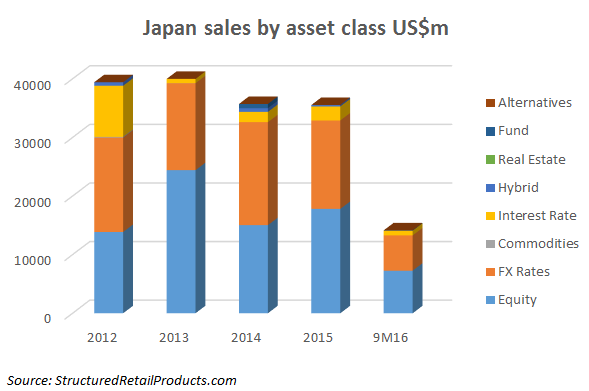

The structured products market in Japan is enduring a trying period in 2016, with sales in the first nine months of the year dropping by just under 50% compared with the same period last year, amid toughening economic conditions and with stimulus efforts focused on exchange-traded funds (ETFs).

Equity and foreign exchange remained the top asset classes by a large margin, with investors still eagerly buying into yen pairs as a hedge against the volatile swings in the Japanese currency induced by its safe-haven status. At the same time, interest in other asset classes continued to drop, with interest rate losing a significant portion of its weight this year.

The most popular underlyings for structured products remained either currency pairs or equity indices, including the Nikkei 225, Eurostoxx 50 and S&P 500. Only 14% of all structured products sold in Japan were based on single stocks or basket of stocks, and no corporate name is present in the 10 most popular underlyings for 2016 as of September 30. In comparison, less than 12% of all products sold in 2015 were pegged to stocks, as well as just over 13% in 2014.

Digitals and dual currency structures were featured in over 77% of structured products sales in the first nine months of this year, according to SRP data. This compares with just over 80% that the two structures featured in in 2015, and about 77% in 2014, indicating that yield and currency hedging remain top priorities for Japanese investors.

The market maintained a quite granular structure in terms of distribution, with Mitsubishi UFJ Morgan Stanley Securities reinforcing its position on top. Excluding MUFJ, which has accounted for 16% of total sales in 2016, the remaining top 10 contributed only 46% of sales, with a total of 66 distributors selling products during the year. The market remained dominated by the domestic distributors, and only ANZ, with a market share of about 8%, maintains a strong foothold on the market at the number three spot.

Scandinavian institutions remain the most popular asset custodians with nearly 40% of Japan's structured products bond providers during the first nine months of 2016 hailing from the region.

"Nordic agencies have had a presence in the Japanese retail market since the beginning of the millennium," Martin Svenholm, funding manager at Municipality Finance, told SRP in a recent interview, noting that Municipality Finance aims to raise up to a third of its funding via Japan retail. "For the borrowers, Japan has always been a stable source of funding at a relatively low cost."

However, arguably the biggest story on Japan's investment scene this year has been the roll-out of an expansive stimulus programme by the Bank of Japan. After a recent upgrade, the BoJ now aims to purchase up to ¥6tn (US$56bn) worth of ETF shares per year in ETFs that pick out companies exhibiting positive corporate governance practices.

Nikkei has recently announced plans to roll out a new mid- and small-cap index to track Japanese companies that observe investor-oriented corporate management, as measured by return on equity and operating profit, to complement its JPX-Nikkei 400 Index. While the new index may fit BoJ's ETF purchasing scope, Nikkei declined to speculate on the treatment of the gauge by the Bank.

"We hope the new index will be utilised by varieties of users including asset management companies," said a spokesperson.

BoJ's measures should help drive up demand for investment in Japan, according to Nizam Hamid (pictured), ETF strategist at WisdomTree in Europe.

"We'll start to see clients coming back to currency-hedged products, which is a very important tool to play in Japan," said Hamid. "We're already starting to see a lot of clients wanting to know what they should be watching for in Japan."

Nikkei and JPX to roll out new small- and mid-cap Japan index

We hope to raise up to a third of our funding from Japanese retail investors, Munifin