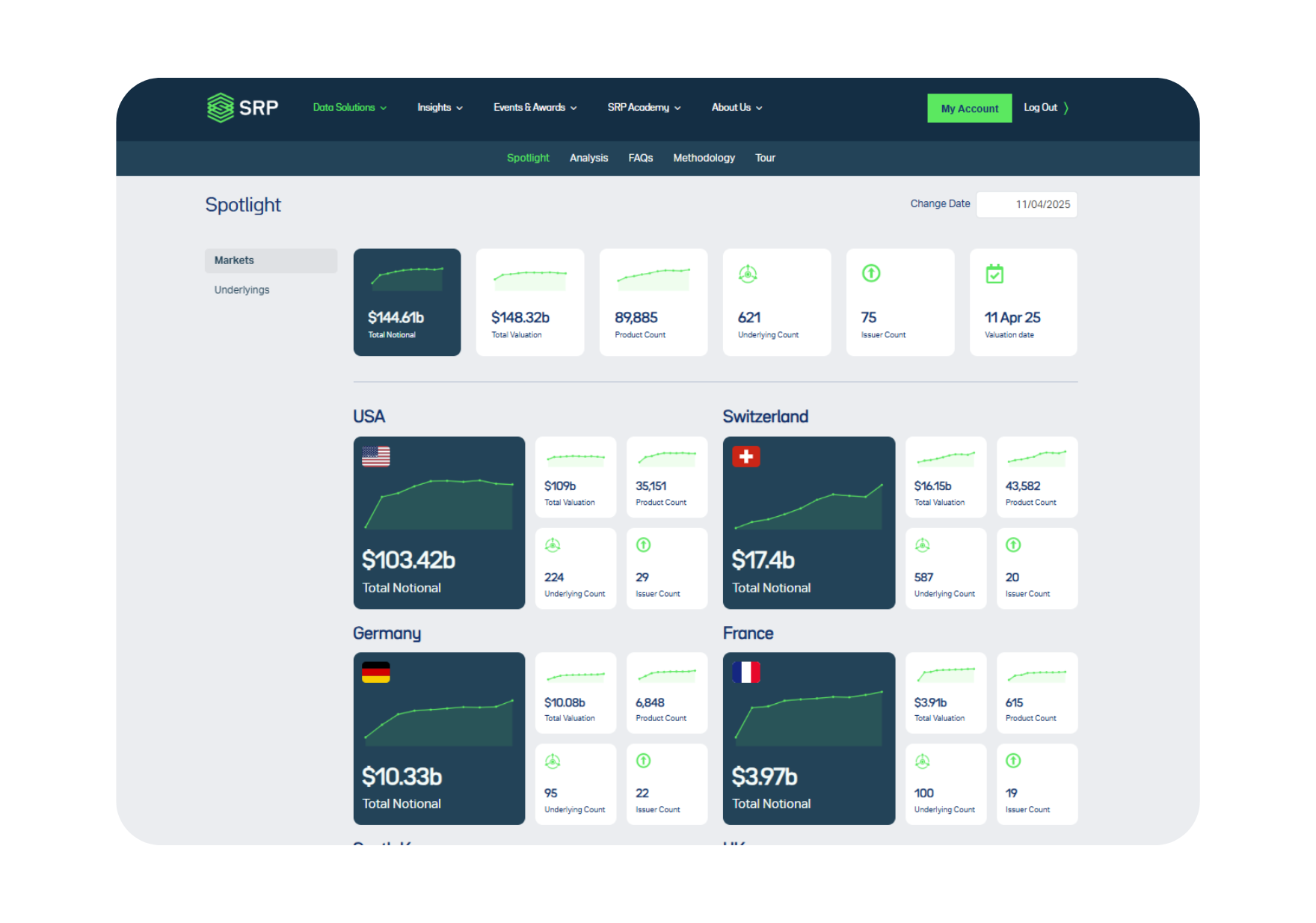

Greeks Analysis

Track daily Greeks. Master structured product risk. Built on the industry’s largest structured product database, SRP Greeks delivers daily sensitivities for Delta, Gamma, Vega, Theta, Vanna and Charm across key underlyings such as the S&P 500, Eurostoxx 50, KOSPI, Nvidia and Tesla — so you see exactly how real‐world products behave.

Request Demo Get Started

.png)