Rabobank has reported a €752m net loss on structured notes in the first half of 2016, driven by a steep drop in interest rates spurred by the UK decision to leave Europe and a tightening of the bank's own credit spread. The loss 'stood in contrast to the first half of 2015 when, driven by the Greek turmoil, a widening of the credit spreads resulted in a net gain', stated Rabo when presenting its interim results on August 18.

The bank's primary objective for its structured notes, which are mainly linked to interest rates, inflation and equity, or have a callable feature, is to raise long-term funding under favourable conditions compared to the larger public bond issues, according to the bank. 'This is possible as structured notes are sold to investors and structured at their request (reverse enquiry),' stated the bank.

The issuance of structured notes diversifies Rabo's funding and allows issuance with non-standard terms and, 'because of the embedded derivatives, fair value accounting is applied to these notes'. Under international financial reporting standards, the fair value must include the impact of changes in the bank's credit risk, according to the bank. 'Although all structured elements are fully hedged, movements in Rabobank's own credit spread can still lead to a profit or loss,' said the bank. 'Furthermore, issuance below secondary market levels can lead to first-day profits, reflecting the comparative funding advantage.'

The net profit of Rabobank Group in the first half of 2016 was €924m, a decrease of €598m on the same period last year. The fall in net profit was due, in part, to higher administrative expenses from additional provisions for adopting the small and medium-sized enterprises interest rate derivatives recovery framework as well as higher restructuring costs, according to the bank. Other income, at €446m, a decrease of 70% from the first half of 2015 (€1,483m) was lower mainly as a result of volatile fair value items - the results on hedge accounting and structured notes - according to the bank.

Underlying operating profit before tax was €2,123m, a decrease of €54m on the same period last year. In calculating this underlying profit, a correction was made in provisions for interest rate derivatives, restructuring costs, hedge accounting and structured notes, and a further goodwill impairment for RNA (its retail bank in California), stated Rabo.

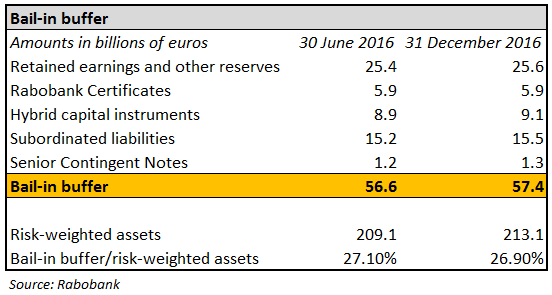

Rabo's bail-in buffer, which it defines as retained earnings, other reserves, Rabobank Certificates, hybrid and subordinated instruments and other debt instruments, the so-called senior contingent notes, decreased from €57.4m to €56.6bn, due to negative foreign exchange effects. In July 2016, the US$1.5bn issue of tier 2 instruments contributed positively to the bail-in buffer, according to the bank.

Rabo said it wishes to mitigate the risk of bail-in of creditors and depositors as far as possible by holding a large buffer of equity and subordinated loans that will be called upon first. Only thereafter will non-subordinated creditors, whose claims are not covered by collateral, have to contribute to losses if the bank gets into difficulties.

In March 2013, Rabo announced the closure of its equity derivatives division, following a review which found that it made only a limited contribution to becoming the number one wholesale bank in The Netherlands, as well as the leading player in the food and agriculture industry. However, Rabobank continues to offer interest-linked structured products to its clients.

'Rabobank's transition clearly took off in the first half of 2016,' said Wiebe Draijer (pictured), executive board chairman in a statement. 'We are making significant progress towards achieving our strategic goals: excellent customer service, a flexible and stronger balance sheet and improved financial results,' said Draijer. 'While there's still much to do, we are well on track regarding the fundamental strengthening of our cooperative bank.'

The Dutch bank has issued 502 structured products in its domestic market the Netherlands. Of these, 40 products, with combined sales of €3bn, are still live. The majority of live products are linked to interest rates (19), followed by equities (eight) and alternatives (seven).

Click the link to view the Rabobank interim report 2016.

Rabobank calls Lehman steepener note

Rabobank to pay over €700m in Libor affair fines

Rabobank: We are not quitting structured products