After riding on an upward trend for many years, ESG-linked products faced a difficult 2023, with both sales and issuance significantly down year-on-year (YoY).

SRP reviewed ESG-linked products in Europe and France during 2023.

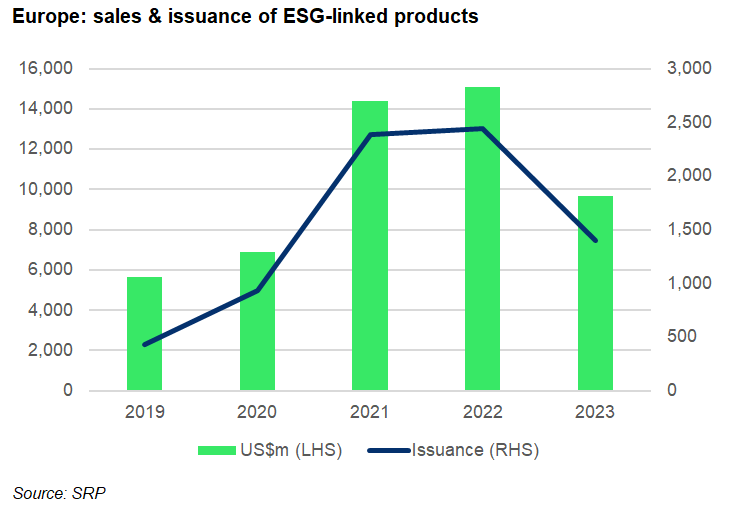

Sales volumes of structured products linked to ESG underlyings reached US$9.6 billion in 2023 – a 36% decrease compared to record year 2022 when US$15.1 billion was collected. ESG-linked issuance also fell: from 2,482 products in 2022 to 1,475 products in 2023.

ESG products were seen in 16 different markets (2022: 18) of which Germany accounted for the highest issuance, 1,139 products in total – mainly on the back of 634 DZ Bank DZ Bank products that were linked to the MSCI World Climate Change ESG Select 4.5% Decrement EUR Index.

There was also significant interest from German investors in the idDAX 50 ESG NR Decrement 4% PR EUR Index and MSCI EMU SRI Select 30 Decrement 4.0% Index, seen in 202 and 101 products, respectively, exclusively issued on the paper of Landesbank Baden-Württemberg (LBBW).

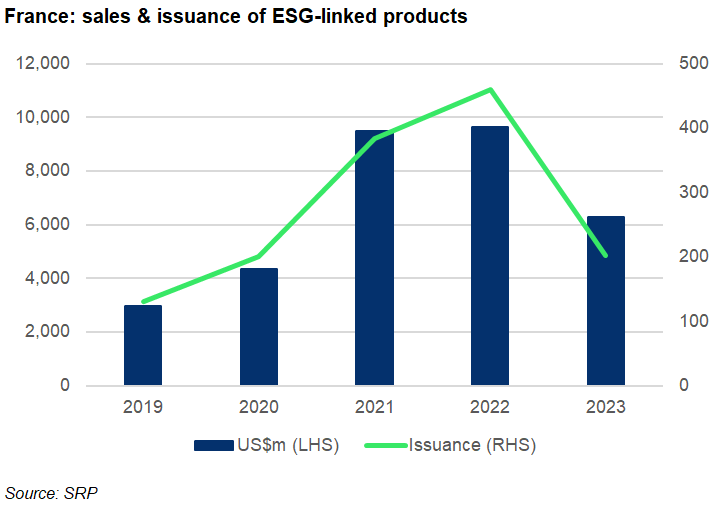

In France, where 234 ESG-linked products were issued in 2023 – much lower than the figure seen in Germany – sales volumes were by far the highest of any European countries. In fact, at US$7.1 billion, they made up almost 75% of all ESG-linked volumes in Europe.

The highest volumes were attached to 12 Natixis' products linked to the iEdge ESG Transatlantic SDG 50 EW Decrement 5% NTR Index that sold a combined US$830m, including the best-selling Avenir Responsable no 3, a capital protected structure that has one autocall point halfway through its 9.7-year tenor.

Another ESG index that attracted interest, again with a Transatlantic theme, was the Solactive Transatlantic Biodiversity Screened 150 CW Decrement 50 Index, which was seen in six products worth an estimated US$440m that were issued via Société Générale.

However, despite being the biggest market for ESG-linked products in Europe, 2023 volumes in France were down 26% YoY while issuance fell by almost 50%.

A third country with high ESG-linked volumes is Italy, where 21 products gathered sales of US$840m in 2023, thanks mostly to five products on the Stoxx Europe ESG Leaders Select 30 EUR Index that sold US$320m.

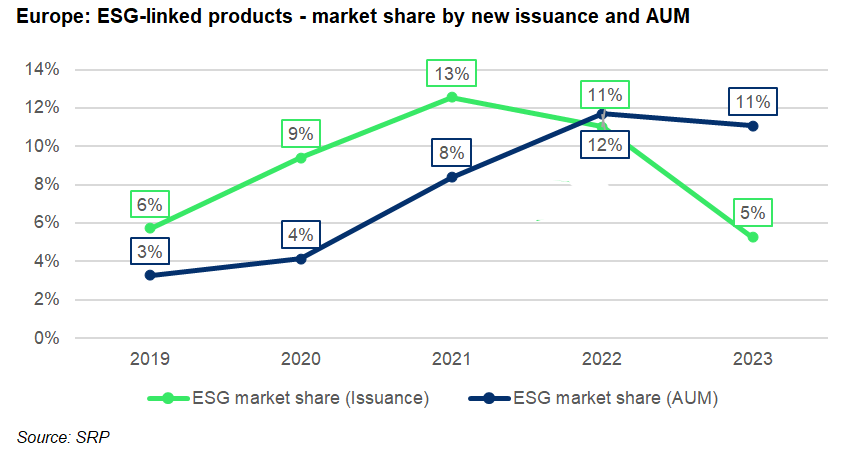

When comparing the flows in the outstanding notional and the new issued notional for ESG-linked products, we notice that these products captured five percent of the European market by new issuance in 2023, down from 11% in 2022 and the all-time high of 13% in 2021. At the same time, their total outstanding notional or AUM, stood at 11%, down one percentage point YoY.

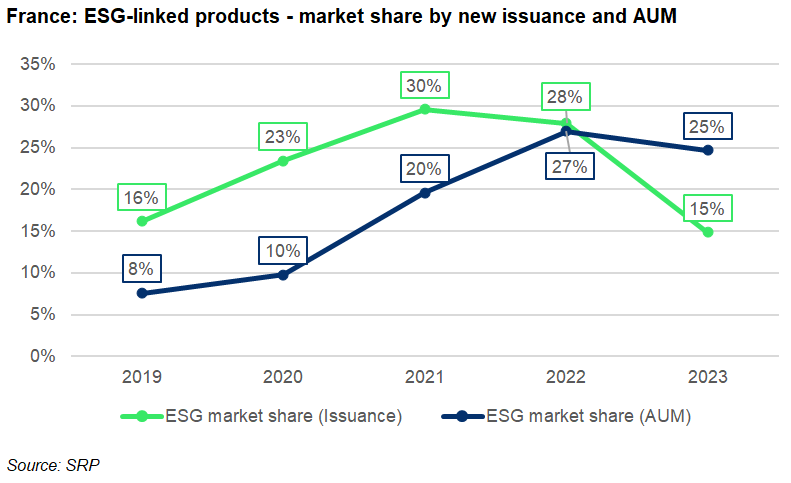

By comparison, the market share for ESG-linked products in France is much higher – both for new issuance and AUM. The former claimed 15% of the overall French market, down from 28% and 30%, respectively, during the previous two years, while a quarter of all outstanding volumes in 2023 were ESG-linked, compared to 27% in 2022 and 20% in 2021.

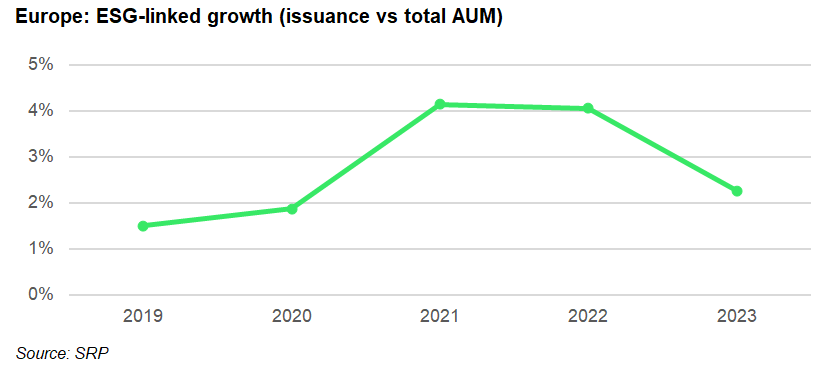

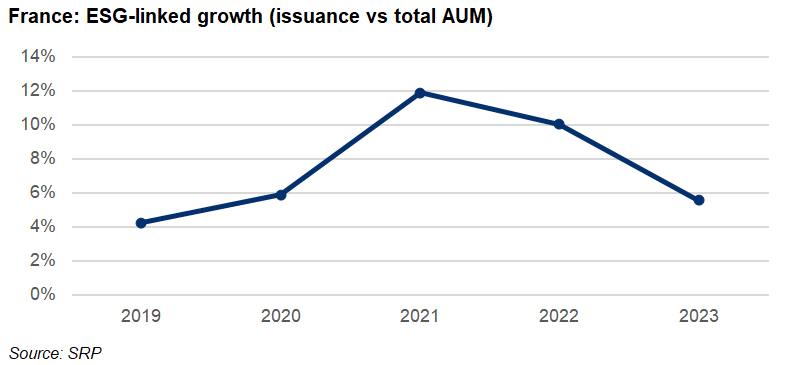

Looking at the dynamics of the new issuance relative to the outstanding volume, another way of analysing the newly issued ESG-linked notional over the years, would be as a relative measure compared to the total outstanding notional (AUM). This metric shows the dynamics of the ESG-linked market segment, and it could provide a forward-looking insight for the size of this market slice, as the new volumes compared to expiring outstanding volumes determines the market evolution.

The above chart shows that the activity in ESG-linked products in Europe has been slowing down over the last two years, with a current ratio of 2.3% in the end of 2023 in Europe, indicating a relative low volume of new issuance which, if this trend continues, may result in a continued decreasing market size.

For France, the average ratio in 2023 is 5.5%, while it has ranged between four percent to 11.9% for the period 2019 to 2022.

Main image: The KonG/Adobe Stock.

Do you have a confidential story, tip or comment you’d like to share? Write to info@derivia.com