Much has been said about the structured product industry and the self-inflicted wounds we committed in the past

Nevertheless, what stills shocks me is the easy target we make ourselves into and how we constantly need to justify our imperfections instead of our potential.

When I first started in the industry as a product creator, I was given a simple challenge: how to diversify client’s portfolio using structured products?

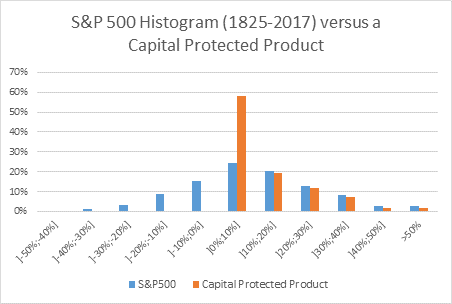

Back then, I researched 12 years of data with performances and the total funding for each product. And it was love at first sight, as I concluded that capital protected products had delivered added value to our clients consistently.

But the most interesting fact is that they delivered the most value when we had more complaints. Why? It was mainly when they did not provide any positive performance, as the underlying, equity or other asset classes had a negative impact.

The truth is that capital protected products are to your portfolio, as your insurance is to your house. You accept paying a small premium in exchange for protecting part of your capital against unlucky circumstances.

What returns should you expect then?

The truth is that structured deposits and capital protected products have the advantage of not being a cost but giving you a return while allowing you to shape the distribution of your future returns, ie., with capital protection you can ensure that you won’t have negative performances but in exchange you lower your expected return compared with the underlying.

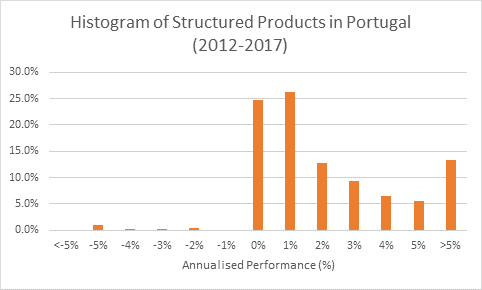

In the Portuguese market, the average annualised return between 2012 and 2017, has been 2.04% on 859 products matured in that period. With the most impressive result being that only 1.6% of the products provided a negative return, compared with a 13.4% of the products who provided an average return above 5%.

If you analysed only capital protected products, where structured deposits are included, the average decreases to 1.7%, on 755 products, as 57% only provided the minimum return, but 43% of these products provided a return above traditional deposits.

It is not a secret that there are many embarrassing structured products out there, which were created to maximise profitability for the distributor or the issuer but thankfully, as in all financial industries, they are a minority, and most of us try to help our customers.