The options exchange concludes that there is no compelling evidence that the growth in products selling options is having a disproportionate impact on the equity volatility market as the decline in equity volatility is in line with other asset classes.

As market dynamics continue to puzzle analysts and commentators about the reasons behind the downward direction of the VIX index which measures the stock market's expectation of volatility based on S&P 500 index options, Cboe's head of derivatives market intelligence Mandy Xu (pictured) believes that "macro fundamentals – which impact all asset classes – are driving volatility lower, rather than anything equity-specific".

"We do not think the growth in option income yield enhancement ETFs or structured products is a primary contributor to the decline in equity volatility," Xu told SRP.

Instead, she points at the "positive shift in the economic growth outlook from recession to soft landing over the past year that’s the main culprit behind the current low vol regime".

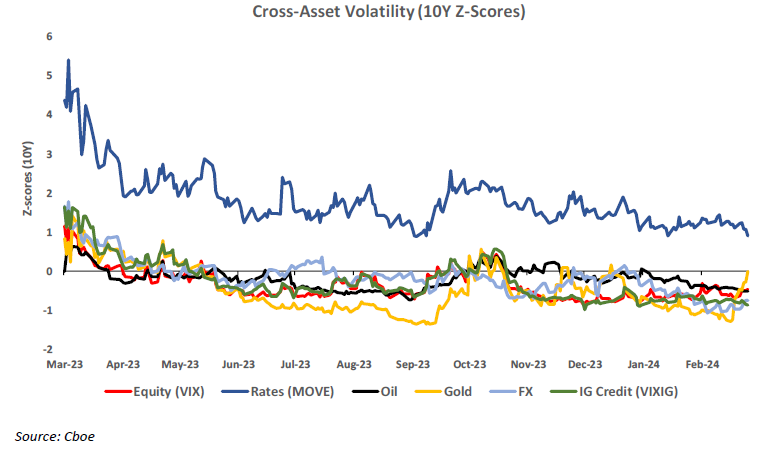

Contrary to a recent report by the Bank of International Settlements (BIS), which concluded that the compression of equity market volatility represented by the fall of the VIX index throughout most of 2023 could have been triggered by option dealers hedging equity-linked structured products, Xu believes that a more compelling reason to think otherwise is that "low volatility is not something that we see just within the equity market, but a phenomenon that we observe across asset classes".

In a recent Volatility Insights update – Are option income funds suppressing volatility? - Xu addressed one of the most common questions that Cboe has been getting since the beginning of the year, which is "why the VIX is so low, and if that has anything to do with the growth in the option income ETF and mutual fund space, which admittedly is a big trend that we are seeing".

The large decline in volatility over the last year or so has led investors and analysts to round up the usual suspects of potential drivers – some see the increasing hedging activity around yield enhancement structured products as a reason but others minimise the impact on the basis that in 2023 there was a shift away from yield enhancement towards principal protected structures, and then within the yield enhancement autocall structures, there has also been a shift away from single name underliers towards indices.

According to Xu, an interesting question is why investors still continue to turn to options for income, when they can get four to five percent per annum from treasuries and eight to nine percent from high yield bonds.

"We think that’s likely to do with option income being a diversifier against fixed income as the two are typically negatively correlated," she said.

Vol selling

Xu notes that there is clearly more AuM going into products that sell options for income and by deep diving into the strategies deployed by these products the specifics of their impact on volatility can be assessed and see if they were having a disproportionate impact.

"First thing we ought to note is that while these funds have grown six times over the past couple of years, from US$20 billion to US$120 billion in terms of AUM, they don't run the same strategies – some are running overwrite or underwrite strategies on the S&P 500, Russell 2000, Nasdaq 100 indices as well as buy-write strategies on single stocks, particularly mega cap tech names," she said.

This means that there is a diversity of underlying indices and tenors with some funds overwriting through weekly options while others use monthly or even three-month options.

Xu added: "The range of strikes, tenors and underliers means that the impact is actually pretty spread out. It's not all concentrated in one-month trades on the SPX, which is what really drives the VIX."

Another important consideration is that if volatility selling strategies such as autocallable products "were getting too big for the broader derivatives market, you would expect to see volatility risk premium in the market shrink".

"That's the difference between implied versus realised volatility, which should narrow if there are more sellers entering the market," said Xu. "But in fact, what we've seen over the past year is the opposite - the volatility risk premium more than doubled from the year before."

Also, according to Xu, if the number of overwriters coming into the market had increased, "the price of the out of the money (OTM) call options would become cheaper relative to at the money (ATM) options which would result on call skew dropping".

This, however, has not happened as over the past year call skew has actually increased with out of the money (OTM) calls becoming more expensive.

"That's because people are buying upside calls to gain tactical leverage into the equity rally and that has been the dominant force in the derivatives market, not call selling," she said.

In other words, it is macro fundamentals that impact all asset classes which boils down to a shift in terms of economic growth outlook what is really driving volatility lower.

Click in the link to read Cboe's Volatility Insights report – Are option income funds suppressing volatility?

Do you have a confidential story, tip or comment you’d like to share? Write to info@derivia.com