Risk premia, factor index and multi-asset allocation are soaring, as the global economy transitions from the recovery cycle and investors adopt increasingly diverse and niche exposure requirements, according to panelists on the 'Creating the Right Investment Strategies' panel at SRP's Third Annual Nordic Structured Products & Derivatives Conference 2017, held in The Grand Hotel in Stockholm on September 27.

Factor investing is not new, but over the past five years, investors have looked to gain exposure through indices, driving a pluralisation of factor strategies, according to Hitendra Varsani (pictured), executive director at MSCI. "Our factor indices have around US$190bn in assets under management, which compares with some $30bn four to five years ago," said Varsani. "We expect the increase to continue at a very high rate."

Nico Langedijk, regional director, Switzerland, Scandinavia and The Netherlands at Stoxx, said that the bulk of indices his company has been developing are theme-based and topical. "The proliferation and increasing granularity of indices on a global scale is driven by demand for equity diversification."

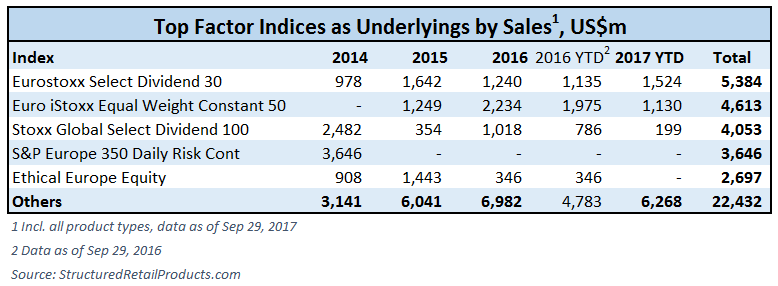

The sales of products based on factor indices more than doubled between 2014-2016, with a 30% increase in sales of factor index-based products this year, despite the number of indices used falling to 91, from 99 for the same period last year.

One of the main issues has been the capacity for banks to price these various and increasingly granular solutions, according to Richard Darville, head of structuring & trading at Exceed. "There has been a kind of Catch 22, where distributors were searching for some exposure, but minimum volume requirements have been getting in the way," said Darville.

There is a clear distinction between capital-protected and non-protected solutions, which has created different dynamics in factor-based structured products, according to Christophe Mignard, head of UK equity pricing and solutions at Societe Generale. Index construction needs to cater to low interest rates and provide for more friendly pricing conditions, offering leeway for additional filters like low volatility and higher dividend, according to Mignard.

For non-protected products, there is less appetite for anything that steps away from mainstream indexation, he noted. Notably, most implied parameters linked to the Eurostoxx 50, like implied volatility and dividend forecasts, have been massively stressed, with volatility low and dividend futures sloping downwards. "This means that you get little value from any long-term structure on the Eurostoxx 50," said Mignard. Indices that re-invest the dividend have worked well in this environment, he said.

"We have identified two trends emerging in recent years: one is a theme-based, with solutions like woman leadership, low carbon, megatrends, very topical things; and the second is the proliferation of the quantitative method in equity investing," said Mignard. "All of these trends and dynamics, however, are now very conscious of the pricing characteristics of the index... we require at least excluding filter on most volatile and lowest div stocks."

Langedijk noted that tradability is one of the most important characteristic when designing indices. "We work very closely with our colleagues from Eurex to launch derivatives on indices, helping creating enough liquidity to allow clients to play complex strategies, like timing of factors, market neutral."

Liquidity is also important for mitigating the crowding risk posed by the proliferation of factor indices focusing on narrow themes, like high dividend and low volatility, the panelists agreed. "It is key to develop indices that are conscious of market caps and volumes, and having processes that smoothen the rebalancing," said Mignard. There has been a trend towards quality equity, with many investors fleeing fixed income in the direction of low beta, low volatility equity as the next best thing, according to Mignad. "Minimum variance did massively perform, particularly in the low rate environment, but there have also been strong returns from momentum, which could indeed easily change if rates increases," he said. "It is critical we make sure we still have a return engine that would suffer if the environment changes. Keep identifying and focusing on market distortions, leverage and arbitrage those."

Varsani said that diversification between pro-cyclical and defensive factors is important. While valuations are at 10-year highs, it is the defensives that have largely carried the market, and conceded that this has indeed prompted some indications of a crowding risk in the sector, according to Varsani. "Diversification is key. Noone has unwavering confidence of how long the cycle will last, and when it would turn, which is why multi-factor investing has been a more comfortable route," he said.

Environmental and Social Governance, or ESG is bound to attract more funds, and having a guarantee that a whole structure is green will be important for structured products, according to Darville. "Does having an option on a green or sustainable index qualify the whole package as green, or would the rest of the structure - the certificate, or the bond, also need to be from the sustainable theme? How would banks make sure the structured product 'passes' the green mark is a question that would need to be addressed," he said.

Related stories:

Demand for new underlyings is increasing as the FIA market grows, SRP Indexed Insurance Forum

We have a real task ahead not only to explain the individual product but also where they fit, SRP Indexed Insurance Forum

We are not just coming out with gimmicky ideas to sell more products, SRP Indexed Insurance Forum

Index roundup: ING and Bloomberg launch emerging markets indices