SRP reviewed 3,200 products that have matured or potentially expire early in France during 2023.

Our analysis of the performance of retail structured products in France in 2023 shows a positive period for the industry and end-investors in a market that continues to grow in size and choice.

The industry has delivered value to investors proving once again that structured products are an efficient way to deliver stable and visible returns, and diversify investment portfolios.

SRP reviewed over 3,200 redeemed products, of which three percent reached their organic maturity date and 97% triggered early maturity during 2023.

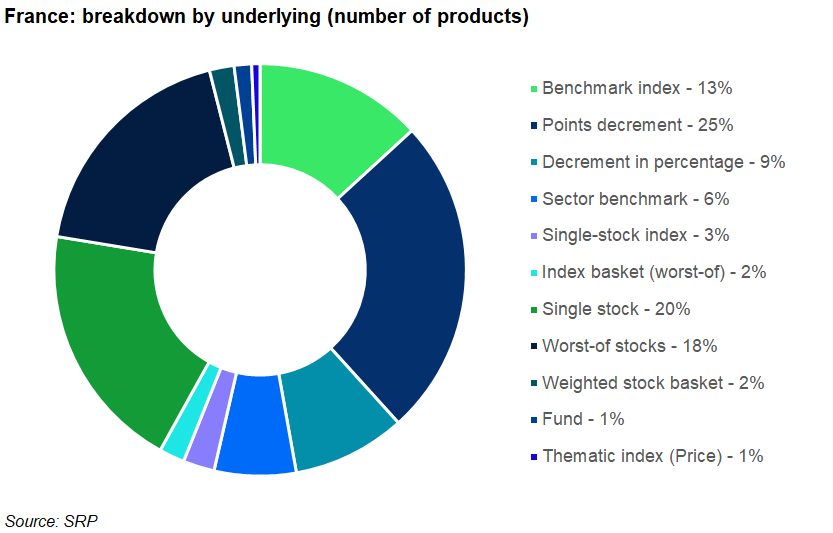

A breakdown of the sample by underlying shows that index-linked products accounted for 59% of the maturities – the majority being linked to decrement strategies. Products linked to a single name represented 20% of the total maturities while worst-of option stock baskets represented 18%.

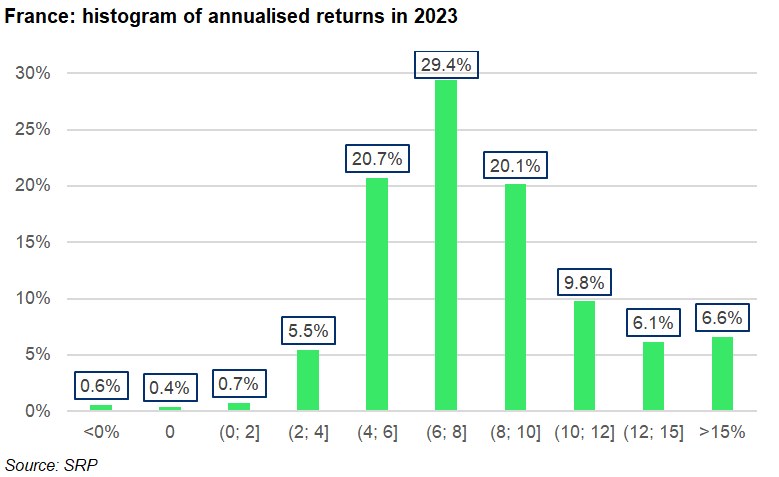

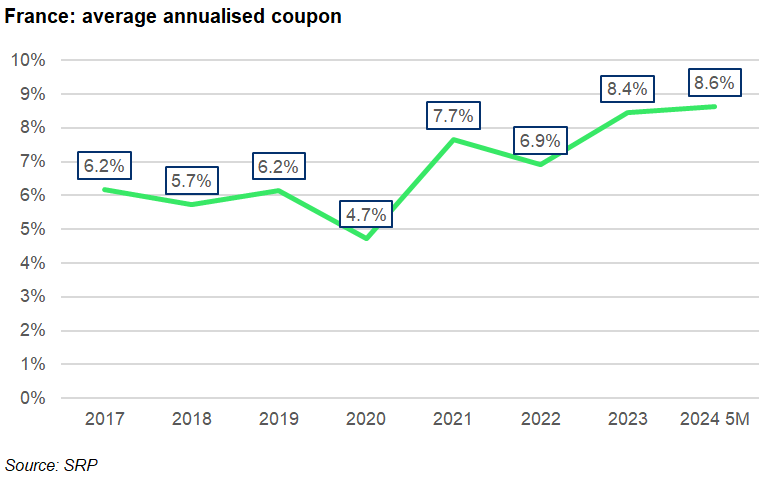

The histogram of returns shows that structured products performed impressively with an average annualised return of 8.4%, which is 1.5% more than the annualised performance reported for the previous 12-month period.

This performance has been realised in a favourable context on interest rates and a rather well faring equity markets, which is in contrast to the consensus at the start of 2023.

Ninety eight percent of all products matured delivered a positive performance with annualised returns of between two and 52%. Some 86% of the products provided an annualised return of five percent or more.

The analysis also found that 40% of the products outperformed the average of 8.44%.

Negative maturities captured by SRP were extremely rare and ranged from -1% pa to -39% pa. Among them were structures linked single names like Vallourec, Electricite de France, Carrefour which were launched in 2015, and some more recent structures linked to the shares of Bouygues, Zoom, Moderna, Nike, and the Hang Seng Tech Index that struck in 2020 and 2021.

Two partially protected structures that returned the guaranteed minimum after eight years of investment were linked to a basket of two funds (Carmignac Patrimoine, Ethna-Aktiv) and three funds (Carmignac Patrimoine, DNCA Eurose, Ethna-Aktiv), respectively. Similarly, three products linked to the Ethical Europe Equity returned 95% and 90% of the initially subscribed notional.

Yield enhancement products, the vast majority autocallables, represented around 95% of the matured volumes. Yield optimisation products consistently delivered around 8.5% over the period which is in line with the objective of these structure: to deliver regular and visible return to investors while ensuring soft protection against market dips and any potential exogenous shocks as we witnessed during market downturns.

Maturing products with guaranteed capital delivered an average annualised coupon of 4.22%. These products were scarce over the period as the low interest rate environment in the prior eight to 10 years did not allow meaningful upside with full protection.

Among them, 14 capital guaranteed autocallable structures have triggered their early redemption in 2023 returning an annualised average of 6.2% to investors for an average holding period of 1.8-years.

Types of underlyings

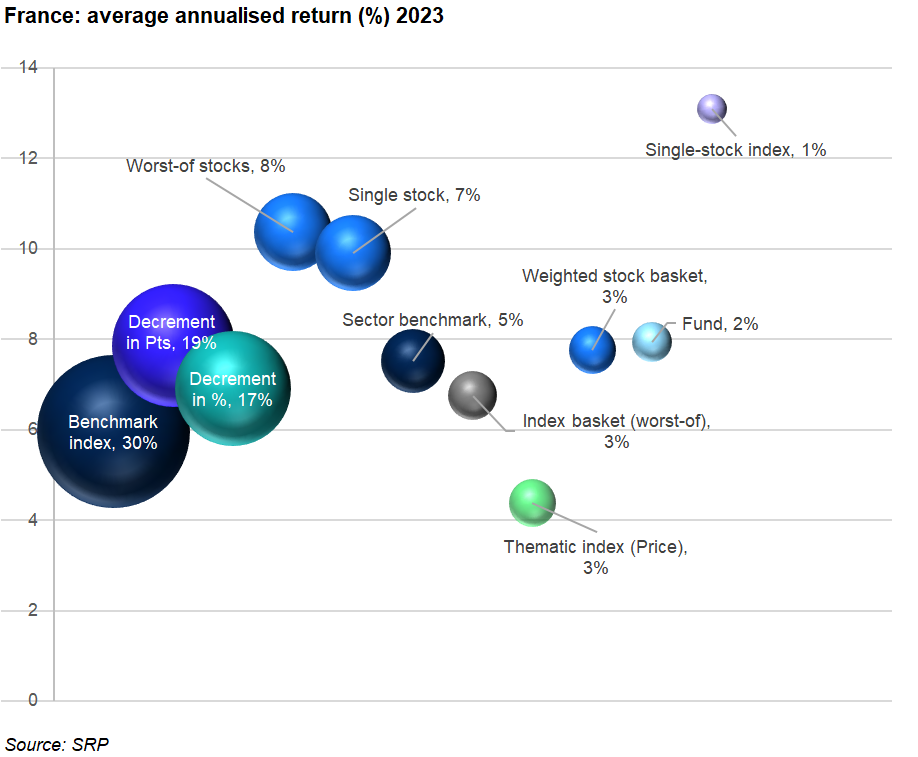

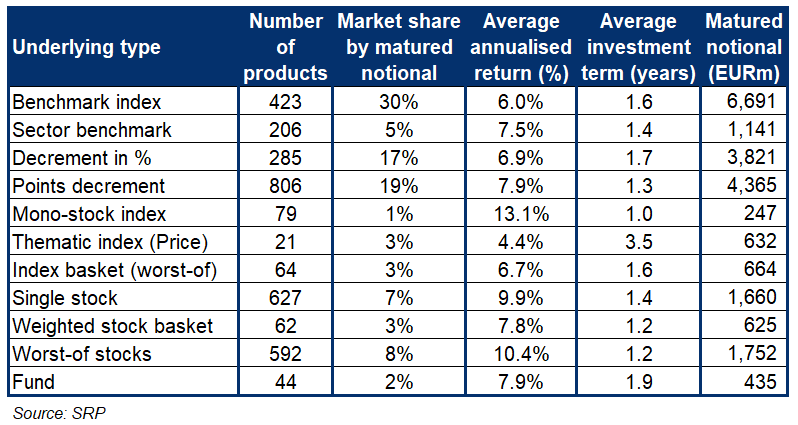

Looking at maturities by underlying type, the analysis shows that products linked to a benchmark index, which represent around a third of all maturities in 2023, delivered six percent (annualised) for an average holding period of one year and seven months, as it can be seen in the chart and table below.

Products linked to a fixed dividend index (Decrement) represented 36% of the matured notional. The split between indices deducting the dividend as a percentage or in points is almost equal notional-wise, while the latter category accounts for almost three times as many maturing products.

Compared to structures linked to benchmark indices, decrement index strategies based on percentage deduction have helped increasing the coupon by one percent and almost two percent in the case of indices deducting the dividend in points. The latter have also demonstrated a 3.5-month shorter holding period compared to a benchmark, as can be seen in the table below.

Well fairing equity markets have benefitted point dividend strategies as the discounted dividend has been decreasing over time. Eventually, this was at the expense of the increased risk of capital loss if the index happened to depreciate.

Products linked to index-wrapped stocks with decrement have showed both highest annualised performance (13% pa) and shorter holding period (one- year).

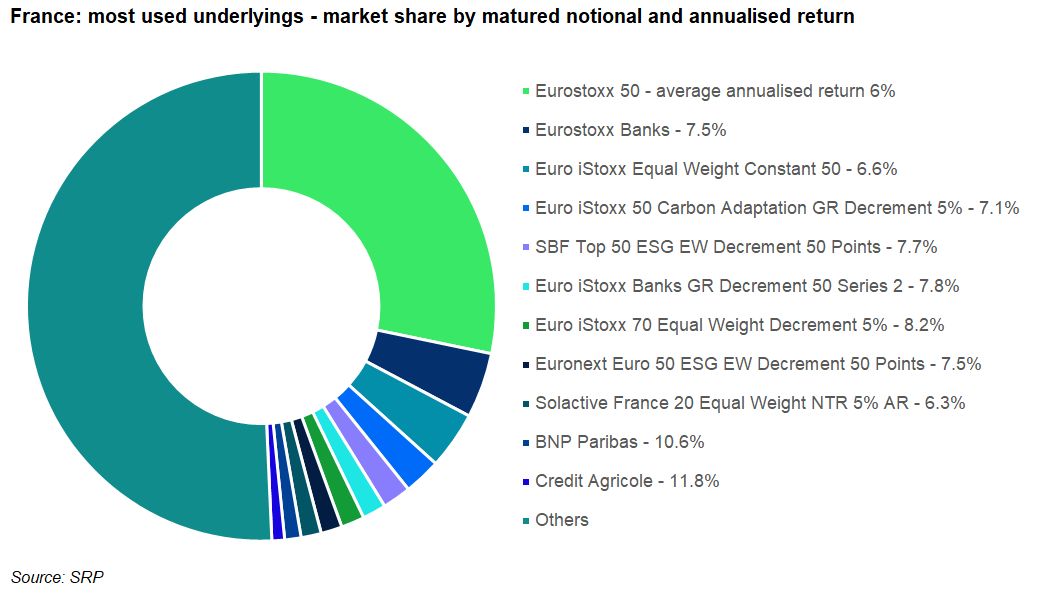

Half of all maturities in 2023 were linked to 11 underlyings (see chart below). The Eurostoxx 50 Index was featured across 12% of all the products matured, representing 28% of the matured notional.

Some 335 products were linked to the Eurostoxx 50 as single underlying. These produced an average annualised return of six percent over an average term of 1.6-years.

The highest index-linked average annualised return (25.4%) was paid out by three products linked to the Euro iStoxx 50 Equal Weight NR Decrement 5% EUR Index from Hedios’ Gamme H series.

Of these, the highest coupon, at 38.75% pa, was paid out by H Performance 44, which autocalled at the first opportunity on 11 July 2023.

Image: Weyo/Adobe Stock.

Do you have a confidential story, tip or comment you’d like to share? Write to info@structuredretailproducts.com