SRP takes a look at some of the most significant developments in the US structured products market during December 2021.

December 2021 was a historic first for the US structured products market as sales volumes for the entire year crossed the US$100 billion milestone. Volumes stood at about US$101 billion and extend over 31,528 products in total.

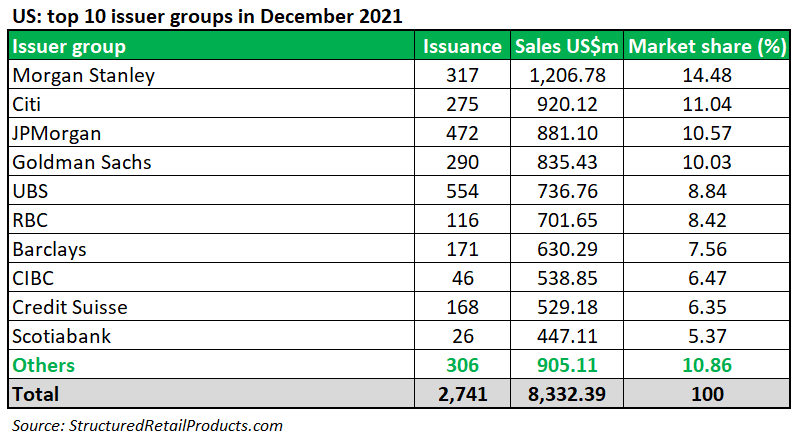

This can be compared with 2020’s total sales figures of US$77 billion for 25,704 products, a 31% increase. Some 2,741 structured products in the US worth US$8.3 billion had strike dates in December 2021. This compares to 2,664 products valued at US$8.9 billion with strike dates in November 2021.

Sales volumes from January to December 2021 fluctuated throughout the year hitting a peak in February (2,734 products/US$9.1 billion), before dropping to an average of US$8 billion per month.

Issuers

In terms of sales, the top US issuer group for December 2021 was Morgan Stanley with US$1.2 billion in volumes across 317 products and a market share of 14.48%. The bank also ranked first during December 2020 with volumes of US$1 billion over 223 products.

Following closely was Citi with 275 products valued at US$920m and a market share of 11.04%, J.P. Morgan with 472 products worth US$881m and a market share of 10.57%. In fourth place was Goldman Sachs with 290 products worth US$835m and a market share of 10.03%, and fifth was UBS with 554 products valued at US$737m and a market share of 8.84%.

In terms of product issuance, UBS issued the highest number of structured products while Toronto Dominion was the lowest of the top 10 in the SRP league tables with 68 products (US$240m).

Payoffs

The reverse convertible payoff type gained the most traction during December 2021 with 1,758 products valued at US$4.6 billion when featured alongside reverse convertible payoffs.

Autocallable structures were also in demand during December featuring in 1,614 structured products worth US$4.3 billion. Accrual structures saw the least traction during the period with just eight products worth around US$20m.

Underlyings

Tesla appeared as a frequently occurring single share underlying in December 2021 with eight structured products worth US$179m. This can be compared with its issuance of 55 products worth US$161m in 2020.

The best-selling structure in December 2021 was the Accelerated Return Notes - S&P 500 (78015B500) which sold for US$84m and was issued by BofA Finance.

With a 22 December 2021 strike date, the growth product has an uncapped call and enhanced tracker payoff type. The note will reach maturity in just over a year and will offer a capital return of 100%, plus 300% of the rise in the index over the investment period, subject to a maximum overall return of 113.07%.

The Eurostoxx 50 index accounted for 51 products worth US$264m while a basket containing Nasdaq 100, Russell 2000, and S&P500 accrued US$779m in sales across 241 products.

Asset class

Equities dominated issuance during December 2021 with index baskets taking the lead across 886 products worth US$2.7 billion. They were also the most popular in the same period of 2020 with 723 products valued at US$2.4 billion.

Exchange-traded funds volumes decreased by 36% to total US$546m (147 products) in December 2021 from US$849m (177 products).

Hybrid structures accounted for US$388m (190 products), a 76% increase from December 2020 volumes of US$219m (85 products).

Two products fell under the interest rate asset class totalling just US$14.2m (two products), while commodity structures accounted for US$15m across five products.