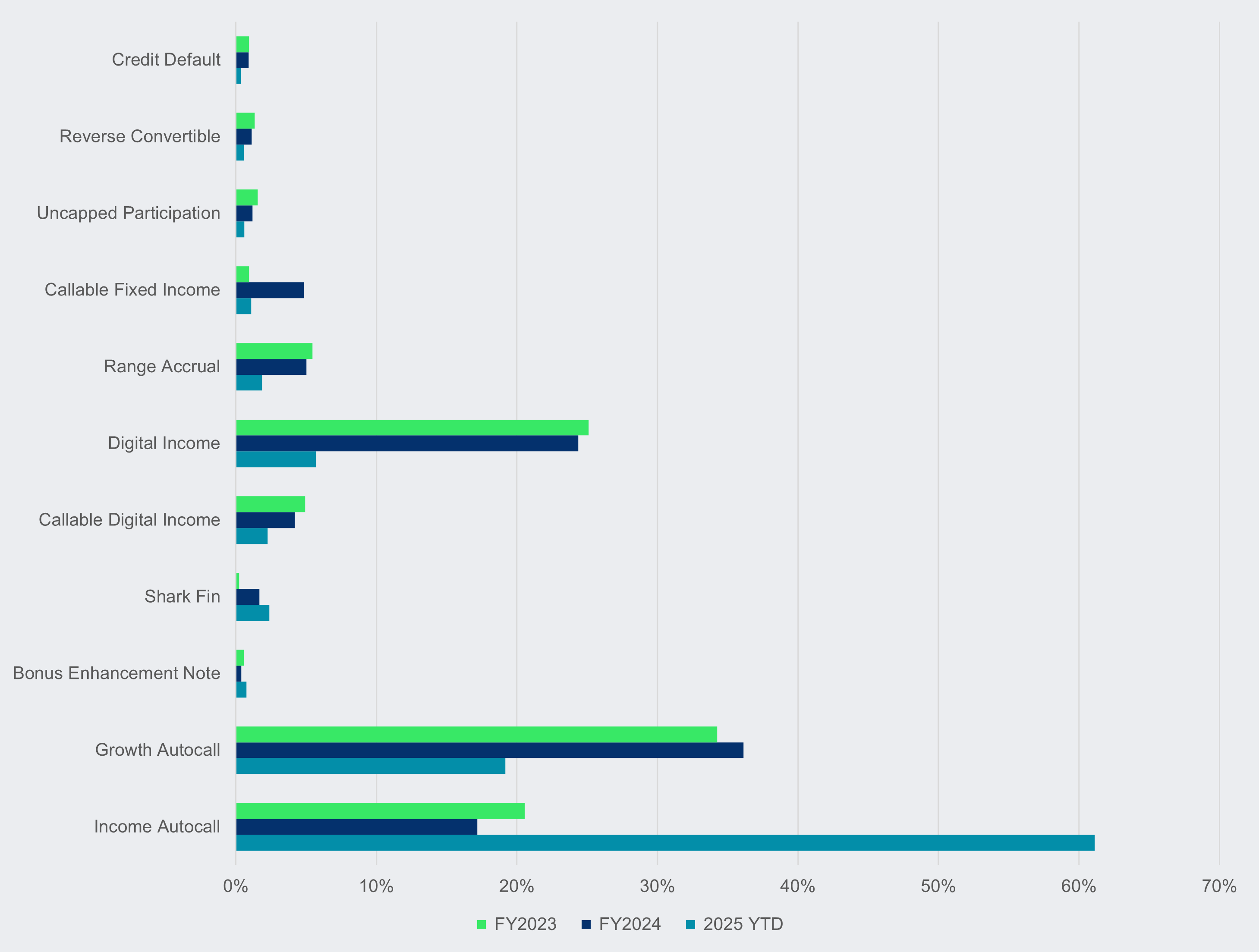

Autocallables dominate the regional market share, led by income autocall structures.

Autocallables are accounting for around 80% of the estimated sales volume of structured products sold in Asia Pacific (Apac) ex-China this year so far, according to SRP data.

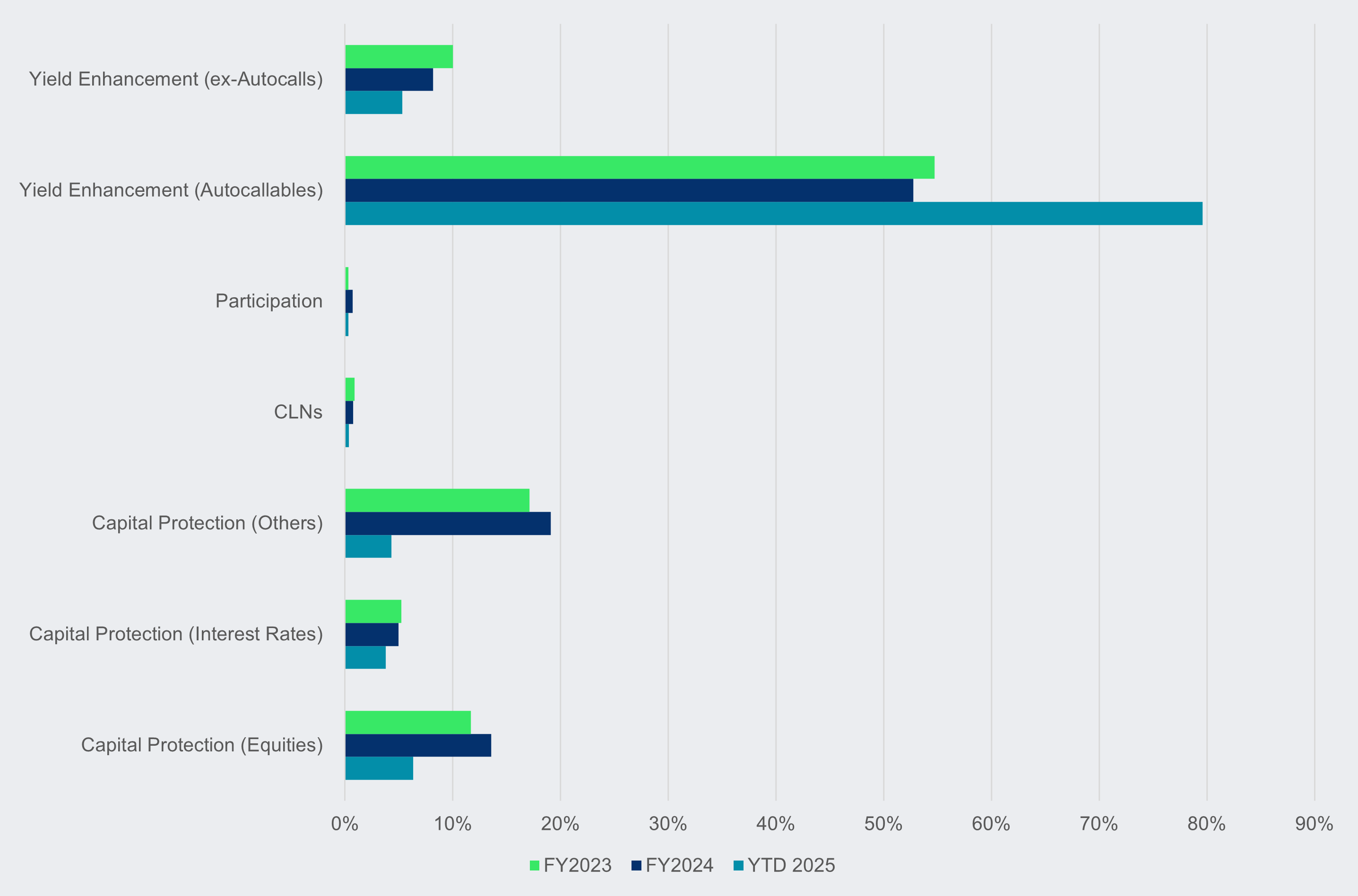

Estimated sales of these yield enhancement products’ saw a sharp increase the 53% market share recorded a year ago, mostly boosted by growth in Hong Kong SAR and Taiwan.

Income autocalls, including the popular fixed-coupon notes that pay a regular coupon, accounted for approximately 62% of the market share, while 19% of the market share stemmed from growth autocalls.

Asia Pacific ex-China: structured products' core payoff market share per estimated sales volume

Source: SRP

In Hong Kong SAR, such income autocall structures have been wrapped in equity-linked investments (ELIs). SRP database registered some 52,000 ELI issuances this year that featured the autocallable payoff – with more than half of which tracking single stock.

The total net notional outstanding of ELIs reached HK$68.2 billion (US$8.8 billion) by the end of November, soaring 66% from the start of this year, data from the Securities and Futures Commission shows.

Meanwhile in Taiwan, there have been over 63,000 structured notes featuring autocallable payoffs this year. Nearly 70% of which were structured as a snowball structure, or growth autocalles, with a daily memory feature.

In South Korea, capital-at-risk autocallable notes, commonly known as equity-linked securities (ELS), have recorded over 7,800 issuances year-to-date worth of US$11.8 billion in sales. All of these products mainly tracking a basket of benchmark indices were sold to retail investors.

The digital income payoff was next in line, with six percent of the market share in the Apac ex-China region year-to-date. These structures are often seen in FX rates-linked structured deposits in Hong Kong and in capital-protected equity-linked bonds (ELBs) sold in Korea, with the latter market seeing nearly US$13 billion sold this year so far, linked to a digital income payoff.

ELBs’ sales are still expected to increase in December, as Korean investors usually deploy money into retirement pensions via one-year-tenor ELBs at the end of each year.

Callable digital income products saw a lower market share of two percent this year, a drop from four percent a year ago. These products were structured as callable equity-linked notes in Taiwan, which recorded 5,203 products by the end of November. Most of these issuances tracked weighted stock baskets.

In Apac ex-China, the shark fin payoff type also gathered two percent of market share in 2025 so far, similar to a year ago, while accrual range’s market share fell to two percent from five percent seen in 2024.

Additionally, callable fixed income, reverse convertible, uncapped participation and bonus enhancement notes each made up around one percent of the market share, respectively, with the latter seeing increased volumes from a year ago.

Asia Pacific ex-China: market share product group per estimated sales volume

Source: SRP

By product groups, yield enhancement’s estimated sales accounted for around 86% of volumes in the region year-to-date, up from 61% in 2024.

Capital-protected structures accounted for 14% of the market share, down from 38% last year. Among, capital-protected equities structures dropped to six percent from 14% a year ago, while capital-protected other structures fell to four percent from 19%.

Some minor volumes were generated from credit-linked notes and participation products in the meantime.

Do you have a confidential story, tip or comment you’d like to share? Contact Us | SRP (structuredretailproducts.com)

Disclaimer: While SRP's aim is to provide accurate and up-to-date information, the data provided is gathered from third parties. SRP does not take responsibility for the accuracy of the data and will not be held liable for any errors or omissions contained in the information provided. The information and data included on SRP's market reports uses sources believed to be reliable. SRP assumes no liability or responsibility for the quality, content, accuracy or completeness of the information, text, graphics, links and any other items contained in this report.