Sales for products linked to indices from the consumer discretionary sector increased by 54% YoY mostly driven by sustained exposure to luxury goods companies and auto manufacturers.

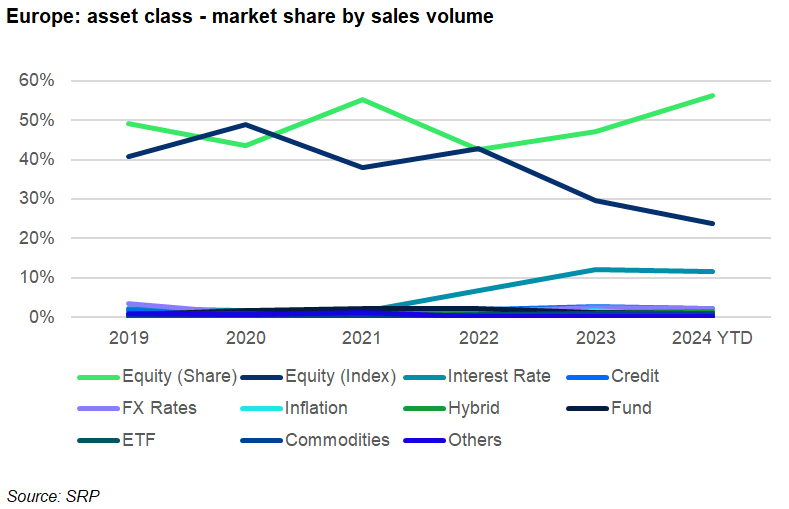

In Q1 2024, structured products linked to equities regained market share in Europe against a backdrop slightly less favourable for rates-linked products, compared to 2023.

In this article, we look at sector thematics driving the demand in Q1 2024, based on the sales volumes collected by single name- and industry sector index-linked products.

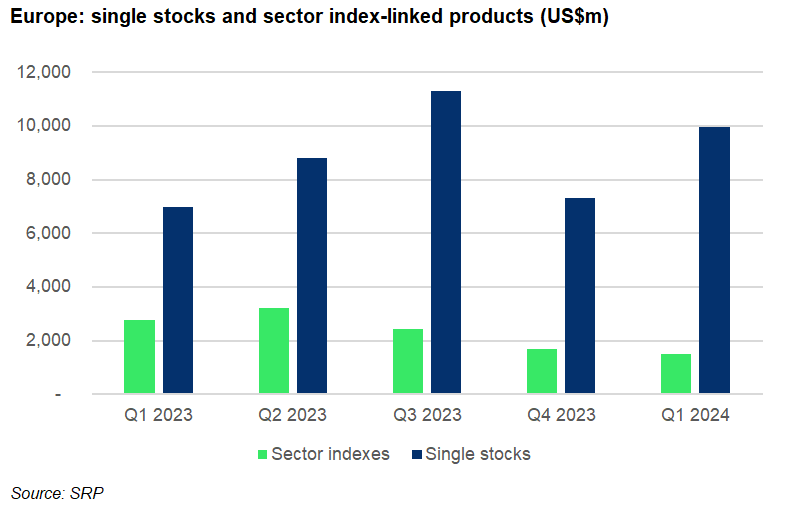

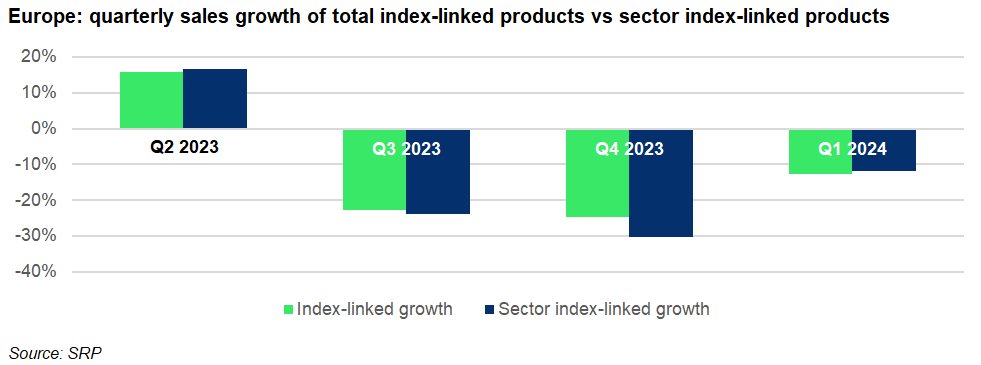

Estimated volumes invested in products linked to industry sector indices decreased for the fourth consecutive quarter, reaching US$1.5 billion in Q1 2024 – down 12% compared to the previous quarter.

The decline is in line with the overall drop in volumes linked to equity indexes seen in the past three quarters, which was driven mostly by strong stock market performance at the end of 2023 and the beginning of 2024, which drove equities near peaks and led to investors turning to specific quality stocks instead – pulling back from less concentrated indices.

Another contributing factor was the rebound in activity in Switzerland - Europe’s largest structured products market, which is historically biased towards single names rather than indices.

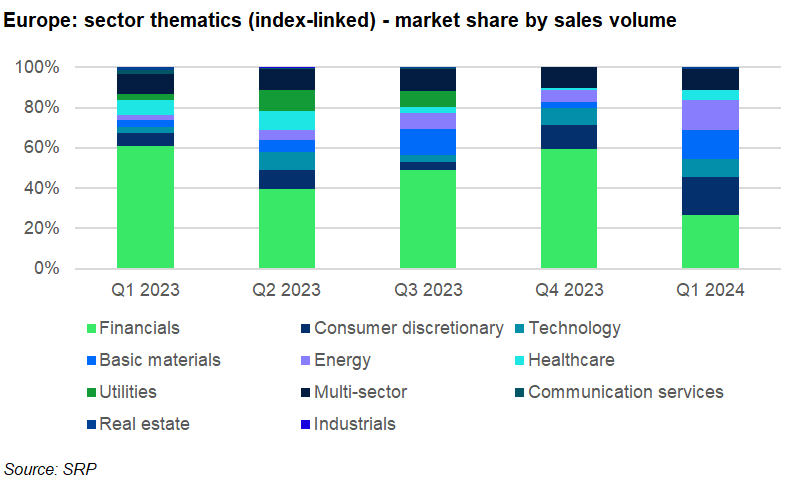

In terms of market share, indices linked to sector thematics have remained stable representing around a fifth of all index-linked volumes for the last five quarters in Europe. However, in certain markets like France and Italy, sector indices represented 27% of the total equity index-linked volumes.

Among the sectors that saw the most activity in 2023, the financials (banking) sector has remained a top choice as it remains undervalued relative to its potential. Additionally, the energy and basic resources sectors also drove significant activity as they are expected to benefit from higher rates and inflation.

As we can observe from the chart below, in Q1 2024 there has been a considerable shift in exposure to sector indices. Indices build around consumer discretionary, basic materials and energy stocks, all significantly increased their market share year-on-year (YoY) at the expense of financial sector indices which saw their market share shrinking by half.

In Q1 2024, consumer discretionary sector indices claimed an 18% market share of the sector index thematics, up from six percent in the first quarter of 2023. The 54% sales growth YoY was mostly driven by sustained exposure to the luxury goods and auto manufacturer industries, led by the Bloomberg Luxury 2021 Decrement 50 Point EUR Index (42 products since January 2023) and iEdge Transatlantic Luxury Goods & Services 10 EW Decrement 50 Points GTR Index (30) for the former, and S&P Eurozone Automotive & Electric Vehicles 50 Point Decrement EUR TR Index (14) for the latter.

Additionally, 41 products were linked to the Bloomberg Eurozone DM Top30 Banking Consumer D and Energy 50 Pts Index – a multi-sector index exposed to three different sectors.

The narrative behind these exposures was to maintain a diversified approach around themes subject to profound economic changes (automobiles, banks, energy) and discounted earnings multiples relative to growth-oriented thematics.

The largest YoY sales growth was recorded by products linked to indices offering exposure to the basic materials (+150%) and energy sectors (+190%). Their market share reached 14% and 15%, respectively, up from three percent in Q1 2023.

The technology sector has also seen an impressive run in Q1 2024, with a 50% YoY sales growth and nine percent market share out of the sector indices, based on sales volumes. The Solactive Semi-Conductors Selection PR Index was the most popular index driven by the demand in the semiconductors thematic.

Beyond financials, the aforementioned four sectors represented 57% of the sector index-linked volumes in Q1 2024. This was up from 16% market share in Q1 2023 and a 29% market share in Q4 2023.

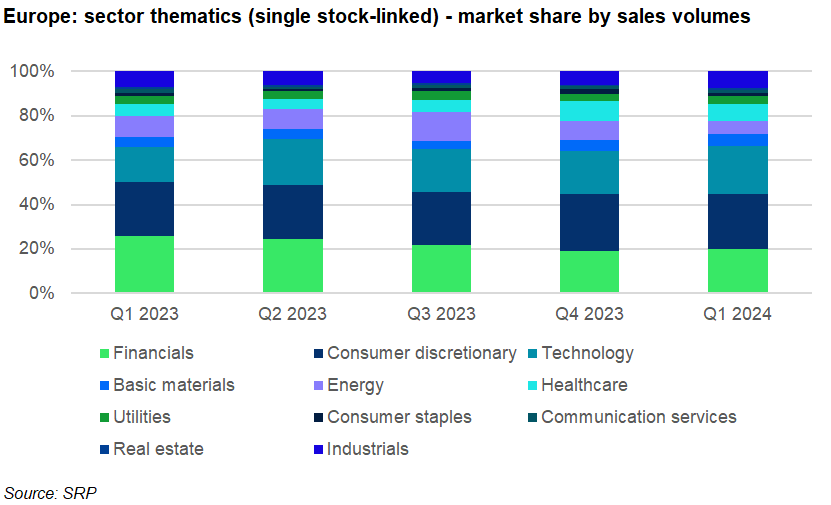

Single stock-linked

Regarding sector exposure through single stock-linked products in Q1 2024, there was dominance of the consumer discretionary sector (25% market share), followed by technology (21%) and financials (20%). The demand for these sectors has been supported by the rebound in cyclical stocks on the back of a favourable outlook for the economy and the IT technology sector rally in Q1 2024.

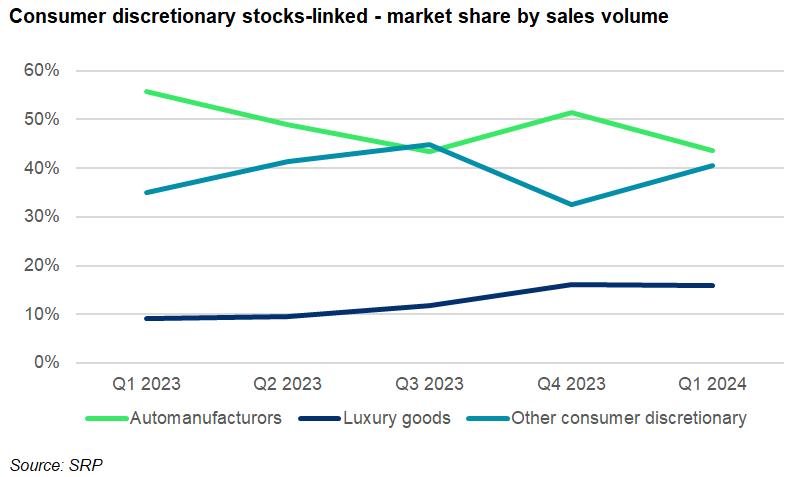

Auto manufacturers represented 44% of the consumer discretionary stocks used as underlyings in Q1 2024, down from an average 49% in 2023.

The share of Mercedes Benz Group notched the top spot - it was linked to 389 products worth an estimated US$300m (13% of the cyclical stocks) sold mostly to investors in Germany (295) and Switzerland (91)

The increasing market share of luxury goods companies shows a resurging interest in the sector with volumes growing 135% YoY and 29% sequentially on the quarter.

The technology sector ranked second with 85% YoY sales growth and 51% sequential quarterly growth. The sector was supported by the semiconductors industry and structural support such as developments in the artificial intelligence (AI) space. The shares of Nvidia (955 products in the quarter of which 882 in Switzerland) and Infineon (428/227) drove most of the activity linked to the semiconductors industry.

Image: Magele-picture/Adobe Stock.

Do you have a confidential story, tip, or comment you’d like to share? Write to info@structuredretailproducts.com.