Equity markets were down last year, and suffered the worst downward run in five years.

The first half of the year was positive for the structured product industry as everyone thought that the markets were going to recover and investors would benefit from the extra yield resulting from the higher volatility, something that happened in the second half.

Against a backdrop of positive economic growth, most distributors increased their exposure to the US market through structured products, with sales reaching a total US$334 billion outstanding only on products linked to the S&P500 index, according to SRP data.

Nevertheless, with signs of a global economic slowdown, concerns about monetary policy and political dysfunction led to an increase in volatility making December a particularly dreadful month, with the S&P 500 falling 9%.

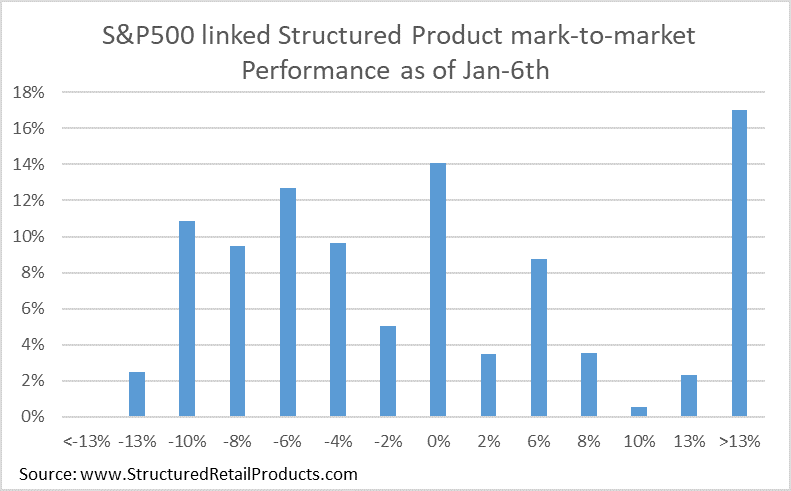

According to our analysis of 26,410 live structured products, from which 50% had the initial strike during 2018 and were out of the money, 32% of the products are still on track to deliver an annualised average return above 6%, providing that the S&P500 does not decline further.

Buffer kicks-in

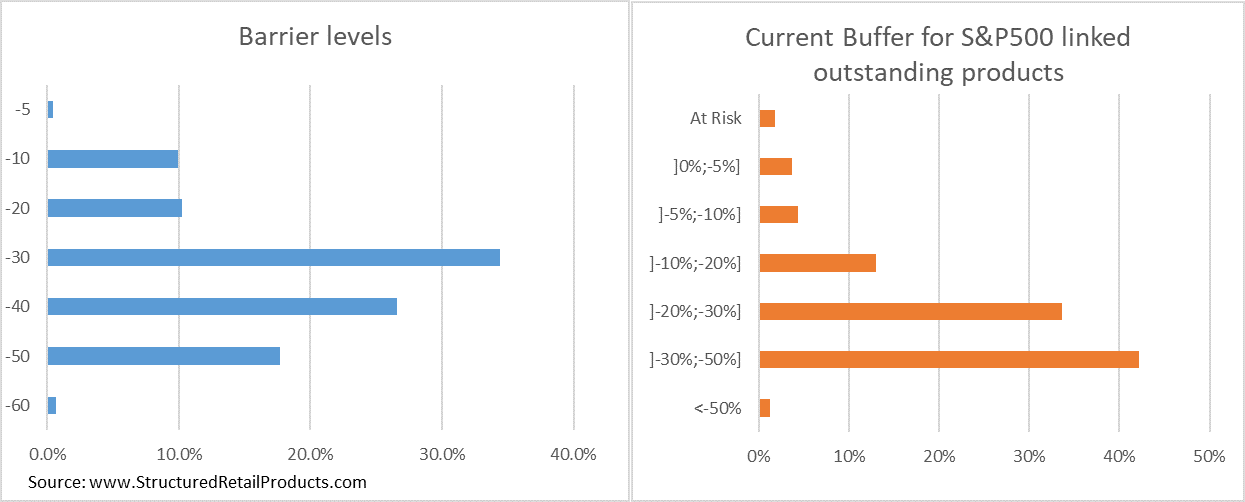

Yet, most structured products have soft protection, which means that although their mark-to-market is highly correlated with the underlying performance, the capital is protected at maturity as long the underlying does not depreciate more than a predefined level, known as the barrier.

According to SRP data, 72% of the products linked to the S&P 500 have an average 35% downside barrier level, which has to be breached before investors lose capital, i.e., the S&P 500 will need to reach 2,000 points, before most products start to have a negative performance.

An interesting statistic is that although most investors lost capital in 2018, only 2% of the current investors on structured notes linked to the S&P500 are at risk of losing capital, and that will only happen if the S&P500 falls an extra 20%, for 23% of the products put capital at risk, according to SRP data.

Last, but not least, autocallables linked to this underlying which represent 36% of the current live products, are now 8% below their knock out strike level. This will make 2019 a more difficult year for the structured product industry as these products will only expire earlier if the S&P 500 rises a further 8%.

Although the current outlook does not seem positive, as long the S&P500 keeps above the 2,500 level, there will be a high number of structured products maturing and returning a positive coupon as the average strike level of the outstanding structured products linked to the American stock market index, is currently at 2,490.