Many investors, including large asset managers and institutional ones spend a good deal of intellectual and research effort looking for great and mispriced stocks. While this investing style might have been successful in past decades, it has performed very poorly recently, and even fashionable spins of it, namely factor investing, are performing poorly and dangerously overcrowded.

Instead of focusing on finding the perfect stock or index, which rarely exist, investors should focus on designing the right payoffs and linking them to most stocks and indices, even the very average ones. This approach guarantees higher returns and lower correlation to traditional assets and market cycles.

Albeit needing a certain derivatives expertise, this approach can be implemented through a rigorous rule based framework, be quasi-market neutral by design and above all lead to much better risk-return profiles.

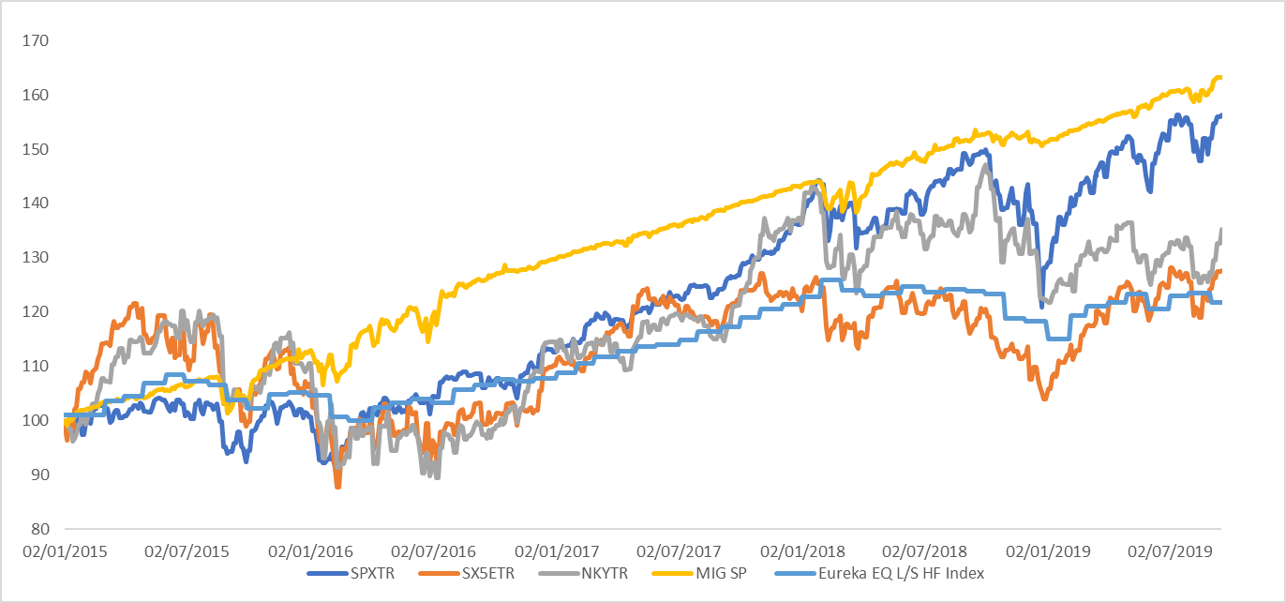

To illustrate this, below is a graph (Source: Bloomberg/Mount Investment Group) showing over the last five years the total return performance of the main developed markets equity indices (SPX, NKY and SX5E), as well as the Eureka Hedge equity long short index versus the performance of the Mount Investment Group's proprietary structured product strategy linked the these same developed market equity indices. The MIG SP strategy's sharp ratio is 1.36 versus a range of [0.13-0.37] for the other indices, and its max drawdown is 4.23% versus a range of [18.9%-28.12%] for the developed market indices. The max drawdown of the Eureka Hedge L/S index, of 8.65%, is based on monthly levels and most likely is higher if daily prices are available. The MIG strategy is implemented through standard liquid payoffs but is designed to generate higher yields and protect capital through most market trajectories. This design also creates a pull to par effect that allows it to limit and recover from drawdowns very quickly.

Structured products is a big business. Sitting at around $4.5 trillion outstanding notional, it is more than double the hedge fund industry. While most of the demand is driven by private wealth management, institutional investors and hedge funds are, unfortunately for their clients, not yet making allocations to this asset class even as it has become highly commoditised with compressed margins and ample liquidity.

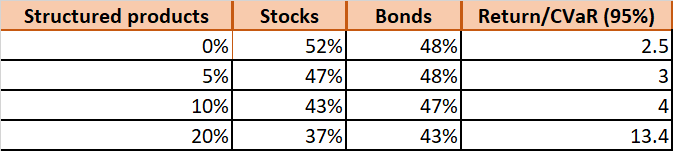

Structured products are not only a great tool to extract much higher yields in a low rates environment, but they are also a superior way that allows investors to extract multiple premia at once while guaranteeing a defined return profile. Multiple academic papers have demonstrated that structured products beat stocks-bonds Markowitz portfolios and are in fact an excellent diversifying tool that increases efficient frontiers. The table below summarises the findings of an EDHEC Research Centre’s case study on the benefits of structured products allocations and show how increasing allocations to this asset class dramatically improves the risk-return profile of a portfolio.

Savvy money managers frustrated with the poor performance and crowding of traditional strategies should be allocating to liquid structured products strategies. Payoff design capabilities allow the creation of positive carry and positive convexity portfolios that are impossible to achieve without the use of the derivatives technology. They also monetise multiple premia and benefit from banks' more stringent balance sheet requirements.

Talal Dehbi is founder and CEO of Mount Investment Group.