US investors have a long history of using US equity indices as a vehicle to access equity exposure.

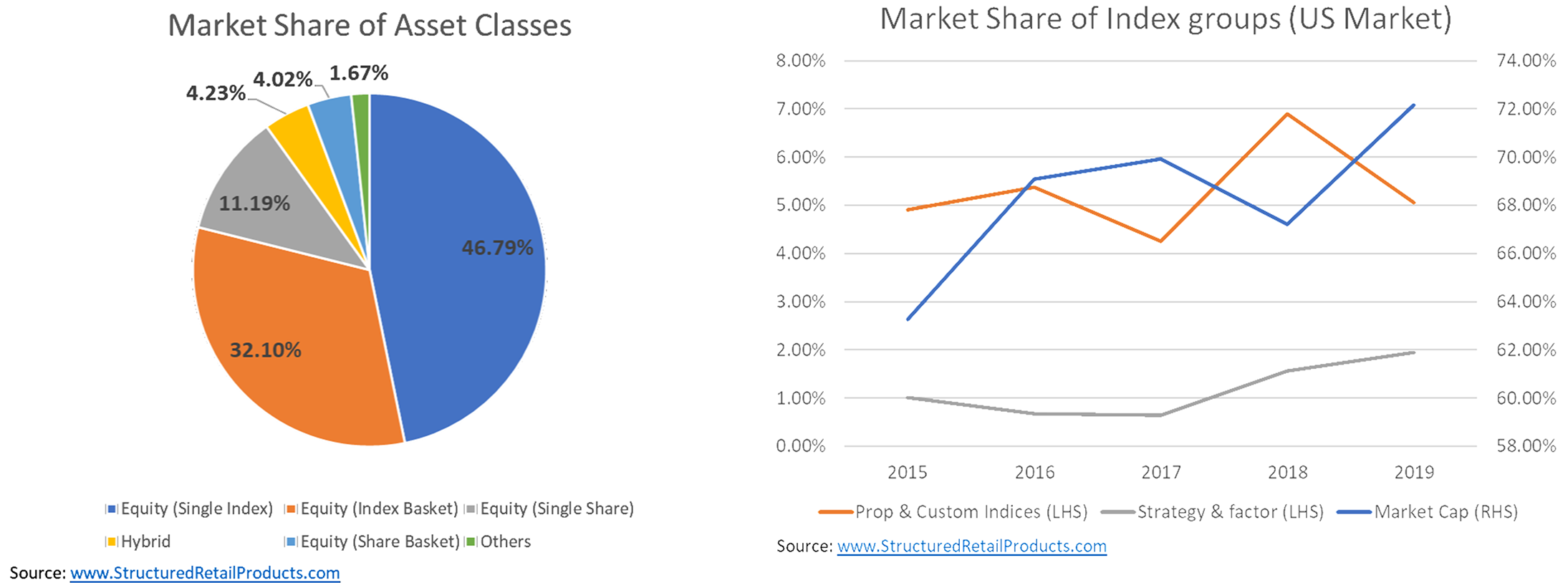

The US structured product industry has also used this approach extensively, with US equity indices representing more than 80% of all the US structured products market volume sold in 2019.

For the past five years, the market share of US indices has increased by 13%, with strategy and factor indices doubling their size to two percent over the four years ending 2019. For their part, market cap indices have grown 13%. However, while proprietary indices increased their market share until 2018, they have declined since then due to underperformance over the last 18 months. Proprietary indices now account for five percent of all products sold in 2019, a similar level to 2015.

To understand if it is worth investing in index-linked products we have to look at their historic performance. SRP analysed the performance of 18,654 index-linked products between 2010 and 2019.

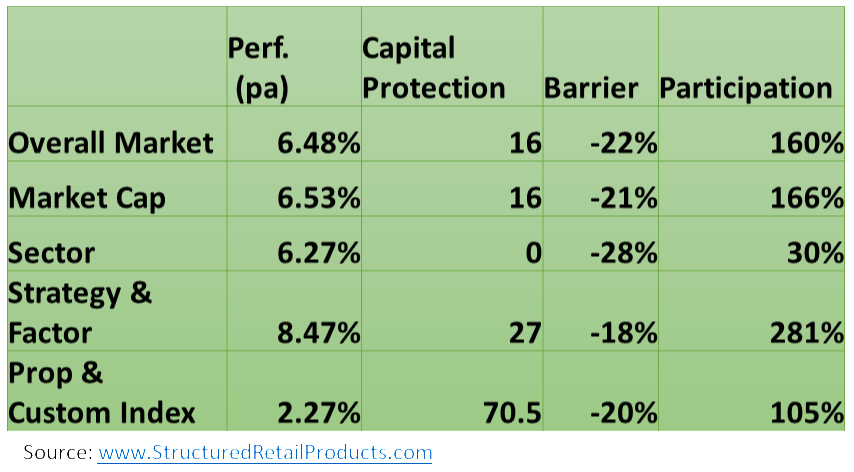

The research found that, overall, index-linked structured products provided an average return of 6.5% pa, offering capital protection of 16%. When comparing the performance of the different index categories, strategy and factor indices outperformed market capitalisation indices by almost two percent pa.

The research also unveiled that different index groups have grown to be more complex because of their ability to improve capital protection or participation/yield on structured products.

Looking at the features of matured products, the research found that strategy and factor indices increased capital protection from 16% to 27%, and participation from 166% to 281%. Proprietary indices are primarily used as underlyings on capital-protected products, using features such as risk control or a mix of asset classes to offer capital protection. The average performance of these products, at 2.27%, was much lower.

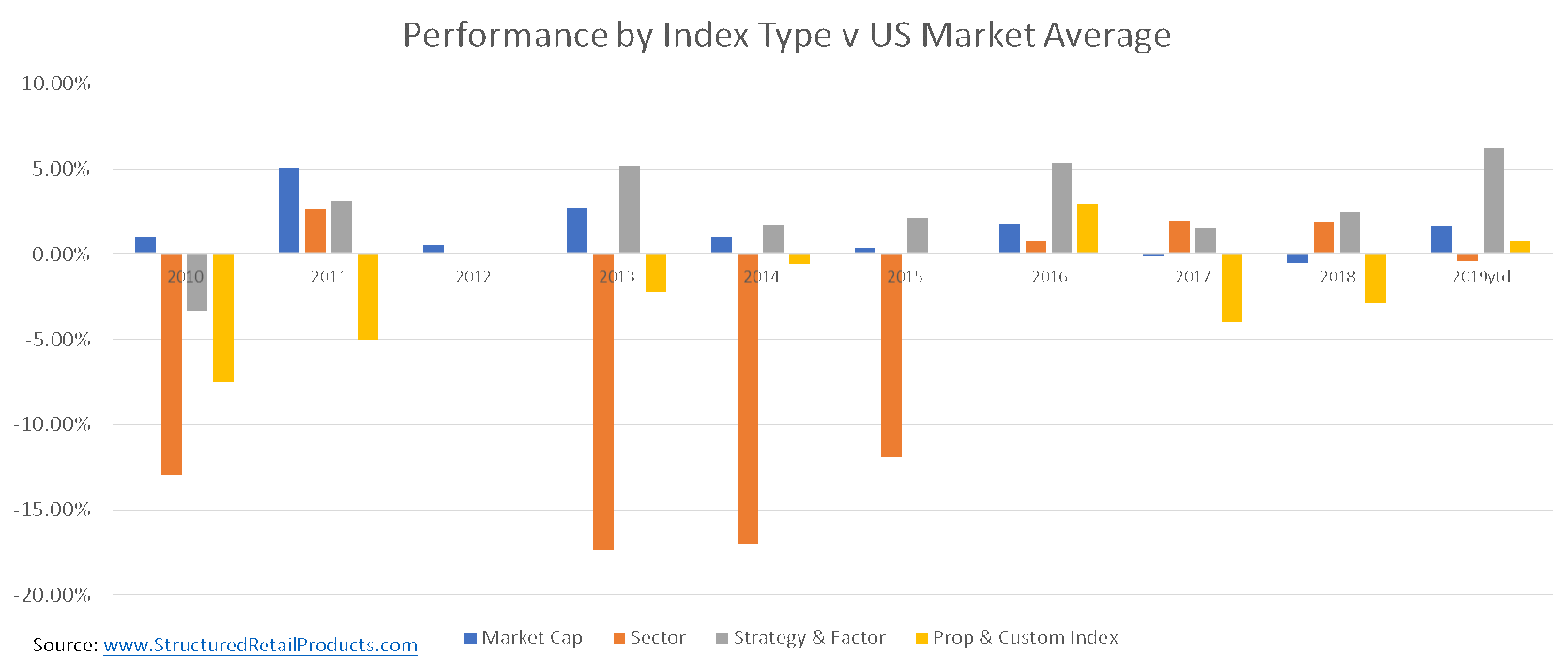

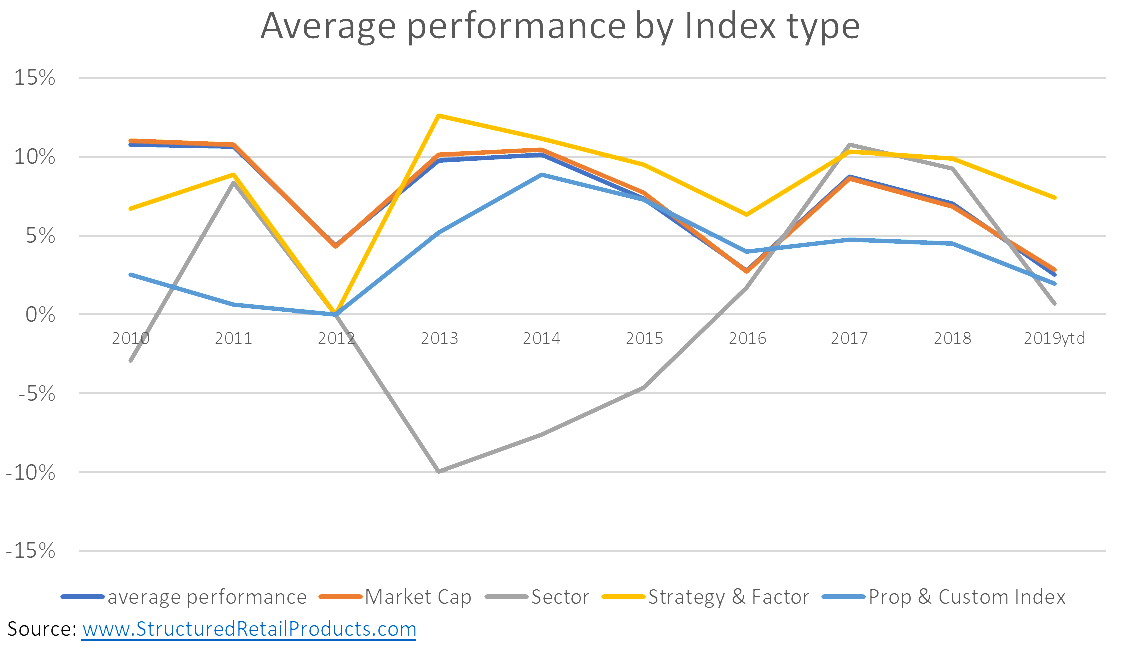

When it comes to performance, the research shows that the performance of sector-linked products is much more volatile. Products linked to the banking sector and commodity indices (with a special focus in energy), delivered a negative performance between 2013 and 2015. Only strategy & factor indices (including quality, value, growth, size, dividend, momentum and volatility factor indices) have performed well since 2012.

Looking at the relative performance of the different types of indices versus the average return offered by structured products, we can conclude that US investors have benefited positively from using US indices, which have been favoured over stocks and other asset classes. Another conclusion of the research is that diversification and factor investing, when used to improve structured products features such as capital protection or participation, are providing value.