For those who work in structured products and derivatives in 2015, August 3 was not a good day.

Following the release of bad economic news from China, the Hang Seng China Enterprises Index (HSCEI), which tracks China companies listed in Hong Kong, collapsed rapidly, from 11,009 to 9,400.

One of the reasons behind this massive 15% crash, as well as the negative effect of the economy news, was the massive exposure to this benchmark index by means of structured products and derivatives. Back then, according to SRP data, there were US$58.4 billion of live structured products linked to the HSCEI, of which 75% were autocallables products.

The truth is, because most investors were investing in the same underlying and payoff structures, the hedging of these products, together with the knockin feature of autocallables, meant that all investment banks had the same trading position. With, therefore, no counterparty, there was only one solution: hedging the underlying risk by taking a position on the underlying asset. This means that, whenever the underlying asset depreciates, issuers need to sell their position on the underlying at the worst time, which exacerbated the pressure on the price of the underlying.

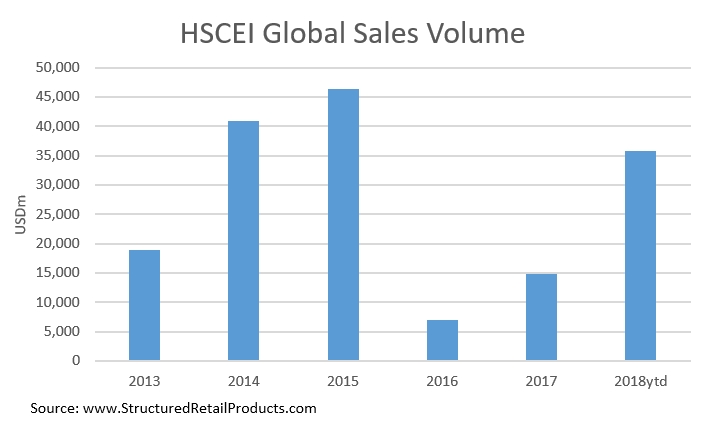

Subsequently, there has been a substantial reduction in use of the HSCEI, with the Eurostoxx 50 and S&P 500 replacements for the $45 billion sold in 2015.

But watch out. Since the beginning of this year, the hunt for yield has ensured that the Hang Seng China Enterprises Index is back on the radar as one of the most popular underlyings globally, with sales of more than $35 billion between January and the end of August this year.

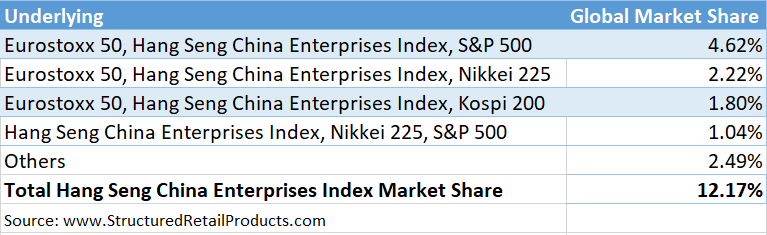

With almost 13% of the structured products sold this year linked to the HSCEI, you cannot stop wondering if we are looking at the same story all over again. There may be less delta linked to the HSCEI compared to 2015 - with $43 billion outstanding, decreasing the risk - the percentage of autocallables has increased to 77%, with all depending on the performance of Chinese equities, but also how the trade war between the US and China will affect the mainland’s benchmark index.