was no cash investment).

Joseph Kairen, senior director, strategy and volatility indices at S&P Dow Jones Indices explained, "the same pattern we saw in early February can be observed with all strategies, but there is still difference in the severity of shift from stocks to fixed income", with low-volatility exhibiting the largest jump from equity to fixed income since year-end 2017.

So far, there are 34 live structured products linked to the performance of the Rotator index, added to SRP database since the index's inception. Except for the internationally offered index-linked certificate with a tracker structure and a digital payout scheme at maturity (XS1569773572), the remainder of the products are all fully capital-protected and aimed at US investors.

Fourteen certificates offer an overproportional participation in the final performance of the index through an enhanced tracker payoff; 18 certificates have an autocallable feature that gives an early redemption opportunity at rising index levels over the course of the investment; and one product combines both.

"Thanks to its 6% risk control, buying optionality on the index is inexpensive and allows investors to leverage their exposure on the upside. [The product] is then generally packaged into notes or certificate of deposits," said Chuard, adding that the index has also traded as a warrant and over-the-counter call option. "So far, we have traded the index well in both the US and Asia, and are starting to get good traction with our European clients as well."

For 2018, JP Morgan intends "to quantify the ability of the signal to pick the right style depending on the economic environment", said Michael Wilson, head of Emea equity sales, JP Morgan. "Over the past three years, the signal picked the best performer among factors 40% of the time, and either the best or the second best 64% of the time."

Wilson expects the factor leadership to change frequently in 2018 as the tax-reform induced style rotation is "unlikely to go smoothly" and with volatility returning, "there is a strong case for the Rotator index with its 6% volatility target to prevent against drawdowns".

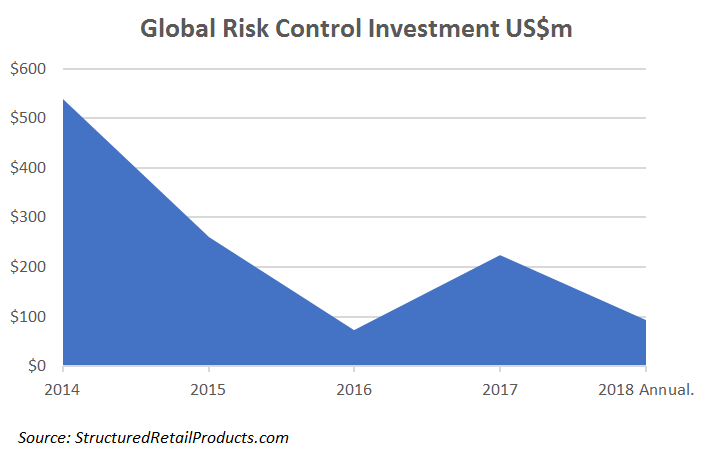

Since 2014, there were 209 products based on risk-controlled strategies that were added to SRP's global database. Until 2017, estimate sales volume of target-volatility investments has more than halved to approximately US$220m.

Related stories:

JP Morgan strengthens German footprint via turbo warrants

Index roundup: Kospi 200 gets momentum, JP Morgan readies Gabi series

Product wrap: JP Morgan targets Dach region with ETF-linked rev conv