Equity-linked products remained the dominant asset class, accounting for 60% of sales in the quarter.

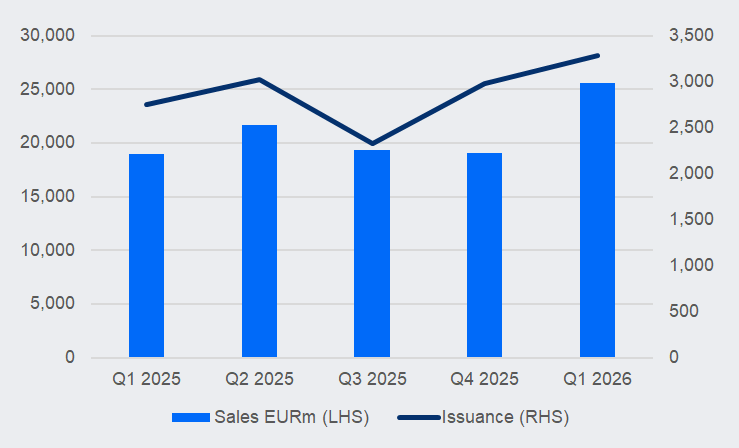

The first quarter of 2026 marked a strong start to the year for the French structured products market with sales reaching €25.5 billion (US$29.8 billion) – up 35% year-on-year (YoY) from €18.9 billion in Q1 2025.

At the same time, the number of products increased from 2,746 to 3,279, confirming both investor demand and sustained issuance across distributors and issuers.

France: issuance and sales by quarter (EURm)

Source: SRP

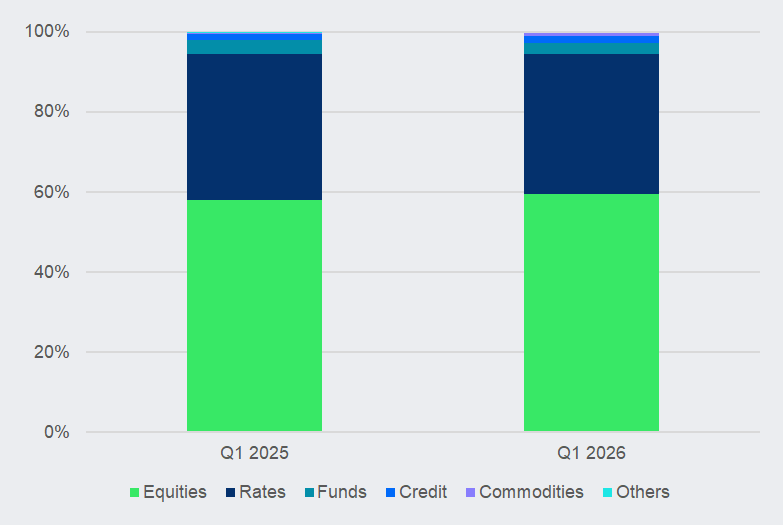

Asset classes

Equity-linked products remained the dominant asset class, accounting for 60% of sales in Q1 2026, compared with 58% a year earlier. This reinforces their central role within the French market, despite a more volatile macro environment and bigger selectivity in exposures.

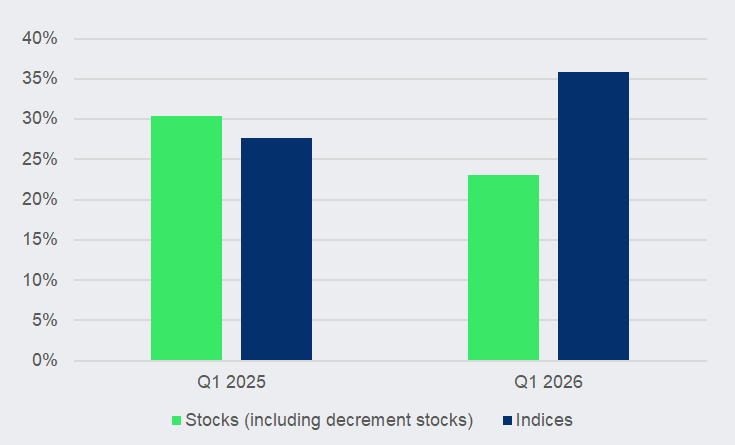

Within equities, a notable shift occurred between stock- and index-linked structures. Products linked to indices increased their market share from 28% to 36%, while stocks (including decrement stocks) declined from 30% to 23%.

Index-linked sales recorded particularly strong growth, rising by 70% YoY. This suggests a partial rotation away from concentrated single-stock risk towards structures offering greater diversification.

France: asset class – market share by sales volumes

Source: SRP

Rates-linked products remained the second-largest segment of the market, representing 35% of issuance in Q1 2026, slightly below the 37% recorded in Q1 2025. Rates products continued to benefit from structurally higher interest-rate levels.

Funds-linked products remained stable at three percent of issuance, while credit-linked notes (CLNs) also maintained a two percent share YoY.

Commodities-linked structures made an appearance in the market in Q1 2026. Although commodities represented only around one percent of total sales, the underlying composition reveals several thematic trends.

Gold was by far the dominant commodity exposure, both through direct commodity-linked structures and through gold mining-linked strategies. Standalone gold-linked products represented the largest allocation, ahead of WTI crude oil and silver-linked structures.

At the same time, commodity exposure also emerged indirectly through equity-linked decrement indices focused on mining and resource themes. Examples included several gold-miners decrement indices as well as the MSCI ACWI IMI Copper and Power Select 20 Fixed Basket 50 Points Decrement Index. These structures suggest that issuers increasingly used thematic equity baskets to provide commodity-related exposure.

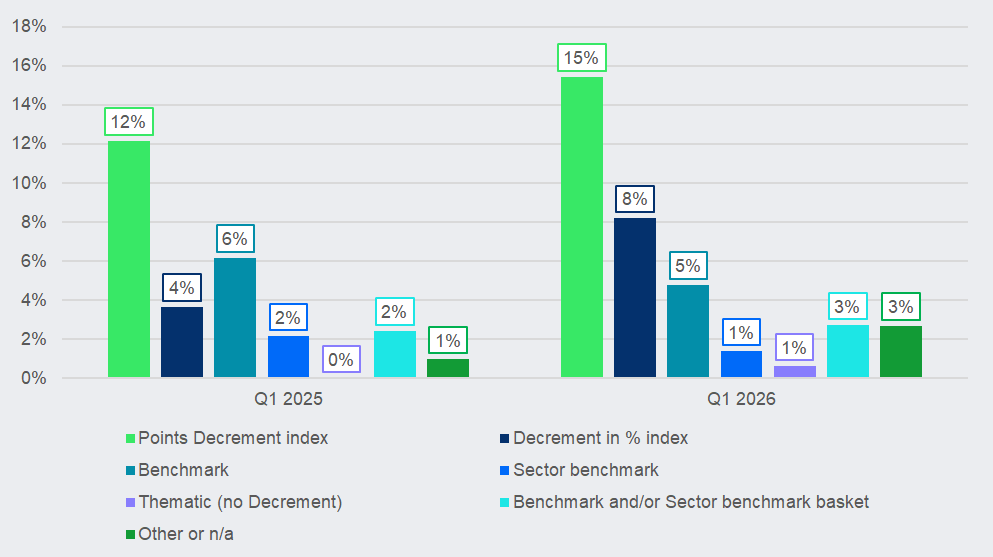

Equities

The shift within the equity segment was particularly visible in the continued expansion of decrement index strategies. Points decrement indices increased their market share from 12% to 15% in Q1 2026, while percentage decrement indices doubled from four to eight percent.

France: equities – market share by sales volume of total offer

Source: SRP

Both categories recorded very strong YoY sales growth, at 66% and 193%, respectively. Combined, decrement indices represented 23% of the French market in Q1 2026, compared with 16% a year earlier. By embedding a synthetic dividend deduction, decrement indices generally allow structurers to optimise coupons, barriers and autocall conditions compared with benchmark indices.

The latter saw only marginal growth in volumes and a slight decline in market share, from six to five percent, while sector benchmarks declined from two to one percent, with sales contracting by 16% YoY.

France: index types – market share by sales volume of total offer

Source: SRP

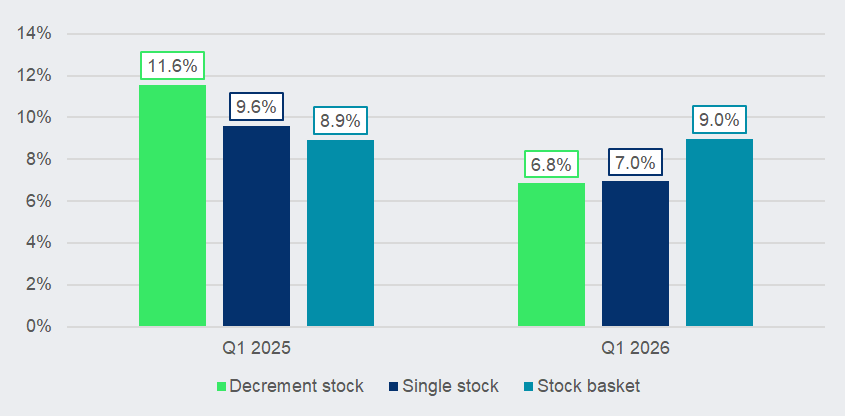

Within stock-linked products, decrement stocks experienced a significant contraction, with market share falling from 11.6% to 6.8%, i.e. a decline of 4.7% and sales decrease of 22.6% YoY. Pure stock-linked products also declined, moving from 9.6% to 7.0% of sales.

These developments indicate a more cautious approach towards concentrated equity exposures, notably following the drawdown observed on Stellantis-linked structures.

Multi-stock baskets remained broadly stable with market share at nine percent.

France: stock types – market share by sales volume of total offer

Source: SRP

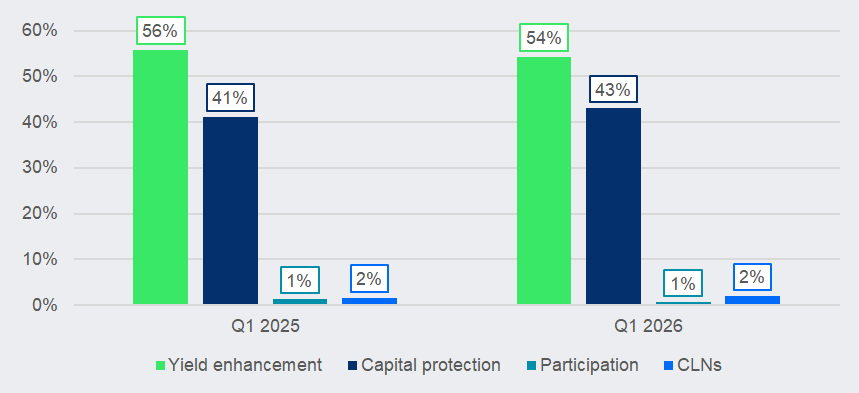

From a payoff perspective, yield enhancement products continued to dominate the market in Q12026, accounting for 54% of issuance, although slightly below the 56% observed a year earlier. Despite this slight decline in market share, sales increased by 27% YoY.

Capital protection products, returning a minimum of 90% of the invested capital, saw their market share increasing from 41% to 43% and sales rising by 37% YoY. This confirms the sustained investor appetite for protected products in an environment characterised by macroeconomic uncertainty and structurally elevated rates.

Product groups and payoffs

Products with directional participation remained marginal, while CLNs remained stable at roughly two percent, recording sales growth of 62% YoY.

France: product groups – market share by sales volume of total offer

Source: SRP

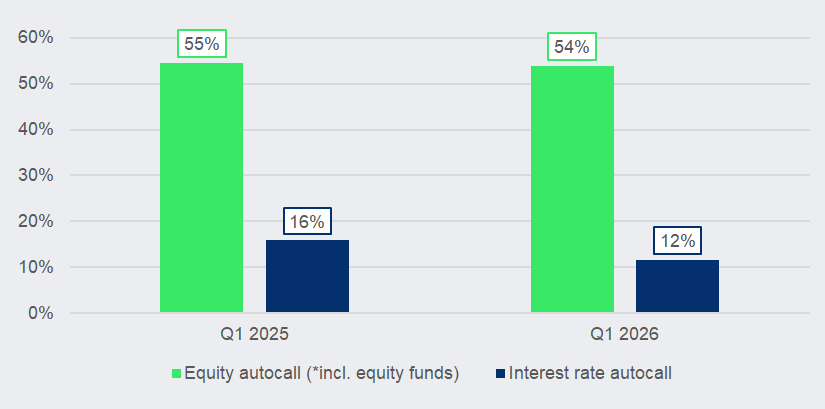

Autocallable products continued to dominate in Q1 2026. Equity autocallables (including equity fund-linked) remained broadly stable at 54% of issuance, compared with 55% in Q1 2025, while sales increased by 29% YoY.

France: autocallables – market share by sales volume of total offer

Source: SRP

Autocallables based around expectations of lower long-term interest rates experienced a decline, with market share falling from 16% to 12% and sales decreasing by four percent YoY. The change in expectations for long-term interest rates, made many of the previously issued products miss their redemption conditions.

The main underlyings used across these structures included short-term money-market benchmarks such as three-month Euribor and 12-month Euribor, sovereign yield benchmarks such as Banque de France TEC 10 and Solactive BUND 10Y 11am, as well as swap-rate exposures including two-year EUR Constant Maturity Swap (CMS) and 10-year EUR CMS rates.

France: payoff – market share by sales volumes

Source: SRP

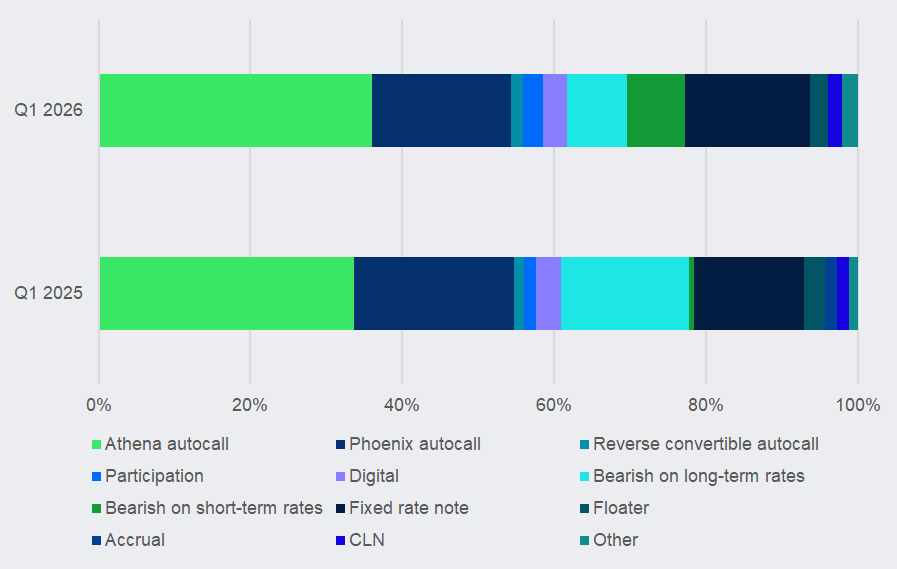

Athena autocalls remained dominant, increasing their share from 34% to 36% between Q1 2025 and Q1 2026.

Conditional coupon reverse convertibles (Phoenix autocalls), while still representing a significant share of the market, declined from 21% to 18% over the same period.

Reverse convertible autocalls remained marginal but increased slightly from roughly one percent to two percent.

The autocallable segment continued to evolve towards more frequent observation frequencies. Quarterly observation structures remained dominant, increasing from 47% to 50% of the equity autocall universe. Monthly observation autocalls expanded even more significantly, with market share rising from 14% to 17%.

At the same time, daily observation autocalls continued to gain traction, albeit from a lower base. Their market share increased from five- to six percent, while sales rose by 78% YoY, making them one of the fastest-growing structure types within the French market.

The optimisation of autocalls was a major trend in Q1 2026. Step-down or negative autocall barriers increased their market share from 45% to 53%. This confirms the interest in structures designed to improve autocall probability over time amidst uncertainty around the medium-term direction of equities.

Within the rates-linked universe, one of the most notable developments was the sharp decline in structures with bearish view on long-term rates, whose share fell from 17% to 8%. By contrast, products based on short-end policy-rate changes increased significantly from one- to eight percent.

Fixed-rate notes remained broadly stable and continued to represent a major component of the rates-linked segment, increasing slightly from 15% to 16%. This segment has been mainly supported by sizeable quarterly campaigns from French retail branch networks.

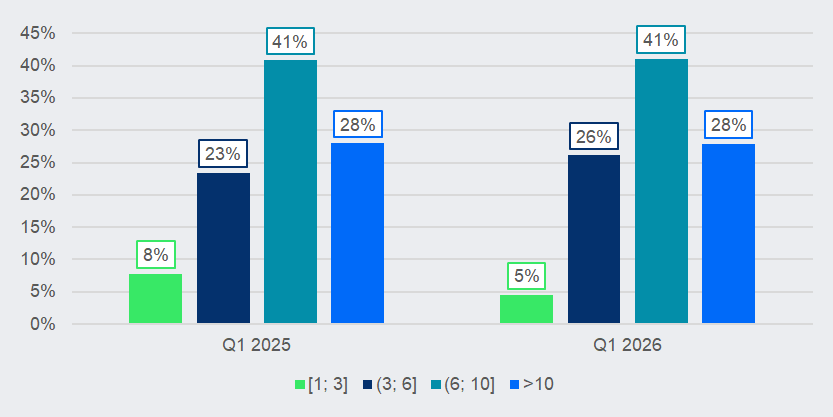

Investment terms

Products with maturities between six and 10 years remained the dominant segment, accounting for 41% of issuance, broadly unchanged from Q1 2025.

France: product terms – market share by sales volume of total offer

Source: SRP

Products with maturities between three- and six-years recorded the strongest relative expansion. Their market share increased from 23% to 26%.

Very long-term structures with maturities above 10-years also remained highly significant within the French market, representing 28% of issuance in both periods.

By contrast, shorter-dated products with maturities between one- and three-years continued to decline. Their market share fell from eight- to five percent, while sales contracted by 24% YoY. This confirms that the French market remained structurally oriented towards medium- and long-term investment solutions, with growing use of more frequent autocall observation mechanisms.

Image: Adobe Stock

Do you have a confidential story, tip or comment you’d like to share? Contact Us | SRP (structuredretailproducts.com)

Disclaimer: While SRP's aim is to provide accurate and up-to-date information, the data provided is gathered from third parties. SRP does not take responsibility for the accuracy of the data and will not be held liable for any errors or omissions contained in the information provided. The information and data included on SRP's market reports uses sources believed to be reliable. SRP assumes no liability or responsibility for the quality, content, accuracy or completeness of the information, text, graphics, links and any other items contained on this report.