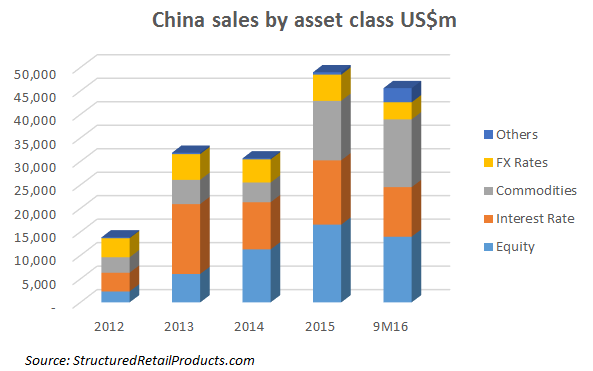

Commodities have edged ahead of equities as the most popular underlying for mainland China's structured products investors in the nine months ended September 30, according to the SRP database.

While the overall issuance is on track to beat the record sales volume for 2015, commodities is the only asset class that has seen its share of the structured products market increase from last year, to account for 32% of total sales in the first nine months of 2016.

Commodities and precious metals are likely to remain the focus over the next 12 months, especially in China and in the Asia Pacific region, according to Vincent Yeung (pictured), deputy general manager of the asset management department at China Merchant Bank (CMB). "Judging by product data since 2015, as CMB has been launching structured products linked to both London and Shanghai gold fixings, the reception to the latter has been encouraging. Geographic proximity and renminbi quotation seem to be the main reasons for this," said Yeung.

Indeed, the most popular underlying in the market in 2016 has been gold, which drew purchases of US$12.8bn this year, according to the SRP database. Competing for second are Libor and the CSI 300 Index, which have both lost some 10% in sales from last year, falling to US$10.5bn and US$10.4bn, respectively.

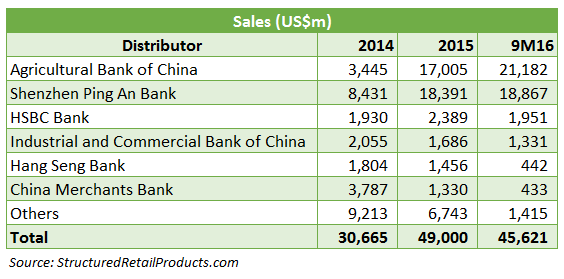

Agricultural Bank of China has been the most active distributor of commodity-linked products this year, with 167 offers, with CMB a distant second with 30 products. Over 79% of commodity-linked products issued in 2016 feature digital payoffs, while range and shark fin were present in 17% and 16%, respectively.

Market distribution by capital protection level has maintained a distinct barbell structure this year. Products with a guaranteed return rate of 100% or more constituted over 53% of sales on the mainland, while structures with zero protection contributed just under 46%. In comparison, the '100% or more guaranteed' spot accounted for over 63% of the market in 2015 and over 87% in 2014, whereas zero protection accounted for 35% last year and just over 10% in 2014.

A more restrictive framework for wealth management products was introduced in July, limiting the amount of leverage that can be used on structured debt notes as well as restrictions to prevent money borrowed by investors inflating the country's equity and bond markets.

Among a number of changes, including lower leverage caps and better disclosure requirements, the rules would allow only banks with more than RMB5bn (US$734m) of net capital to pump wealth management product funds in non-standard credit assets, while others will have to seek out less risky investments. The new rule is designed to encourage issuers to use alternative ways of enhancing product returns, according to one Shanghai-based senior banker. "This evolution should be positive for the structured investments landscape in China," said the banker.

UBS losing ground in Australia as equities widen appeal gap

China QFII investment limitations lift to help funding management

Education is vital for getting rid of the demons, China Merchants Bank