FTSE Russell Indices has launched Idea (index data expertise & analysis), a weekly snapshot of the performance of Russell/FTSE indices and the factors affecting today's market activity.

To gain insight into the impact of certain market factors on US equity market performance in 2016, the index provider examined year-to-date performance through the lens of the FTSE USA Qual / Vol / Yield Factor 5% Capped Index, a new multi-factor index which measures performance of higher quality, lower volatility, dividend-paying US mid- and large-cap stocks.

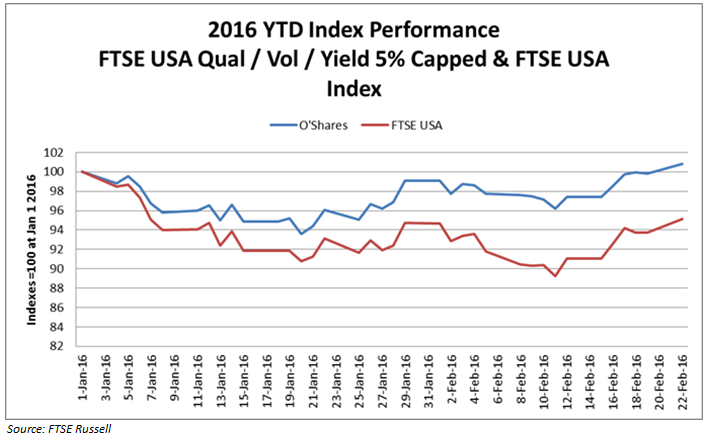

According to FTSE Russell, the FTSE USA Qual / Vol / Yield Factor 5% Capped Index has risen 0.8% year-to-date compared to a 4.9% decrease for the parent FTSE USA Index.

The latest FTSE Russell Idea highlights the shift towards the second generation of low vol-oriented investing, according to Guillermo Cano (pictured), director, alternatively weighted indexes at FTSE Russell. "If you recall, post GFC when dealing with low volatility single-factor low vol options worked well, but were often one-dimensional and used as one-size fits all," said Cano. "Low vol strategies work very well in certain market conditions yet in others, such as the 2013 market bull-run when the Russell 1000 was up by 33%, low vol strategies returned 23-25%. The risk of underperforming in such periods is pretty tangible. Sometimes this is labelled tracking error but the impact is real."

According to Cano, what we see now is that the combination of diverse factors such as quality, volatility and yield can be very complementary. "Low vol orientation goes beyond that single factor exposure and can extract value from other factors," said Cano. "Vol control strategies have been very popular in structured products because traditionally have constrained the volatility of mainstream and widely used indexes. This FTSE Russell Idea highlights a different approach. Rather than constrain the volatility of an index, with this control mechanism we are looking at these factors from the very beginning."

The index provider believes this approach will be appealing to investors because it provides complementary exposures. "For instance, there are times during the market cycle when the value factor has junk-like tendencies and some stocks that may look attractive from a value perspective but may actually be distressed," said Cano. "But if you combine value with a factor such as quality, it can simultaneously help investors get a little bit more of their desired exposure. That's the key element of this Idea."

The market seems to be moving towards a multi-factor approach, but FTSE Russell thinks that just because "you can combine factors it doesn't mean you should". Before developing any strategy or index, we examine academic and practitioner literature, and also approach this process with common sense, said Cano. "We first identify the theme we want to capture and run relevant back-testing. But we then ask ourselves if it is a sensible strategy for the end investor?"

According to Cano, there is no one size fits all when developing indexes as different indexes and weighting strategies can be used in different products. "Traditionally, investors with large cap weighted allocations have liked the liquidity/cost of that allocation but at times when markets are falling they can incur heavy drawdowns," said Cano. "Often when this occurs we have seen asset owners moving to deploy low vol strategies with their core cap weighted allocation, as a way to reduce the volatility and potential drawdowns."

In terms of usage, FTSE Russell believes that multi-factor indexes like the FTSE USA Qual / Vol / Yield Factor 5% Capped Index which can select stocks with specific characteristics are an important and innovative new tool for examining markets, complementing its offering and creating investable products.

"We have indexes that are broader oriented, lower cost and lower turnover that are very appealing to some conservative asset owners [and] we also have targeted strategies providing higher exposure/lower membership that can be appealing for ETF providers/users," said Cano. "This applies to structured products, as we offer indexes that can fit very well in products can be reproduced synthetically (long/short multi-factor index)."

The FTSE USA Qual/Vol/Yield Factor 5% Capped Index (FUSYQVCF) is designed to reflect the performance of high quality US Large and Mid Cap equities exhibiting relatively low volatility and high dividend yields. Constituents are selected and weighted based on quality, volatility and yield characteristics. The index is part of the FTSE Global Factor Index Series, a new suite of benchmarks designed to represent the performance of specific individual factor characteristics or a combination of these factors.

There are currently over 5,200 structured products featuring FTSE Russell indexes across jurisdictions that are still live

FTSE Russell targets product issuers with expanded global factor index range

FTSE Russell: Volatility is now an indicator of return

FTSE Russell: The merger will allow us to generate greater global exposure

FTSE Russell debuts 50% currency hedged index series

FTSE Russell rolls out new smart beta series as Source readies tracker