Shakespeare showed us the value and meaning of things and how they can change so suddenly with the exclamation from the play, King Richard the Third.

We can almost consider it poetic, that after so many disappointing absolute returns and mixed performances from other asset classes, how autocallables are now becoming essential to investors’ portfolios.

According to SRP data, autocallables, which represented 10% of structured products sold back in 2009, ended 2017 with a 40% market share globally.

What is an autocall?

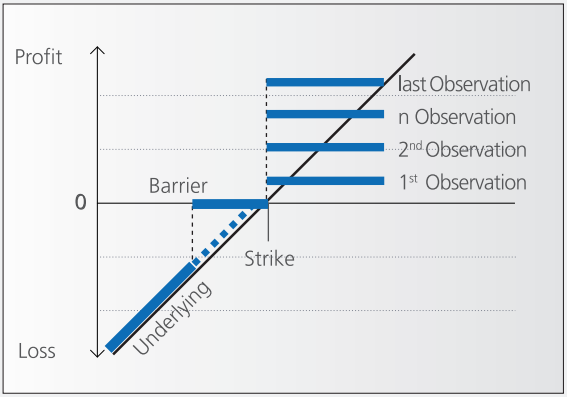

An autocallable product is a structured product that has an automatic call feature on pre-defined dates known as the auto-call dates. Usually they offer a large coupon payable if a call level is triggered when the underlying is above the strike on the pre-defined date. If not auto-called, the coupon increases and goes on to the next call date that the condition is revisited.Shakespeare showed us the value and meaning of things and how they can change so suddenly with the exclamation from the play, King Richard the Third. We can almost consider it poetic, that after so many disappointing absolute returns and mixed performances from other asset classes, how autocallables are now becoming essential to investors’ portfolios.

The large coupon itself is achievable as the investor is selling a knock-in put which has a barrier level, where the capital becomes at risk if the underlying is below the barrier level, usually at maturity. As such, the coupon level is more dependent on the volatility of the underlying than the interest rate environment.

Why the increase in demand?

As interest rates decreased, autocallables started to become more eye-catching and with annualised coupons around 6%/7% pa. they seemed to be the perfect asset to hold on a sideways equity market.

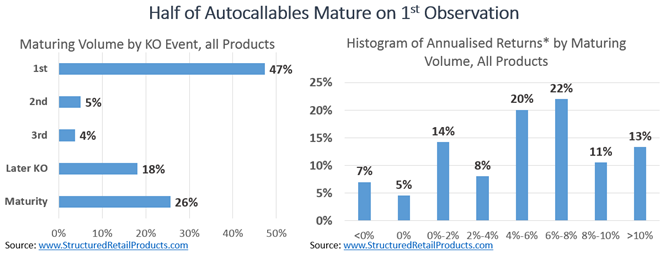

But above all, experience has been telling investors that these are good products. From the 56,545 autocallables with performance that SRP collected in the past 17 years, almost half of them expired on the first observation, providing an average annualised coupon of 7.35%.

If that’s not impressive, 88% of the autocallables provided a positive performance, with only 7% losing capital.

With an average of 4.76% annualised returns, even with almost 2,000 products suffering a negative return around the financial crisis with a 1% negative return, autocalls seems to be a good solution to increase returns.