JP Morgan has been an active issuer of structured products 'though various channels" in the Dach (Germany, Austria, Switzerland) region for over 10 years. However, SRP data shows that the US bank has become increasingly active in the retail structured product market over the past year and has over 100 live products in Germany, and 187 in Switzerland. SRP spoke to Marcel Biere (pictured), executive director, head of German distribution at JP Morgan in London, to find out about their plans in the region with a focus on issuance, market trends and challenges.

JP Morgan uses different distribution channels in the Dach region with a range of non-listed products as well as a suite listed on the Stuttgart and Frankfurt stock exchanges, however, the majority of the products are distributed via large private banks in Germany and Austria. What other distribution channels is the bank covering in the region?

Private banks have typically been one of our major distributors and they themselves use their various pan European distribution channels. That is why our products are increasingly offered simultaneously across Germany, Austria and Switzerland. These issuances can be listed at the local exchanges, whereas the majority of our private placements are not listed. Beyond private banks, our other distributors in the region include a number of asset managers and regional banks as well as IFAs who frequently engage with us. In all cases, our products are sold via a distributor, so we are not facing the end-client directly.

Products with NL-Isin codes are usually in the form of certificates, whereas products with XS, DE or CH-Isin codes are notes, and are issued out of JP Morgan BV, our issuer for retail structured products based in the Netherlands.

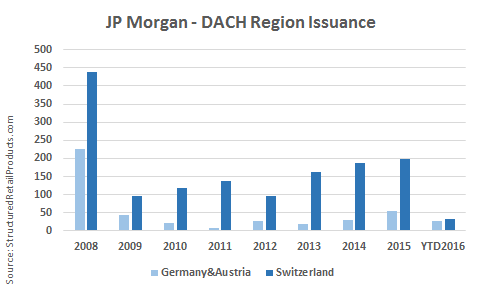

According to SRP data, JP Morgan's issuance is higher in Switzerland than in Germany. Is there a stronger focus in the Swiss market?

In Germany, the vast majority of investors are self-directed and purchase structured products directly from the exchange, whereas a large portion of the traded notional falls within the warrant/day-trader segment. While we see good demand from German private banks and asset managers beyond the listed space, the Swiss private banks tend to demand more products that are made to order.

After the initial market shock of the credit crisis, we have increased our issuance in Germany over the last few years as, when investors returned to the market, they saw that a more conservative mix of structured products was a good way to enter equity markets.

What's JP Morgan's differentiating factor in such competitive markets?

In the retail structured products space, we are able to serve our clients on all kind of structures and underlyings, and we always try to be as innovative as possible. However, innovation is quite difficult as regulation has become more defined - so it is as much about service, speed, idea generation on popular products, and showing the right use of yield enhancement products. One of the key-strengths of JP Morgan has always been in serving the client from an asset allocation and strategic angles to complement their conventional portfolio allocation. It seems to be really appreciated where we combine research with new initiatives run by our structuring and trading desks. Our risk premia based products have also seen a lot of interest from our clients - private banks as well as asset managers use our products in that space as an additional source of diversification for their portfolios.

We try to adapt to the market, and automate any flow that is reoccurring in an efficient manner. We also have [implemented] initiatives to streamline our issuance and pricing processes, and therefore we were able raise higher volumes than in the past. Obviously, there are costs involved in issuing and structuring these type of products to serve clients, and we have focused on driving down our own costs to become more efficient in doing that.

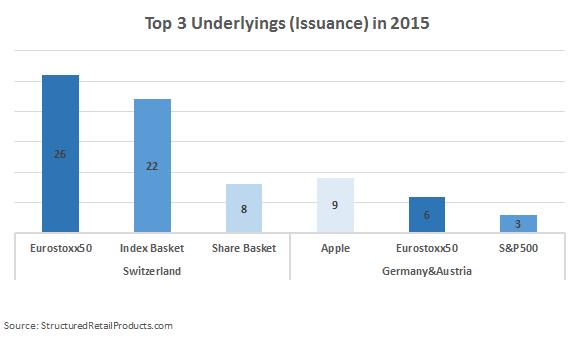

SRP data shows that the Eurostoxx50 index and the Apple stock were the most used underlyings in 2015. Why do you think these assets had so much traction?

[The Eurostoxx 50 [index] is probably the most used underlying for structured products in Europe as it's a benchmark for many investors. For single-stocks, we have seen significant interest in German and Swiss blue chip names as well as in the US. For the latter, investors have been particularly keen to gain exposure to "lifestyle" stocks like Apple and Facebook.

What underlyings do you think will drive most of the activity this year?

It is always difficult to forecast what kind of underlyings we will issue structured products on ahead of time, but recently we have seen a pick-up in demand for stocks with dividends and lower volatility. Apart from this, environmental and sustainability focused topics are a growing area, so the whole ESG topic (environmental, social, and governance) is certainly a topic where we invest and see opportunities for our investor base. Our recently launched JP Morgan Ethos Investments platform will allow us to serve our clients even better with a holistic approach in that space.

What is the difference in underlying trends in Germany and Switzerland?

Historically, Germany has been focused on domestic German single names and underlyings (Dax, Eurtostoxx 50), while in Switzerland the focus is more international. There is more interest in Switzerland for US underlyings, and the range of different underlyings is higher than in Germany. The Swiss market tends to be faster to adapt to new underlyings/innovations which we have noticed particularly within the smart beta space.

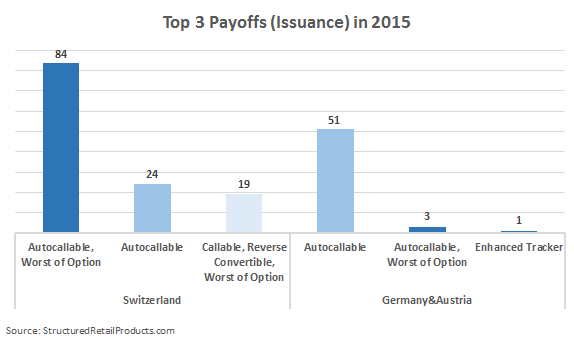

Over the last few years, autocallables have dominated the payoff landscape. Do you see this dominance changing any time soon?

Last year, investors in Switzerland and Germany have mainly been interested in so called autocallables, which stand more than any other product type for the investor's aim of yield enhancement in a low rate environment. It has been all about coupons rather than investment into beta-type products.

What are the challenges and chances you see in Germany and Switzerland in the future?

To interact further with our client base, I think there is a huge opportunity to engage more on asset allocation, which is a more strategic way of thinking rather than just advising on the tactical use of structured products.

Certainly there is a degree of margin compression in an environment that thrives for platform-solutions as well as standardizing product offerings. If you are not keeping up with the technology to support this, then that is a business threat. However, we are very aware of this, that it requires investment from day one, and it has to be offset with expected future revenue.

In terms of Fintech what are you involved with at the moment?

Fintech is and will be increasingly important in the future. Take, for example, the platforms with multiple dealers in Switzerland that have gained popularity in the recent years. We are in discussion with clients about where they would like to see us in future. We are already on Vontobel's Deritrade platform and we are in discussion with other venues too.

What's your forecast for the market?

A structured product is not what it used to be - a complex one-off investment. It is now what I'd call "light structured flow" and it is likely to be even more flow-based in the future (at least when it's about distributing on an advisory basis). That will be especially the case in Germany where the requirement for documentation has increased significantly now that the room for innovation is very limited. So in that market, it is all about standardised and automated payoffs.

Is regulation impacting your day to day business in any way?

Mifid2, the reporting and the auditing, is important and will become more important in the future. You need to serve clients in a way that makes it easy for them to serve their own clients, without over-stretching resources in the process. Fintech will be part of the solution to this and will only have more impact on the structured products market.

JP Morgan dispatches ESG-focused investments platform

Lyxor deploys JP Morgan factor strategies

JPM joins Deritrade multi-issuer platform in Switzerland

JPM teams up with World Bank for new green bond

JP Morgan's Nexus platform doubles trading activity in a year