UBS is pushing its range of 'buy on dips' structured notes as an alternative structure to barrier reverse convertibles which dominate the capital at risk segment of the Swiss market.

The new UBS' Buy on Dips Note Linked to SMI is a growth and income structured certificate based on a combination of payoff types (portfolio insurance, range).

The product invests 50% of the initial capital in the SMI (risky asset) at the start level, and 50% is placed in a cash account (less risky asset), paying an interest of 3.00% p.a. (indicative). Each time the underlying is at or below a respective trigger level of 95%, 90% and 85% for the first time during the lifetime of the product, an additional 20%, 20% and 10%, respectively, will be invested in the SMI. At maturity, the investor participates in the positive or negative performance of the index with the capital invested in the cash account accruing interest which is also reimbursed at maturity quarterly.

"The structure is not specifically offered to monetise volatility," said Robin Lemann (pictured), head of public distribution equity derivatives at UBS in Zurich. "The buy on dips notes are rather participation products that enable investors to participate in the performance of an underlying and to potentially benefit from an additional regular coupon payment on the cash component."

The first UBS 'buy on dips' note was marketed in August and was linked to the Eurostoxx 50 Index, according to Lemann. "This product is aimed at investors who are anticipating short-term corrections in the SMI, but a positive overall performance until maturity. However, this structure offers a potential advantage compared to other participation products, as investors can participate in the underlying and, at the same time, benefit from a potential constant return or from a lower entry level into the SMI," said Lemann. "This could allow investors to take advantage of lower index entry levels in a negative market environment provided that the underlying recovers until expiry."

This kind of structure can also be offered on single stocks, although demand is mainly based on index underlyings, and that the bank is providing extra support for clients to understand the payoff structure as UBS is offering this structure for the first time at the Swiss Structured Product, according to Lemann. "The [buy on dips] structure gets mainly distributed internally to wealth management [clients], and each product comes with detailed product description explaining the [payoff] structure," said Lemann. "In addition to this, regular one-to-one sessions are offered to client advisors to ensure the relevant know-how transfer."

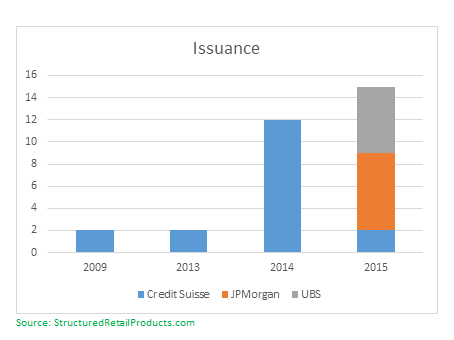

SRP data reveals that UBS is not the only issuer offering this kind of payoff structure in its offering, and that indices are driving issuance due to the difficulty to provide this kind of structure on the performance of company stocks: JP Morgan (seven products) and Credit Suisse (18 products) have been offering 'drop back certificates' featuring the Eurostoxx 50 (21 products), SMI (two products) and S&P 500 (two products).

The UBS Buy on Dips Note Linked to SMI closed its subscription period on December 11, and is listed on the Six Swiss Stock Exchange.

Related stories:

UBS readies 'high beta' ESG range

SEC orders UBS to pay $19.5m to settle charges relating to V10-linked notes

UBS names co-heads of ECM/corporate solutions Emea, di Stasi switches roles