Ingenuity is probably one of the most distinctive qualities of the structured product industry.

Its capacity to come up with a solution, no matter the circumstances, is one of its great qualities. Sometimes, however, creativity can become a weakness, as is the case when explaining complex structures is concerned.

What is a decrement index?

Decrement (aka synthetic dividend) indices are optimised gauges tracking a benchmark where the future dividend is fixed in advance. Strictly speaking, they reinvest the dividends paid by companies in the benchmark with a constant dividend markdown expressed as a fixed percentage or index points that are subtracted on an accrued basis. In most cases, this dividend is accrued daily based on the performance of the index.

Decrement indices’ growing popularity stems from their ability to eliminate uncertainty on future dividends, and enable issuers of structured products to offer a potentially higher yield and/or improve capital protection.

The million dollar question is this one: is it worth deploying this complex and innovative product in an investment portfolio?

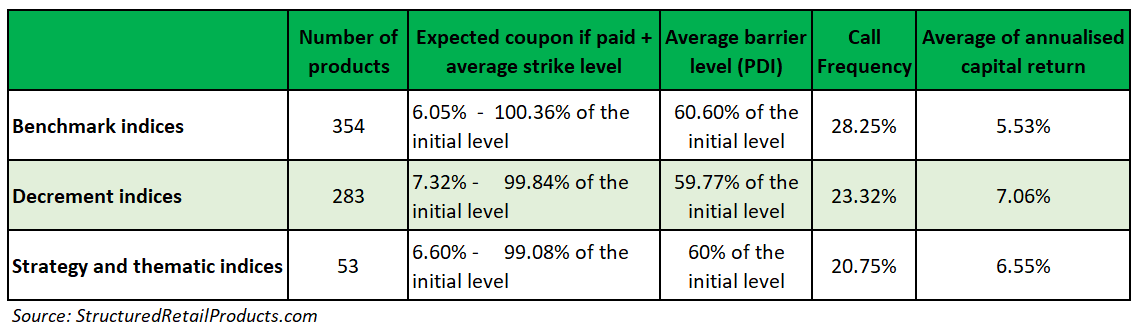

Our analysis of autocallable products sold in France that maturing or knocking out early between April 2018 and March 2019 showed that these products have been delivering what they are supposed to.

Looking at the autocallable market as a whole, with observation dates during this period (expired and live), we observe that structures linked to decrement indices have increased the average headline rate from 6% to 7.3% while growing downside protection by lowering the knock-in barrier level by 0.83% on average.

The most interesting finding, however, is that products maturing early have increased the return to French investors from 5.5% to seven percent, in a market where interest rates are considerably low.

As with any investment however, there is a trade-off that investors accept when opting for products linked to decrement indices. Despite their higher returns, the likelihood of these products being called decreased from 28% to 23% during the 12 months considered. On the other hand, and taking into account the bear market, decrement products have provided significantly better returns in a recovering market, compared with strategy and thematic indices, which featured low volatility and risk control features.

We may conclude, therefore, that decrement indices are an interesting solution for structured products in sideways and bullish market conditions, as they can outperform and deliver good returns. But what happens if markets crash? Will clients understand that the likelihood of getting the product called is lower - and riskier?