The market for leveraged products in Singapore is getting increasing traction following the launch in the summer of the new two types leveraged products- structured warrants and daily leverage certificates (DLCs), according to Luuk Strijers (pictured), director and head of products at SGX.

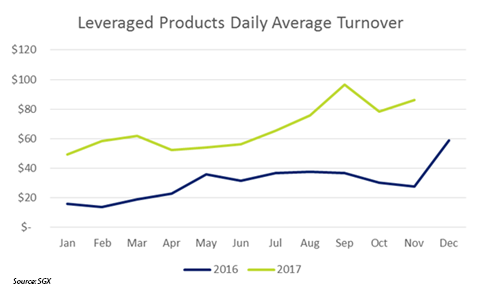

"Average daily turnover is significantly higher in 2017 when compared to 2016," he said. "Month-on-month comparison, for October daily turnover is up 160% and for November (until November 28) - up 211%. For structured warrants, 95% of the volumes are typically in HSI warrants, while approximately 70% of the DLC volumes are executed in the MSCI Singapore ones."

The main driver of activity in the market for leveraged products in Singapore is the access to leveraged exposure to a variety of underlyings, according to Strijers. "Investors are interested in these product types especially during bull trends or market highs. Naturally activity is boosted on days with higher volatility," said Strijers.

However, while there is a strong appetite for leveraged trading in Singapore, there has not been any new listed products in the past ten years after the introduction of warrants, according to Strijers. "Due to the complexity of warrants, many investors turned to trade contracts for difference (CFDs) on overseas indices, commodities and Forex (FX)," he said. "We see that the transparency and simplicity of DLCs on SGX will offer a fresh new trading option for investors to capture short term market moves."

SGX is not seeing an impact of current regulatory changes on trading activity, although the regulatory regimes such as the Specified Products Regime implemented by MAS in 2012 requiring pre-qualification before investors can access leveraged or complex products, could limit the size of the investor base, according to Strijers.

On the other hand, the current low interest environment pushes investors to look for yield. "For that reason, we at SGX see a lot of interest in our 3 Reits ETFs, for example, with indicative index yields of more than 5%," he said. "Investors with a higher risk appetite can also trade our structured warrants and DLCs range for the same reason."

Strijers believes this segment will continue to grow on the back of continued investor education and awareness. "Since their launch, more than S$1.5bn has been traded in DLCs and investor feedback is positive," he said. "Thus, we see the potential for more issuance of DLCs, such as higher leverage DLCs and more DLC listings with other market indices as the underlying, possibly by new issuers."

The reception and performance of the DLCs have been very positive in the past months with total turnover since their launch in mid-July standing at more than S$1.5bn. "We see the number of unique investors steadily growing," he said. "Outstanding (overnight) positions which are reported on a weekly basis by issuers is gradually growing too. In Europe, DLCs have shown the largest growth, in terms of traded value compared to other listed structured products since the introduction in 2012."

DLCs have less complex product features compared to warrants, CBBCs and options, which may suit a more broad-based audience and thus have higher potential for sustained trading interest, according to Strijers. "Furthermore, Asian investors have shown a strong appetite for leveraged products in recent years, as demonstrated by the activity in the local structured warrants market, the success of CFDs and leveraged and inverse funds in the region," he said. "We think that the transparency and simplicity of the DLCs listed on SGX will offer a fresh new trading option for investors looking to capture short term market moves."

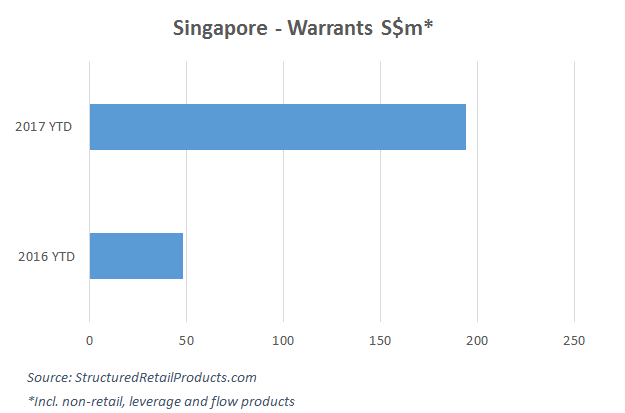

According to SRP data, a total of 171 warrants worth S$194m were issued in Singapore year-to-date, up 304% compared to the same period last year when a total of 16 warrants worth $48m were issued.

Related stories:

DBS's wealth management income spikes by 25%

SFC conducts a thematic review on prime services and related equity derivatives activities

UOB adds rates and commodities to multi-asset offering (Part 2)