Structured product players in Asia are weighing the impact of a potential AI bubble as elevated tech valuations extend into 2026.

Fears over a growing artificial intelligence (AI) bubble have kept markets buzzing, shipping such jitters from late last year into 2026.

Clients are increasingly focusing on balancing their technology exposure with lower-beta investments - Jaye Chiu, Bank of East Asia

Structured product market participants in Asia are showing a split, with some exploring tactical strategies to navigate rising valuations in Wall Street’s AI-exposed companies, while others emphasise diversification to manage short-term volatility.

One is the growing emphasis on diversification to mitigate risk amid short-term volatility, despite the high conviction in the technology sector, according to Jaye Chiu, regional head of private banking at Hong Kong-based Bank of East Asia.

“Clients are increasingly focusing on balancing their technology exposure with lower-beta investments, ensuring portfolio stability in times of market fluctuations,” Chiu told SRP as he spoke of the role structured products play in investors’ portfolios.

The private banker noted that the AI growth narrative holds with many leading AI companies maintaining “strong balance sheets” and “stable” credit risk indicators broadly, but the bank advises its clients to actively monitor their positions and limit their overall exposure to AI sectors to avoid potential over-concentration.

[Investors] are broadening out and diversifying across industries and geographies - Tony Lee, J.P. Morgan

When considering underlying exposures via structured products, investors are looking to broaden their AI-beneficiary stock picks beyond Wall Street’s names, said Tony Lee, head of global equity derivatives strategy at J.P. Morgan.

“Not only on the ‘Magnificent Seven’ and or your typical hyper scalers, but [investors] are broadening out and diversifying across industries and geographies,” Lee said. “That's why you see Korean AI stocks continue to rally, and so did Taiwan Semiconductor Manufacturing Company. Of course, people are now looking into the Hong Kong/China space.”

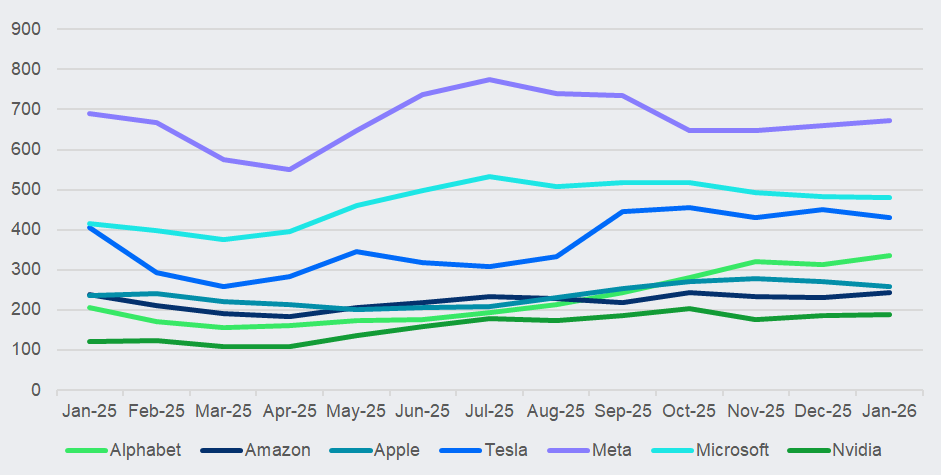

US ‘Magnificent Seven’ stocks’ price move since the start of 2025 (US dollar)*

*Data as of 27 January’s market close

Source: Yahoo Finance

To hedge a potential AI headwind in 2026, the US bank recommends hedging structures that “can still be monetised if a selloff happens after another upside run,” reads a recent research report.

This includes resettable and lookback put spreads that trade “at a historically narrow premium” and best-of put spreads on these AI-exposed indices like the Nasdaq 100, Nikkei 225, and Taiwan Stock Exchange Index that provide a “more balanced combination of cost savings and protection”.

On the other hand, some see little change: an equity derivatives Asia sales head told SRP this month that fears of an AI bubble collapse remain “just talks” and have yet to trigger any meaningful market shift for underlying exposure in trading structured products in Asia, as investors who look for returns “are afraid of ‘fear of missing out’ (FOMO)” from the US equities’ rally.

We don't know where the bubble burst or how many can survive, but what we surely know is, for example, Nvidia, Microsoft and Google will survive - Jingwei Chen, Wrise

For Wrise Group, a Singaporean independent wealth manager that deployed 25% to 30% of assets in structured products in its high-net-worth-individuals’ portfolios last year, the strategy is straightforward: sticking with the big names.

“We do believe that there is a certain bubble in this AI, but we believe that even if the bubble bursts, somewhere will just survive and continue to win the market,” said Jingwei Chen, regional chief investment officer.

“We stay boring – we don't know where the bubble burst or how many can survive, but what we surely know is, for example, Nvidia, Microsoft and Google will survive,” Chen said, pointing out these big firms’ “strong cash flow” and “best capital expenditure spending” like Google’s Gemini model are among its key underlying-picking factors.

The wealth manager, which captured a 40% to 50% climb in structured products traded notional in 2025, uses fixed-coupon notes (FCNs) trades on “moderately bullish underlyings” and bonus-enhancement notes (BENs) on “super bullish underlyings” to get the full upside, according to the Wrise executive.

The rise of Chinese/Hong Kong equities

Meanwhile, China’s AI startup DeepSeek has sparked a comeback in Chinese equities, prompting some investors to embrace Hong Kong-listed AI-exposed products from Bank of Singapore and BNP Paribas Wealth Management. The latter had capitalised on the trend to combine US and Hong Kong equities into an AI-related basket exposure and had deployed into BENs, FCNs, and accumulators in Asia.

Retail investors couldn’t miss out on this China AI theme when trading listed structured products, either.

Going into 2026, investor sentiment in Hong Kong continues to be driven by China’s recent AI advancements - Keith Chan, Société Générale

The Hong Kong Exchanges and Clearing (HKEX), Asia’s largest listed structured product bourse, showed that total turnover in ATMX-linked derivative warrants – consisting of Alibaba, Tencent, Meituan, and Xiaomi – skyrocketed 72% year-on-year to HK$648 billion (US$83 billion) in 2025, according to statistics from Société Générale.

“Going into 2026, investor sentiment in Hong Kong continues to be driven by China’s recent AI advancements and growing anticipation around upcoming AI-related initial public offerings,” said Keith Chan, head of cross-asset listed distribution for Asia Pacific at the French issuer.

“Year-to-date fund flows indicate a clear risk-on appetite, with most activities concentrated in call warrants on major technology names – led by ATMX – as well as companies expected to benefit from the accelerating adoption of AI,” Chan added.

Allocation beyond the US

Asian investors are also eyeing exposures beyond traditional markets, industry observers said.

Bank of East Asia saw its structured products’ underlying exposure was “fairly balanced” between the US and Hong Kong markets in 2025, with investors’ increased exposure to the Japanese and Chinese markets, Chiu noted.

“This trend highlights investors’ willingness to explore opportunities beyond traditional markets to capture emerging growth potential,” he said. He added that the shift towards tailored, non-flow products and the demand for principal-protected structures are also emerging in the market.

Wrise’s Chen said in 2025 that half of the firm’s equity-linked product volume came from US exposures, 40% from Hong Kong, and 10% from Singapore, with the latter’s volume doubling as dividend-paying names lured local investors.

In 2025, US names accounted for around 60% of the 70% of Asia-issued structured products’ underlying exposures, slightly shy of the 80-90% seen in 2023 and 2024, J.P. Morgan’s Lee estimated.

Lee added that US stocks remain “pretty attractive,” while Hong Kong/China stocks “will take time to pick up” for this year’s structured products’ underlying exposure outlook.

“The US [market exposure] is too big to ignore,” he said. “Talk of the end of US exceptionalism has cooled – the focus has shifted to building more diversified portfolios across regions and sectors.”

Image: Sikov/Adobe Stock

Do you have a confidential story, tip or comment you’d like to share? Write to jocelyn.yang@derivia.com