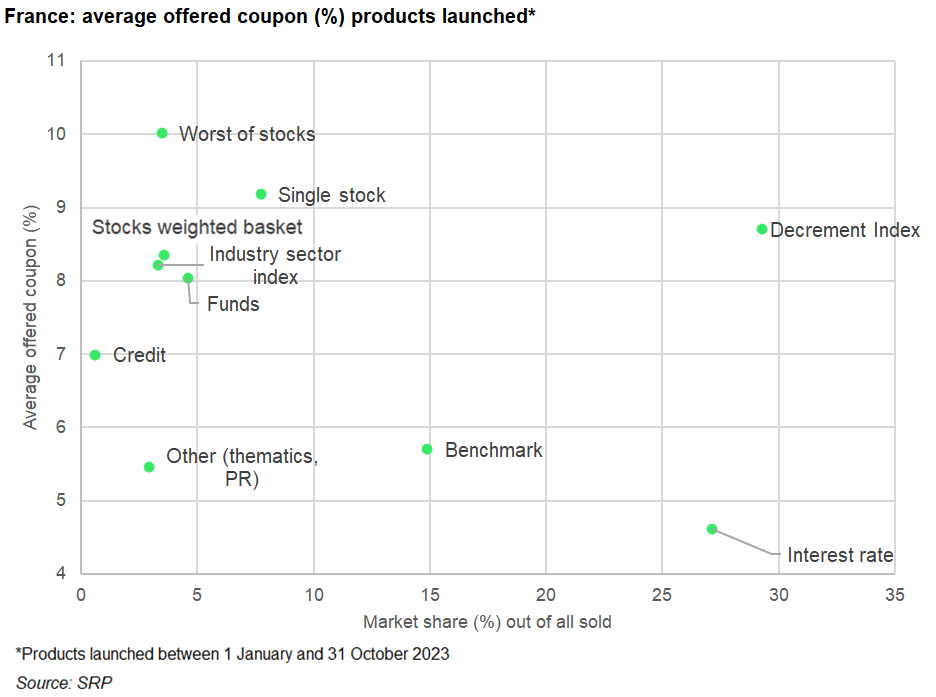

The average offered coupon reached 8.1% during the first 10 months of 2023 with products linked to a worst-of basket of stocks the most generous.

An estimated €34 billion (US$37 billion) was collected from 4,254 structured products that struck in France during the first 10 months of 2023 – up 32% by sales volume compared to the same period in 2022.

The highest average coupon, at 10% pa, was attached to products linked to a worst-of basket of stocks, which captured a 3.5% share of the market in 10M2023

Although the increase in sales volumes was largely fuelled by a higher rates environment allowing for the comeback of capital guaranteed products, the yield enhancement segment has remained relevant for investors seeking to remain invested in equities and protected.

Autocalls claimed just under 60% of the French market by sales volume (and approximately 75% by issuance) in 10M2023; other coupon paying products included callable fixed rate notes (19% market share), digitals (5.1%), and barrier reverse convertible (2.5%).

The average coupon offered by products launched between 1 January and 31 October 2023 stood at 8.1% compared to eight percent in the prior year period.

The highest average coupon, at 10% pa, was attached to products linked to a worst-of basket of stocks, which captured a 3.5% share of the market in 10M2023. During 10M2022, the average coupon for worst-of stock baskets was also 10% pa, although back then their market share, at 5.10%, was slightly higher.

Examples of such products include SG Issuer’s Phoenix Plus Worst Of, which pays a fixed coupon of three percent for every quarter the underlying shares of Société Générale and Bouygues close at or above 60% of their strike price, and BNP Paribas’ Phoenix Memoire which offers 9.8% pa providing the shares of Shell and Total Energies close at or above 50%.

The average offered coupon for products linked to an industry sector benchmark index is 8.2% pa, much higher than the 5.5% pa on offer for structures on thematic price indices, although the market share of both categories is relatively small: 3.3% vs 2.9%.

Products linked to benchmark indices, which held 15% market share, offered coupons of 5.7% on average while structures tied to synthetic dividend indices, the largest category by market share (29%), are due to deliver average coupons of 8.7% pa.

The latter category includes Goldman’s Elae Tempo Banques Avril 2023 on the S&P Eurozone LargeMidCap Banks (Industry Group) 50 Point Decrement EUR TR Index and BNPP’s Exigence 18C on the Bloomberg Transatlantic Titans 40 Decrement 50 Points Index, which offer a coupon of 9.8% pa and 7.5% pa, respectively.

Notably in the above category, single-stock decrement indices offer an average coupon of 11.6% pa, 2.4 percentage points higher than the 9.2% pa offered by products linked to a pure stock, although their investment horizon is twice as long: 10-year maximum investment term for products linked to single stock decrement indices vs five-year for their single stock equivalent.

By payoff type, the highest average coupon is offered by conditionally protected knock-in barrier autocalls (9.3% pa).

Looking at the conditionally protected index-linked offering over the period, we observe that structures linked to decrement indices have increased the average headline rate from 5.9% to nine percent while increasing the downside protection – lowering the knock-in barrier level by 0.3% on average and increasing the investment tenor from five to 10-years.

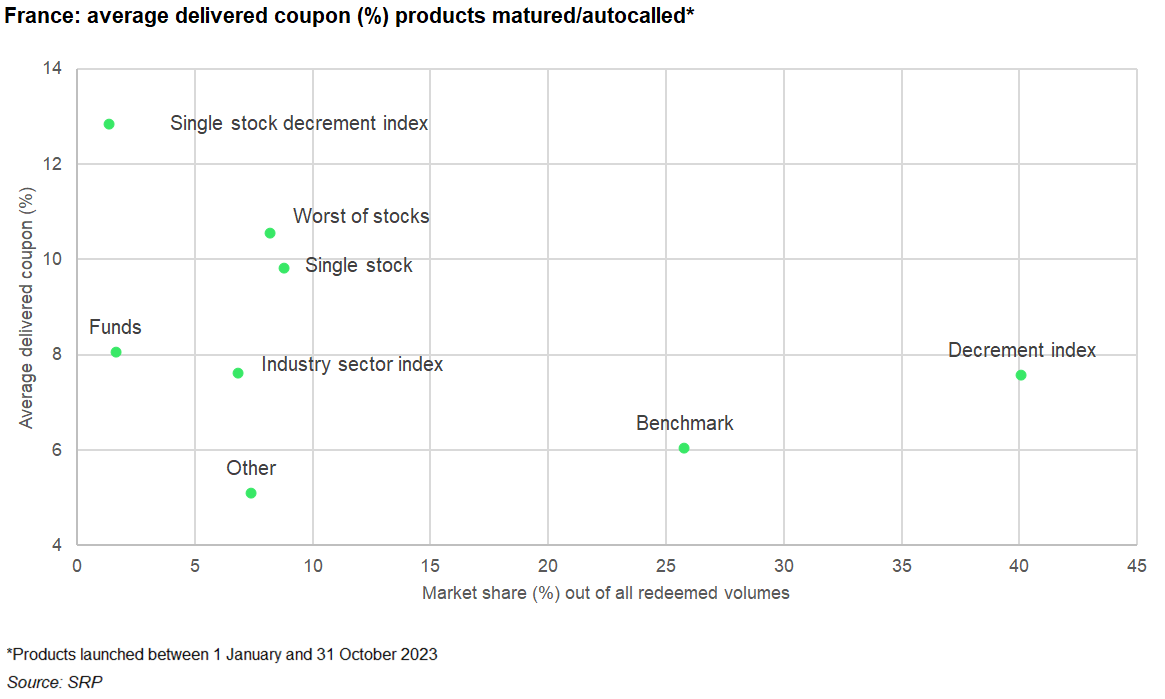

It is also worthwhile to draw a parallel with the average returns delivered by the 2,850 products that matured or autocalled during the period - the highest coupon paying products were those linked to single stock decrement indices. On average, these structures returned 12.9% pa, despite having a market share of only one percent.

Two of the most seen single stock decrement indices were the Euronext G Credit Agricole 010621 GR Decrement 0.9 Index and iEdge Orange SA Decrement 0.8 EUR GTR Series 1 Index.

The former was used as the underlying index for Goldman’s Frequence Privilege Crédit Agricole 2022, a 10-year autocall which knocked out after one year, returning 115.20% of the nominal invested. Another autocall, this time issued on the paper of Natixis, returned 117.52% – also at the first time of asking – after the iEdge Orange SA Decrement 0.8 EUR GTR Series 1 Index closed at above its initial level on 15 March 2023.

Products on worst-of stocks and those tied to single stocks delivered average annual coupons of 10.6% and 9.8%, respectively, while fund-linked structures reached 8.1% pa.

The average delivered coupon for products linked to benchmark indices, which were responsible for 26% of all redeemed volumes, registered at 6.1% pa, while decrement indices – the biggest category by redeemed volumes (40% market share) – delivered an average coupon of 7.6% pa.

The best performing product in this segment was H Performance 44, a 12-year autocall from Citi on the Euro iStoxx 50 Equal Weight NR Decrement 5% EUR Index. It was distributed in France via Hedios Vie and, because the index increased by more than 10% on the first valuation date, returned 140% after one year.

Main image: Pic3D/Adobe Stock.