Despite the dominance of equities and interest rates in the market, FX products have established themselves in many markets as opportunistic investments and for hedging purposes.

Equities and fixed income are the most common asset classes for structured products. This is to be expected since equities, indices, bonds and cash are the most important investment vehicles. However Foreign Exchange (FX) linked products represent an important niche area that attracts a decent volume of issuance.

FX structured products are often used for taking speculative positions, or for hedging purposes

The logic of the use of FX has some similarities with interest rate linked products. Both these asset classes are broadly held to be “mean-reverting” in that a long-term trend is not expected very often, unlike equities which is the asset class that investors look to for long term returns tied to the growth of an economy to beat inflation.

FX structured products are often used for taking speculative positions, or for hedging purposes. In both of these cases product maturities tend to be quite short in order to capture a particular view or hedging requirement.

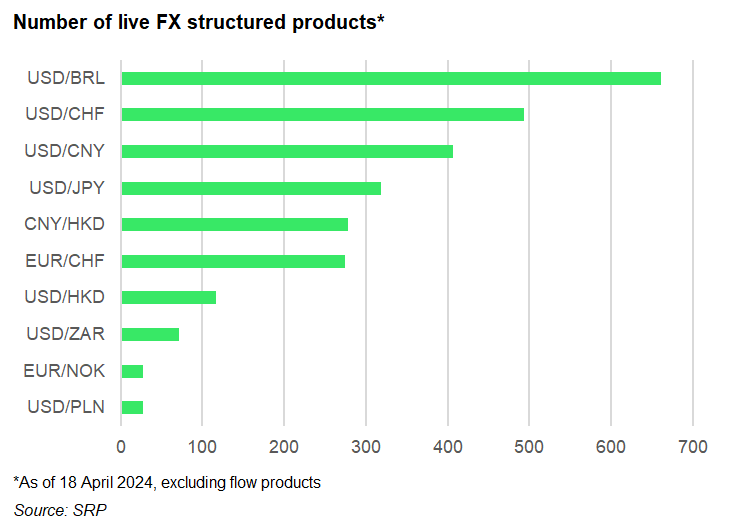

The list of popular FX pairs below is dominated by those involving the US dollar (USD). Top of the list is USD against the Brazilian real (BRL). Brazil has a large economy and an active structured product market. The higher levels of Brazilian interest rates combined with historical weakness in the FX rate and the geographic proximity of the two countries explains the high number of FX structured products in the market.

Country breakdown

Typical product types in Brazil are the dual directional and digital. The dual directional pays the absolute return of the FX move in either direction subject to a cap. The digital will pay a fixed amount if the rate moves in the right direction. Usually this will be if the BRL weakens against USD and products are generally capital protected and denominated in BRL. Therefore, these products offer a partial currency hedge against BRL weakening, important for local investors.

Other currencies against the USD are Swiss franc (CHF), Chinese yuan (CNY), Japanese yen (JPY) and Hong Kong dollar (HKD). These currencies are important regional choices, and their respective economies will be influenced by the US market and the performance of the FX rate.

There are many products in the Swiss market issued as either discount certificates or reverse convertibles which will benefit from a currency move between USD and CHF, offered in either FX direction. The maturities tend to be less than two years.

Switzerland also accounts for most of the issuance of USD/JPY linked products, with shorter maturities of three months or less. This gives the opportunity for speculative currency investing if the investor has a strong view.

Products linked to USD/CNY are also very short dated (six months or less) and denominated in HKD for the Hong Kong market. There is issuance for both Bullish and Bearish directions, therefore investors can benefit either way if their view is correct. Such products are tactical in nature which is a popular way to invest in Hong Kong generally.

The two most popular FX pairs not involving the US Dollar are EUR/CHF and CNY/HKD. These are both regional plays for the smaller economies of Switzerland and Hong Kong versus the Eurozone and China respectively.

The EUR/CHF products originate mostly in Switzerland and are very similar in design to the JPY issuance in the same market having a very short maturity. Switzerland with its large certificates market offers many products in a range of currency pairs.

By contrast, the CNY/HKD linked products are mostly issued in Hong Kong and are capital protected with some FX exposure. These are rather longer and can be up to one year in maturity.

Like interest rates, FX rates also play an important role in many structured products not directly linked to them. In the case of interest rates, the prevailing level of the risk-free rate influences product maturity and product type because of the effect of discounting payoffs at a higher interest rate, making the construction of capital protected products easier when the risk-free rate is higher.

FX rates also influence equity linked products when the underlyings are in different currencies to the product payoff. For a EUR denominated structured product linked to the Eurostoxx 50 and S&P 500 for example, the index performance of the S&P 500 needs to be calculated either in index performance alone (“Quanto”) or by calculating the index performance converted into EUR (“Composite”).

The level of interest rates in the payoff and underlying currency will help to determine which is more popular although Quanto is generally the more common so that investors can isolate index performance.

Reflecting its importance in world economies and markets, the FX asset class offers a range of direct investments in many countries and indirectly feeds into other asset classes and product types.

Image: Tierney/Adobe Stock.

Do you have a confidential story, tip or comment you’d like to share? Write to info@structuredretailproducts.com.