In the second of three articles analysing the equity-linked structured products market, SRP looks at how equities continue to claim the dominant share of the market, and how products linked to this asset class have fared over the last three years.

Although affected by decreasing new sales, equities have remained the top asset class with investors still eagerly buying. With 1,257,133 structured products linked to the asset class in 2016, equities have added 8% to a market share that stood at 49% in 2015.

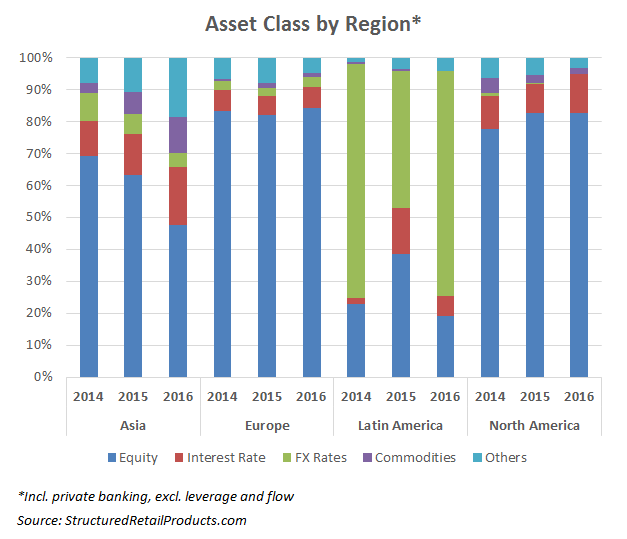

The attitude of the investors in Europe and North America was almost unchanged, while in Asia and Latin America the use of equities fell 6% and 18%, respectively, to the benefit of interest rates and FX rate-linked products, according to SRP data.

US equity-linked notional issuance has contracted, down by 10-15% year to date, according to Jorge Chancay, vice president, EFS solutions, at Barclays. "Equity-linked issuance has simply contracted in line with the entire market and continues to represent 80% of the total notional in the US," said Chancay. "We experienced some uncertainty in the summer with Brexit, which affected flows from some of largest players in the US. Flows were also affected in the fall as a result of the US elections. This uncertainty could continue into next year, depending on the degree of clarity we get around policy in the US."

"I have not seen particular trend towards Asian underlyings in Europe and I believe there is room to do much better than that." said Julien Lascar, head of cross-asset solutions and distribution sales for Europe ex France, Societe Generale. "For this, we need to go through a lot of education as, at this stage, people have limited understanding of Asian assets. For what we see, most of the big loads don't go to Asia yet. I feel it is still a tough discussion to our European retail and high net worth clients."

The market uncertainty ensured that investors paid attention to well-known, domestic indices, which saw an increase in sales at the expense of diversification and investments in other region underlyings. This trend is most prominent in the Americas, where the use of foreign underlyings decreased with an average of 15% of the total sales while local indices gained more ground. Eurostoxx 50, which was the top underlying in the first six months of 2015 with 28% of the market, was replaced by the S&P 500.

The latter has gradually increased its penetration reaching 30% as of November 2016, compared with the 8% of a largely disinvested Eurostoxx 50 losing even the second place to the benefit of interest rate-linked products.

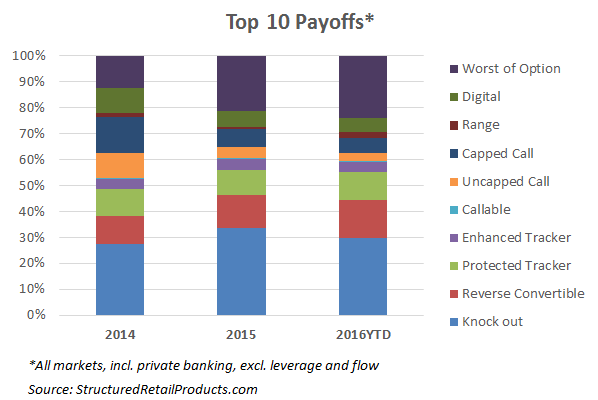

Historically, autocallable structures are the dominant payoff among the equity-linked products due to the fact that they are well understood by investors and allow providers to issue products with longer maturities while leaving the possibility to redeem early. According to SRP data, 30% of the total sales in 2016 were linked to these structures compared to 33% in 2015 and 28% in 2014.

"In the current interest rates environment (low, even negative rates), it is very difficult to design capital-protected products offering attractive value for money," said Arnaud Heckenroth (pictured), director, head of equities and hybrids exotics structuring Emea, Barclays. "You need to put capital at risk to make the product work. Autocallables and reverse convertibles are traditionally bestselling products in the private banking channel. We have recently seen those products and other partially capital-protected products very successful in other channels."

The low interest rate environment makes it harder to structure capital-at-risk payoffs because less coupon or upside can be bought but also encourages demand for worst-of option structures that gradually increased from 12% in 2014 throughout 21% in 2015 to 23% of the total sales in 2016.

Related story:

Equities 1: Equity-linked products in decline amid market uncertainty and lack of conviction