The purpose of this article is to break down the essential elements of structured products - including how they are built, how investors use them and most importantly the risks that come with them - in a way that's easy to understand.

We’ll start with a simple definition…

What is a structured product?

Structured products are a type of financial investment that you can buy - and later sell (if it makes sense) - just like a stock or a bond. They show up in your investment account as a single security with its own ID number (called an ISIN).

As the name suggests, there is some clever "structuring" behind them: think of them as a "combo meal" in finance - they bundle two or more financial instruments together into one single product. A bank or a specialized firm builds this combo, packages it and sells it to investors.

What is inside the combo? Often, it is a mix of two ingredients:

| A bond component: typically, the base that helps protect or grow your money steadily but be careful it is itself a risk as the bond may not pay back the money - the so-called credit risk (more later on), and |

| A derivative instrument: the “exciting” part - a contract whose value depends on something else, like a stock price or an equity index - which gives the product its special payoff(s) |

What are derivatives?

A stock, listed on a U.S. stock exchange such as the New York Stock Exchange (NYSE), will be traded when a buyer’s bid meets a seller’s ask based on their respective transaction orders and the transaction will take place at the corresponding price. Now, a derivative related to that stock - with that stock as the as the underlying asset, has its price (economically) derived from the stock’s price.

Therefore, the derivative is not the stock itself, but an instrument based on that stock. A derivative can have different purposes such as (easily) providing leverage to increase or increasing substantially the exposure of a portfolio, but they all involve a transformation of the risks of the investment portfolio.

“Plain vanilla” derivatives

Among the simplest derivatives, used in the context of structured products, there are the forward and the futures as well as so-called European options. They all are also called plain vanilla - vanilla being one of the most basic and appreciated tastes, it simply makes sense.

A forward or a future contract, if it listed on a dedicated exchange (it is called a future and it works also a bit differently from a forward), consists in committing to buy or sell at future point in time while the price of the (future) exchange of money versus underlying is set… today.

Its simplified pricing formula is Forward = Costs (with financing costs in particular) -Benefits (for equity, the dividends) or: F = S + C -B, up to that future point in time called the forward’s expiration. Benefits – Costs are called the basis - they are a function of the time to expiration - and as the forward gets closer to the expiration, the basis will “converge” towards zero.

Actually, the pricing formula is based on what is commonly called arbitrage: it must be the same, going long a forward or buying today the underlying using credit. What is key is that both, the risks and the cash-flows are identical: then selling a forward today and buying it indirectly with the underlying (using a credit) will lead at expiration to a net zero-cash-flow – as you buy and sell the same thing in the future!

The forward can be used by a gold mine company to sell its future gold production at set price (today): it therefore can budget a selling price despite the gold not being yet extracted! That is called a short (because they sell the forwards) hedging transaction, one of the key use cases of derivatives.

Selling a derivative means entering a short position in that derivative: if someone buys the forward (thinking its price will go up), your profits and losses are the opposite of theirs. It is like someone makes money when you lose, and vice versa. Does this mean it is a game where nobody wins or loses (a zero-sum game)? Not really! Like other businesses, margins (a little extra money you need to start) and commissions (fees paid to people helping with the trade) are always added. Derivatives are a very easy way to “bet” that something will go down: that is the so-called short exposure. This is a really important feature of derivatives, especially in Europe where shorting stocks is more complicated.

Buying and selling

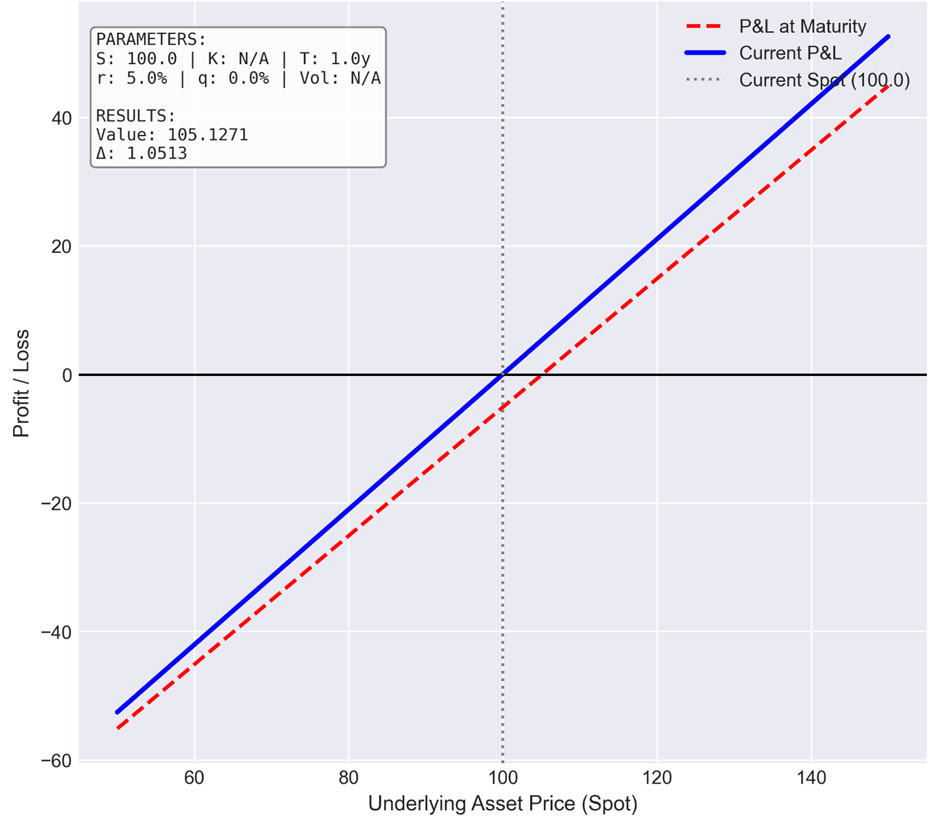

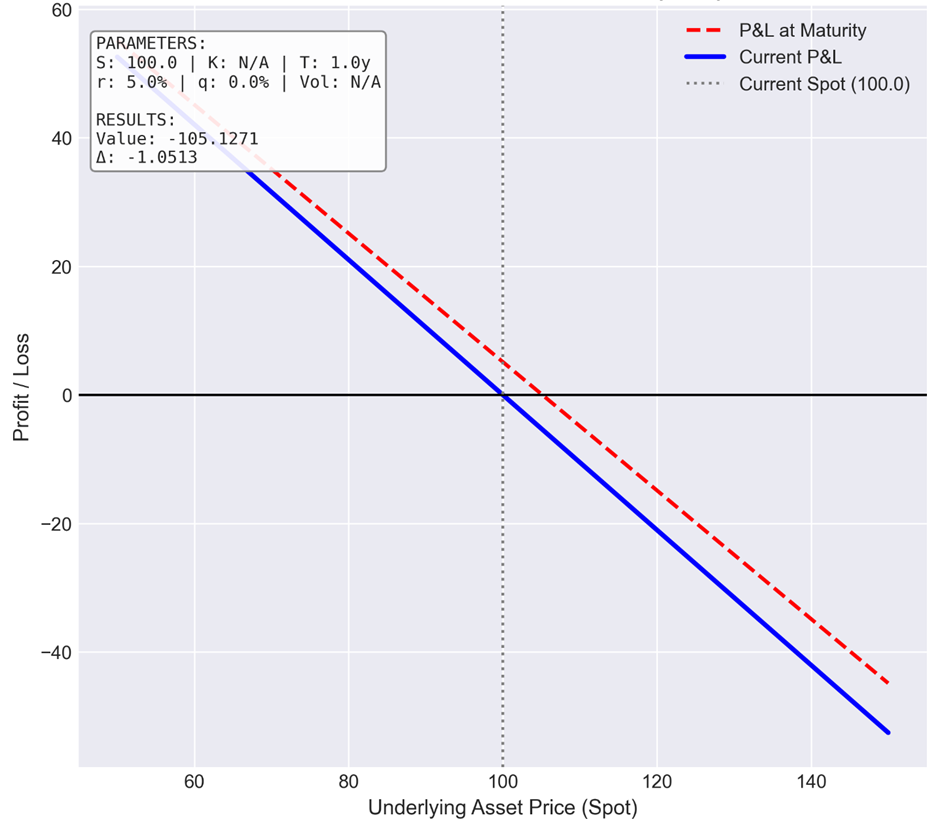

Let's look at what happens when you buy (long) or sell (short) a forward contract. Imagine a graph where the price of the underlying asset goes from left to right.

If you buy (go ‘long’) a forward contract: you profit when the price of the underlying asset goes up. Your profit goes up as the price of the underlying increases further. We use the term profit & loss (P&L), just like in any other industry.

If you sell (go ‘short’) a forward contract: it's the opposite. You profit when the price of the underlying asset goes down. Your profit goes up as the price of the underlying decreases further.

Long forward - profit & loss (P&L)

Source: Evolids Finance

Short forward - profit & loss (P&L)

Source: Evolids Finance

In these two graphs, one can also see the first Greek we want to address: the Delta. Delta measures the change in the derivative’s value resulting from a change in the underlying price. So, if an equity index is the underlying and it rises by 1, while the Delta is +1.0513, the long forward will increase by +1.0513 × 1 = +1.0513 and the short forward will decrease by -1.0513 × 1 as the Delta is -1.0513. For a long forward, delta is typically close to +1, and for a short forward, it is typically close to -1. We can approximate this by saying that the forward’s value moves one-for-one in absolute terms with the underlying.

Options types

Let's discuss European-style options, which come in two types: calls and puts. When you buy a call option, you obtain the right (but not the obligation) to buy the underlying asset at the specified strike price - one of the option’s parameters - giving you a bullish position (with a positive Delta). A put option, on the other hand, gives you the right to sell the underlying asset at the strike price, representing a bearish position (hence a negative Delta).

Importantly, these rights are exercisable – you then buy (call) or sell (put) the underlying - only at the option's expiration date: this is what differentiates European-style options from American-style options, which can be exercised at any point up to and including expiration. The expiration is another one of its parameters. If you buy an option, you pay a premium for the right to buy (call) or sell (put) at the strike price, independently of how much the underlying moves: the more the underlying moves in the right direction the more money you make – the option is the said to be In-The-Money (ITM).

Moreover, the forward price of the underlying asset at expiration is important for determining the option's value; hence, the forward is an integral part of the pricing equation.

And, contrary to what some may think, these derivative exposures can be reversed before expiry: if you bought at the ask-price at the beginning, you can sell at the bid-price before expiration.

In summary, there are four basic option positions: long call, short call, long put and short put.

Each corresponds to a distinct market view: with a long call, the investor who paid a premium to go long expects the underlying to go up (quite) sharply. With a short call, the user expects the underlying not to move (or to change only slightly) at expiration or to stay a bit below the strike; the ideal outcome is to retain the premium as profit. With a short put, the user expects the underlying again not to move (or to change only slightly) at expiration; preference is then a small gain in the underlying. Finally, with a long put, the user who paid a premium to go long, expects the underlying to go down significantly.

Leverage with derivatives: the case of the forward / future

Derivatives like forwards and futures let you get leveraged exposure - meaning you control a large amount of an asset (like stocks or commodities) with just a small upfront investment which is the initial capital required. Leverage is simply the ratio: total position value divided by your initial capital (called margin). For example, with 1’000 dollars margin, you might control 10’000 dollars’ worth: that's 10x leverage.

This works for forwards (custom, private / Over-The-Counter contracts) and futures (standardized, Exchange-Traded Derivatives). But leverage cuts both ways: it amplifies gains and losses.

A big risk is counterparty risk - the chance your trading partner can't pay up. Forwards have higher risk since there is an Over-The-Counter agreement directly between two parties. Futures are safer: they're Exchange-Traded Derivatives (ETDs) handled by a clearing house that steps in as the middleman for everyone. It requires margin accounts tailored to each product's risk to cover potential shortfalls. This leads to the famous “margin call”, where the investor must post additional funds to cover losses.

Key categories of structured products

Structured products come in about five key categories based on the derivatives they use, each designed to match a specific, fine-tunable market view (prediction). This setup matches your market prediction perfectly. We will explore this further - and the benefits of shifting from traditional asset allocation to strategy allocation - in an upcoming article.

| Category | Description | Exposure Type / Beta Relationship | Typical Investor View |

| 1. Leverage Products | Provide amplified participation in the price movements of the underlying asset through derivatives, typically using futures or options. | Multiple of beta (≥ 1 or ≤ –1); very high sensitivity to underlying movements. | Strong directional view - investor expects a pronounced move in a specific direction. |

| 2. Market Participation | Replicate or slightly outperform the underlying asset’s return by using derivatives to gain efficient exposure. | Close to 1× beta or slightly higher (beta +). | Positive or strongly positive with time market view |

| 3. Yield Enhancement | Enhance yield by selling volatility or downside participation (e.g., reverse convertibles, discount certificates). Capital protection is partial or absent. | Reduced or asymmetric beta; investor gives up upside for additional yield. | Neutral to mildly bullish view - investor expects stable or moderately rising markets. Especially at maturity. |

| 4. Capital Protection | Ensure partial or full capital repayment at maturity using zero-coupon bonds and options; participation in upside is limited. | Limited participation (beta < 1) due to embedded protection. | Cautiously positive view - investor wants upside exposure with protection against loss. |

| 5. Credit-Linked / Credit Risk Products | Link return to credit events or spreads of specific issuers or reference entities (e.g., CLNs, credit-linked notes). Investor takes on credit/default risk. | Exposure to credit spread or default probability; no capital protection. | Credit view - investor expects no credit event and aims to capture higher yield from taking additional credit risk. |

Beta measures how an investment’s returns react to movements in the wider market (usually a benchmark index but it can also be a basket of stocks, for example).

A beta of 1 indicates the product moves in line with the market - it carries comparable risk and expected return.

A beta >1 means it amplifies market moves (up or down), so higher wins but also higher risk.

A beta <1 shows less reaction to market swings; the product tends to be less volatile and therefore less risky than the market.

Next up: Part 2 of “Structured Products and the Greeks in easy language” will be released later this year and will dig deeper into structured products while maintaining the same easy-to-read approach.

Image: Adobe Stock

| This article is based on data and analysis provided by the SRP Greeks product. Find out more about SRP Greeks here |

Disclaimer

This content is not intended as a solicitation or an offer; it is provided solely for informational purposes to professional investors. The information presented herein has been prepared with great care; however, errors may still occur.