Common asset allocation strategies typically splits the investment portfolio into different asset classes, based on theory behind, following Harry Markowitz’s Modern Portfolio Theory stating that, because of asset correlations, portfolio risk, or standard deviation, was lower than that calculated by a weighted sum.

But why would stop here?

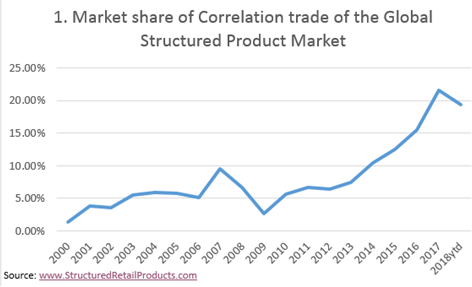

According to SRP data, correlation trades, which accounted for less than 5% of structured products sold before 2004, ended 2017 with a 22% share of the global market.

The main reason that issuers adopt these strategies lies with the difficulty in structuring attractive products while interest rates remain low: if you offer the performance of the worst performing underlying asset versus a basket, a higher potential coupon or higher participation can be achieved.

Logically, these products should produce the same average performance as the baskets they link to. However, the performance of these correlation trades has been better than the non-correlation products, according to SRP data.

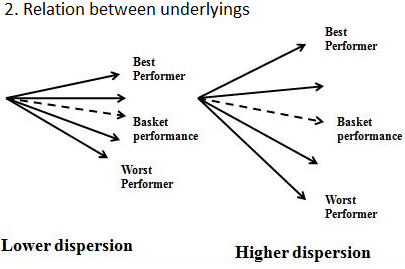

These products capitalise on the pricing of correlation options, such as worst-ofs, in relation to basket options.

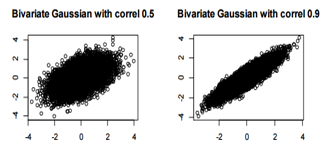

The higher dispersion leads to a lower payoff for the call option on the worst performing stock. Since lower correlation leads to highly dispersed returns on the underlying assets, lower correlations would lead to lower payoffs for worst-of call options.

As most of these products have been using equity indices with correlations above 0.7, investors have been increasing their coupons and participations with a limited reduction in the probability of getting a positive return.

So, if you’re taking your portfolio to the next step in the world of correlation, the most important consideration is to decide the correlation level risk you are willing to accept, knowing that you will increase your returns against a higher risk, if correlation between the assets decreases.