Structured products are investments which provide a return based on the performance of an asset.

Introduction to Structured Products.

Structured products are investment vehicles made up of different building blocks. A bond or deposit that aims to provide the capital repayment feature and financial instrument linked to the underlying asset, which often is an option or derivatives strategy that provides the return feature of the investment. The two components combined, create a unique investment, and the level of risk and return can be customized to meet the needs of the target investor.

Both the return and capital repayment depends on the performance of an underlying asset such as equities, indices, funds, interest rates, currencies, commodities, and many other asset classes.

Compared to other investments structured products offer defined returns that are contractually binding, and the possible return and capital repayment scenarios are communicated to investors before the investment is made.

Since most of the features are defined at the outset, they can easily be divided into different product categories, making it easier for investors to find investments right for them.

They are bought by institutions, high net worth individuals, and retail clients.

Let's start with capital protected products. When investors seek to get back what they invested at the end of a period, plus a return in excess of deposit rates, they use capital protected products. Their return is similar to bonds, and they are mainly used to provide participation in different asset classes, whilst protecting capital when the market drops.

Now let's look at yield enhancement products.

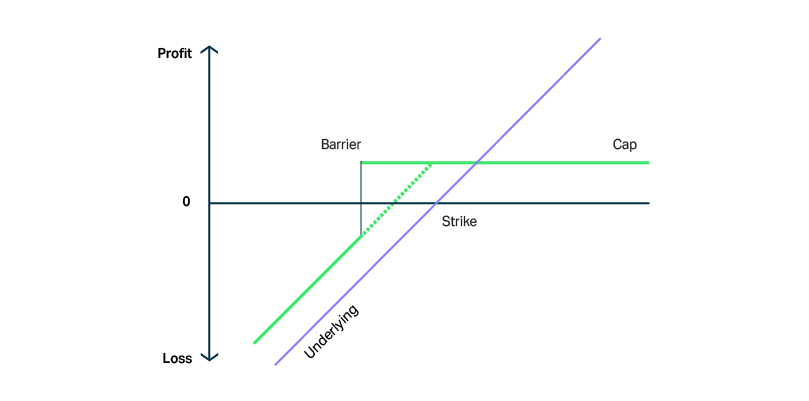

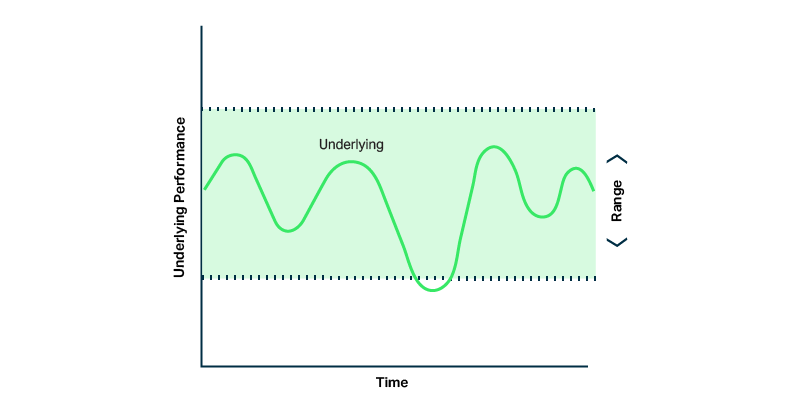

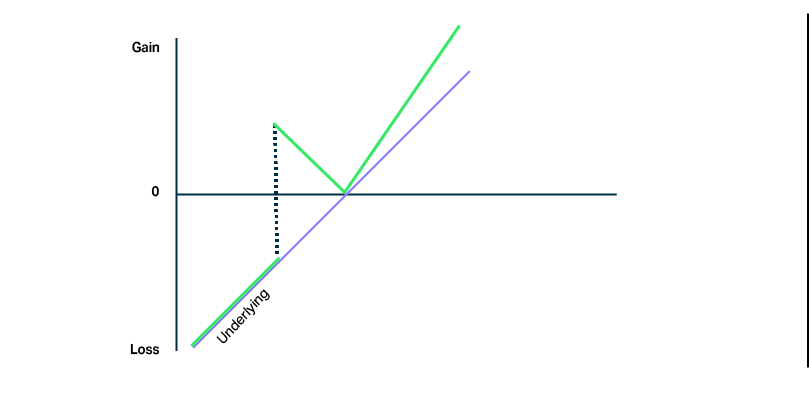

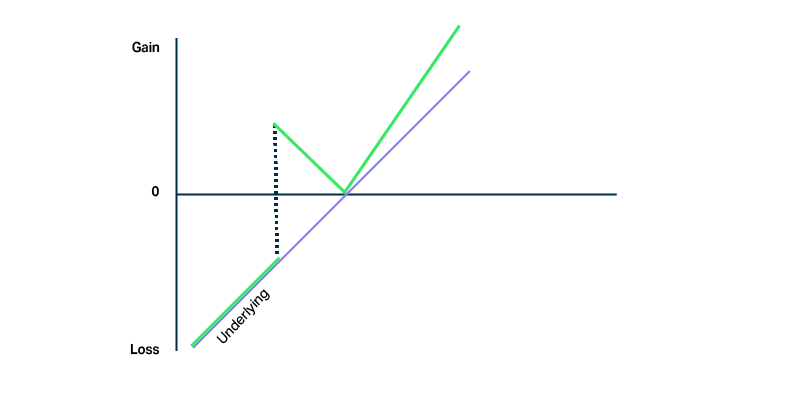

These products may provide investors the opportunity to generate higher yields and are suitable for investors willing to risk some or all of their investment to obtain this income. An investment in this category usually involves less risk than a direct investment in its underlying asset classes since they often have some level of predefined protection against market falls. However, investors may potentially lose some or all of their investment if the underlying asset falls below this level of protection.

Now let's look at Leveraged Products.

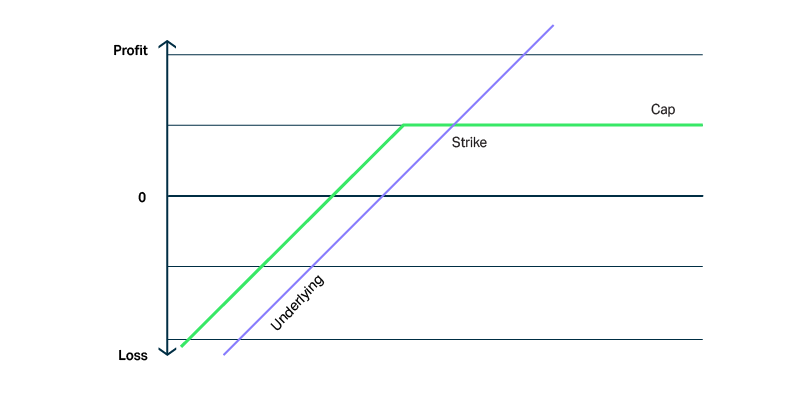

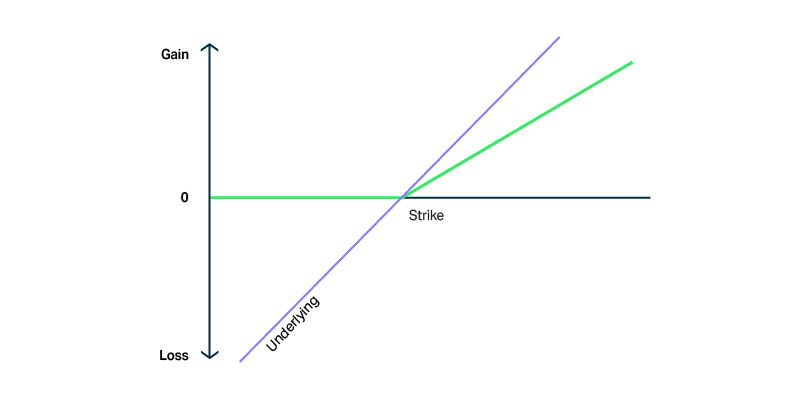

Leveraged products are used when investors are looking to take a directional position on an underlying asset while only investing a fraction of the underlying price. Investors therefore take advantage of leverage amplifying underlying movements. They are widely used to change the risk profile of investment portfolios, but are also used to hedge against negative market scenarios.

Now let's look at the Risk and Benefits that you should be aware of before investing in a structured product.

Benefits of structured products.

Their flexibility means that they can give investors exposure to different asset classes and they can be designed with different level of protection and the expected returns are clearly defined at the outset.

Risks of structured products.

Counterparty risk is the risk of a client losing money, when there is a failure of the bank that backs the products.

Now let's look at the risks. For structured products, counterparty risk is the risk of a client losing money not because of the performance of the product, but because of the failure of the bank that backs the product.

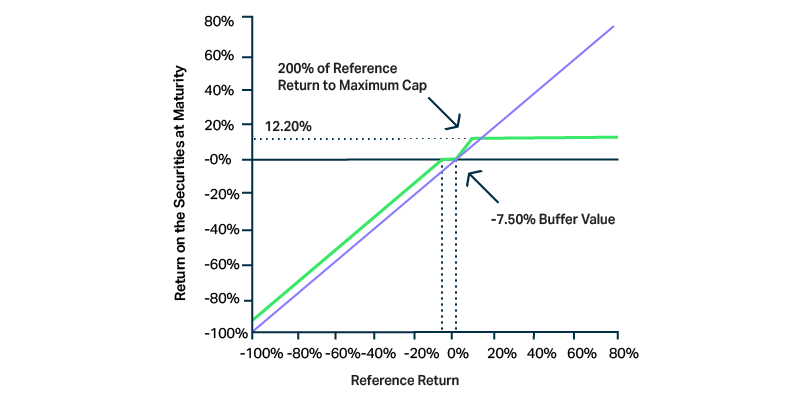

Both returns and capital repayment may be exposed to downside market risk.

You should be willing to hold your structured products to maturity since there may not always be a liquid secondary market.

This is not a complete list of risks and you should always read the documentation of the product before investing and speak to your financial advisor before proceeding with an investment.

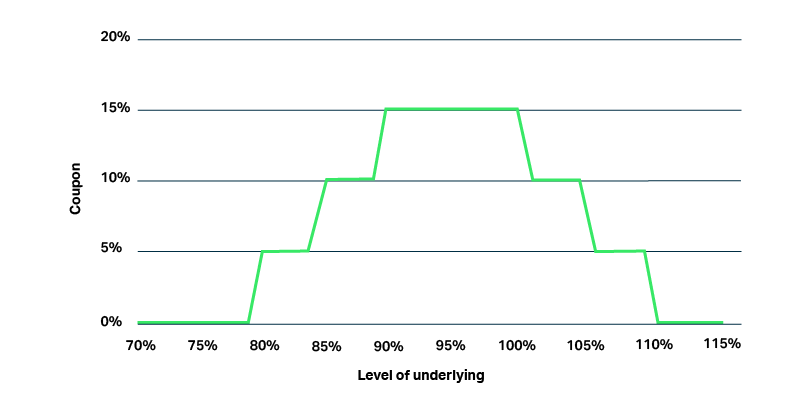

This asset can cover the equity, index, fund, interest rate, currency, commodity or property markets. The payoff and level of capital at risk can be pre-defined. Payoff profiles can be designed to take advantage of rising, falling or range bound markets, and delivered in a way that can be tailored to the needs of investors.

They are designed for investors who are prepared to invest for a fixed period, and who also want some degree of protection over their initial capital.