The Swiss structured products market is one of the most developed markets in Europe with a turnover of CHF235.1bn (€216bn) in 2015 and CHF66.2bn in the first quarter of 2016. Around 65% of the products are targeting institutional investors, 30% private banking and 5% are retail; non-listed products represent 73% of the issuance while exchange traded products took 27% market share in the first quarter of 2016, a decrease of 5% in comparison to last year figures, according to the Swiss Structured Products Association (SSPA) which released its first quarterly statistics earlier this year.

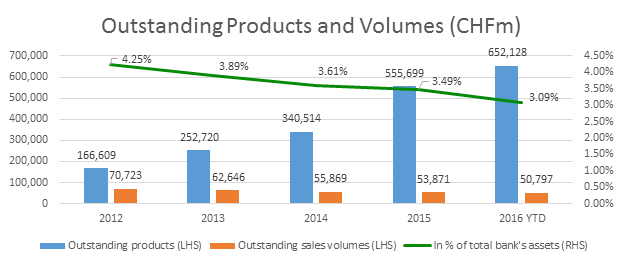

According to SRP data the gradual increase in product issuance has been offset by decreasing sales which reflects a market shift towards increased issuance of leverage products which often generate a lower sales volume. The same trend is visible in the falling percentage of structured products within the total assets held by Swiss banks.

Increased volatility and uncertainty in the capital markets has pushed Swiss investors to become more cautious towards their investment strategies, according to Adrian Steinherr (pictured), managing director derivatives distribution at UBS bank. "Markets continue to be dominated by low interest rates and political uncertainty, especially in the EU and the US," said Steinherr. "Therefore investors [have become] less active and foster more a 'wait and see' philosophy. This [has led] to reduced double digit volumes year-on-year in structured products in Switzerland. "

Source: StructuredRetailProducts.com, SNB Monthly Statistical Bulleting

The total number of issuers in Switzerland stands at 27 with Vontobel, Leonteq Securities, Notenstein La Roche, Credit Suisse, Julius Baer and UBS taking the lion's share with a total retail products sales volume of CHF9.8bn in 2016YTD.

Despite the fall in activity, the Swiss market remains at the forefront of developments around automation and click and trade platforms. Vontobel, the leading provider in this segment with its deritrade platform has reported a volume increase of 267% YOY, and continues to develop add-ons such as SmartGuide, a customised decision making tool based on smart and crowd data. Leonteq is also pushing its partner's platform business which generated a 40% increase to CHF8.7bn in Q1 2016 and has already plugged-in seven issuers; and UBS has also bolstered its Neo platform for actively managed certificates (AMC). "Our AMC platform continues to grow and attract attention," said Steinherr.

The most recent development in the platform segment came from Six Swiss Exchange which hard-launched its over-the-counter platform, XBTR, in April with Leonteq and Credit Suisse executing the first trades. Single and multi-reverse convertible structures, as well as reverse convertibles with callable or autocallable features remain the most popular payoff types due to the conditional capital protection and income coupon payments. "Investors are evaluating market opportunities more carefully and are still seeking alternatives to low yields," said Steinherr. "Swiss investors continue to be very active in multi and single barrier reverse convertibles. The current trend is to trade lower barrier multis, rather than higher barrier singles, effectively reducing market risk at the cost of added correlation risk."

The introduction of the lock-in feature in the typical barrier reverse convertible structure brought some innovation in the product offerings and attracted investors' interest. This structure offers the possibility of turning into a 100% capital-protected product when the underlyings close above a specified level. A product with such features was first introduced in 2008 by JP Morgan but the issuance of lock-in barrier reverse convertibles spiked in 2015 with 83 products added to the SRP database.

Another typical Swiss product is the Outperformance Bonus certificate, with a payoff enhanced tracker, protected tracker, which offers participation in the development of the underlying, has a specified bonus and a barrier level. In case of no barrier event, the investor receives at least the bonus level multiplied by the denomination with a possible leveraged participation in the performance if the final level of the product is above its initial. In 2015 and 2016 this type of product generated a sales volume of CHF462m with ABB, Credit Suisse, Roche, Nestle and Syngenta being the most preferred underlyings.

One of the more unusual products was the Buy on Dips note/Drop Back certificate based on a combination of portfolio insurance and range payoff types. This type of product is offered by UBS, Credit Suisse and JP Morgan. The structure reallocates capital from cash to equity in case a trigger event takes place. At maturity, the investor participates in the performance of the underlying and receives a conditional coupon on the capital invested in the cash account.

Recently, Notenstein started offering autocallable barrier reverse convertibles with a new coupon feature, Lock'n'Roll- which pays the full coupon which the product offers during its term even in case the product matures early. Thus, Swiss investors are lured by the higher annualised yield in case of early redemption.

In terms of underlyings, Swiss investors have a home bias towards domestic assets such as the Nestle, Novartis, Roche basket, which are the most popular underlyings in the market. Since 2015 there has been an increased interest in oil-related underlyings which began to be deployed in bearish inverse reverse convertible structures. Towards the end of last year an increased demand for safe-haven commodities, such as gold, palladium and silver, appeared with demand from both retail and institutional investors. The trend continues after the Brexit vote with a spike in demand for FX and precious metal related products. "Over the last weeks we have seen increasing demand in leverage products [linked to] gold and USD/CHF, said Steinherr. "It seems investors are getting slightly away from so called mega trend themes and are again more interested in traditional investment stories like family businesses. We've seen some good flow in our tracker certificate on Global Family Companies Index (FAMUSU)."

According to Steinherr, current market conditions are challenging for the whole industry. "Volumes are down, and so are revenues," said Steinherr. "Increased regulation requirements such as the packaged retail and insurance-based investment products (Priips) or the US treatment of dividend equivalents- 871m will bring new difficulties for the structured products market players. "We are currently in the final steps for the Priips-Kid implementation going live at the end of this year. Although this is mostly effecting our EU business, this will also become important for the Swiss market soon."

The Swiss market continues to be focused on increased transparency and the SSPA began publishing quarterly market statistics with detailed figures for both the listed and non-listed products segments. SSPA is also pushing financial education by offering a new app which explains the use of structured products in a more comprehensive and user-friendly way with simulations of market conditions and investment strategies. "Product transparency and education are essential to further increase the confidence and to allow investors sustainable and profitable investments," said Steinherr. "Client education is something very important to us and for the structured product industry."

Notenstein offers music to investors' ears with Lock'n'Roll certificates

Volatility drives shift to low barrier reverse convertibles, SIX readies OTC platform

Swiss sales of commodity-linked products rise

Leonteq to refine 'organization and strategic priorities' as growth slows down

Vontobel's Deritrade notional volume up by 267% YOY