copy.png)

Credit linked products represent an interesting niche area of income investments, and they are related to both the corporate bond and structured products market.

Credit linked products have been around for many years and provide a way for investors to aim for a significantly higher yield than the risk-free rate.

With the rise in popularity of Credit default swaps and various credit instruments in the early 2000s this sector became very popular but subsequently gained huge notoriety after the real estate bubble, the credit crunch of 2007 and the default of Lehman Brothers in 2008.

Prior to 2007 many investors barely gave A-rated entities any consideration from a credit risk standpoint except to take simple diversification measures

The complexity and opacity of credit linked instruments spiralled to an unsustainable level and most operators in the market significantly underestimated credit risk of banks and major corporates. Prior to 2007 many investors barely gave A-rated entities any consideration from a credit risk standpoint except to take simple diversification measures.

This situation was exacerbated for structured credit instruments which came in for much criticism. Products that claimed high credit-worthiness were being issued but turned out to be highly leveraged and risky. It took ten years after the global financial crisis for the retail market in most countries to consider using such products again in any meaningful volume. The part that credit instruments played in the global financial crisis also had serious regulatory repercussions.

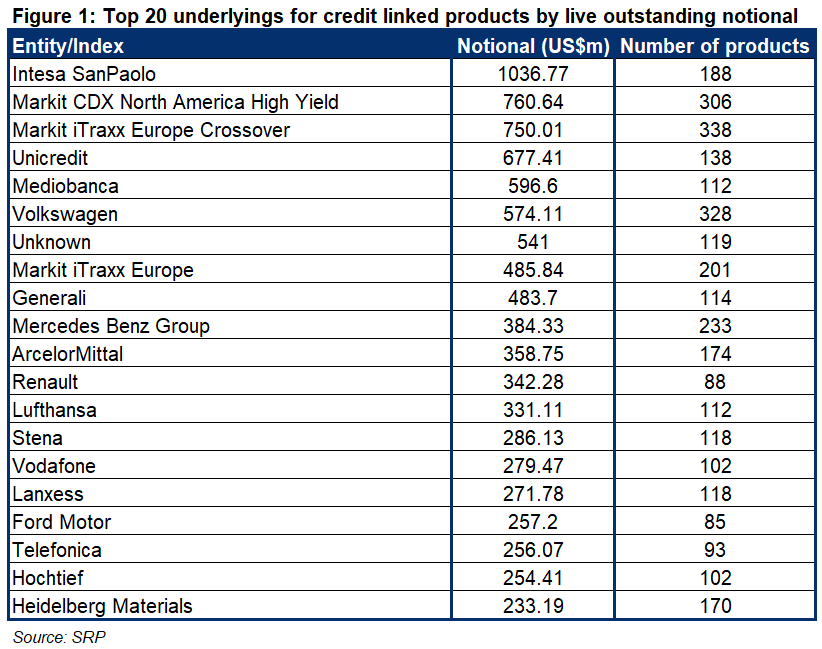

Today the credit linked product market is split between single name notes and tranche linked products as can be seen from the table below:

Single names, indices

It has long been the case that equity linked issuance in structured products is divided between equity index products and those using single stocks or baskets. The vast majority of products are linked to the mainstream indices as investors prefer broad based exposure. By contrast, the credit linked market is dominated by single names with the three main credit indices only accounting for 20% of the market by notional and 25% by number of products as can be seen from the table.

The company IHS Markit has long established itself as the leading credit index and data provider. The Markit iTraxx Europe Index comprises the 125 most liquid European companies in the CDS market, and the Markit iTraxx Europe Crossover is made up of the 75 most liquid sub investment grade companies. These two indices give different levels of exposure which can be used to create products depending on risk appetite.

The equivalent indices covering US corporates are the Markit’s North American Investment Grade CDX Index calculated from 125 companies and the Markit CDX North America High Yield Index drawn from 100 sub investment grade companies. While the North American High Yield Index is the most popular credit index of all in structured products, rather surprisingly the main US credit index is well outside the top underlyings and is not currently a popular solution for credit linked products.

Credit indices allow investors to seek high income levels with different types of exposure. Some products are linked to the index itself in a basket construction, but more leveraged solutions feature “tranche” approaches, whereby losses are accumulated at different layers.

A note can lose perhaps 10% of capital for each of the first ten names. A lower tranche product might allow for the first five defaults but then lose 20% of capital for the next five names. The tranche products are more difficult to value and hedge and add a significant amount of complexity.

Single name products are much simpler and offer a coupon that is paid until a credit event occurs, at which point the product terminates and the relevant recovery value is paid back as capital payment. Single name products are much closer to corporate bonds, although they can be tied to more credit events and therefore investors need to understand the full range of circumstances where income or capital is at risk as these can be wider than what would impact a regular corporate bond.

Credit linked products have been seen in various markets but have proven particularly popular in Scandinavia. Sweden, Finland and Norway have a strong fixed income culture and therefore credit linked products provide a natural way to seek higher yields in a related asset class.

Regulators in these markets have also placed severe restrictions on the Equity linked structured products market over time because of perceived complexity and risk. Therefore, credit linked products were the only meaningful way to seek higher yields.

Single name credit linked products are popular in Italy. This is for a rather different reason, in that the Italian market has traditionally had well known companies that have carried high credit risk for years and therefore the investor base is more comfortable with that concept. The three most popular underlyings in the above table are the Italian banks Intesa SanPaolo, Unicredit and Mediobanca. Volatility in the global banking sector has contributed to their yields being higher.

Two recent examples linked to Intesa San Paolo pay a fixed coupon and full capital return provided no credit events have occurred. Product with SRP id 44312588 pays 3.15% in a CHF denominated note over two years, and one with SRP id 45054282 pays 5% in EUR over 5 years.

These headline rates are quite different, but both represent around 200 basis points over the risk-free rate in the two currencies. The German company Volkswagen is also high up on the issuance table, and one example product is SRP id 44710560. This pays 4% coupon in EUR, representing around 100 basis points over the risk-free rate. Since most investors would trust a company of this size to remain solvent over the life of the product, they are happy to take the associated risk in order to produce higher yield.

Both the fixed income and equity linked structured product sectors have solutions to generate high income. The credit sector is an alternative and interesting way to try to achieve the same goal.

Image: Adobe Stock.