AnaCap Financial Partners (AnaCap), a specialist European financial services private equity firm, has entered into exclusive negotiations to acquire Barclays' French retail banking and wealth businesses including the bank's network of 74 branches, life insurance business, and wealth and investment management operations. Any potential transaction is subject to a mandatory consultation period.

Barclays will continue to operate its corporate and investment banking operations in France. Barclays' French retail banking and wealth business operations are focused on the mass-affluent segment, offering banking services such as current accounts, deposits and mortgages, as well as a variety of products including life insurance and wealth management.

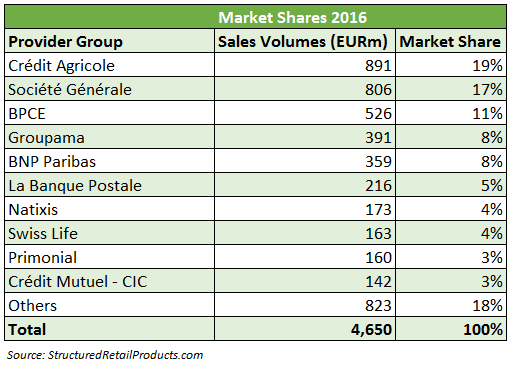

Barclays has been an active provider of structured products in France since 2004 and has been in and out of the top ten ranking on a regular basis sporting a 2-3% market share over the last five years. Year to date, Barclays holds a 3% market share on the back of €125m worth of sales.

The UK bank has marketed over 27,500 products among French retail investors mainly certificates, but also life insurance products (92), structured notes (69), structured funds (56), and structured savings plans (33).

It is understood that AnaCap will take over the management of 23,612 live products issued by Barclays investment bank, and sold through its commercial network in France, and will provide the French firm with more than €4.63bn of estimated assets under management (AUM) in structured products. Barclays declined to comment.

The investment would become AnaCap's latest addition to a growing banking platform which comprises Aldermore in the UK, which is now publicly listed on the London Stock Exchange (LSE); MeDirect in Belgium; Mediterranean Bank in Malta; Equa bank in the Czech Republic; and FM Bank in Poland. In addition, the acquisition would mark the firm's second French investment, following the buyout of AssurOne Group, a digital insurance broker, in 2014.

"This is an opportunity to acquire an attractive and established banking operation built on a team of highly talented individuals with exceptional relationships with customers across France," said Nassim Cherchali, director of AnaCap, in a statement.

Jes Staley (pictured), Barclays Group chief executive, said that "accelerating the disposal" of the bank's non-core unit is the "key to creating a simpler, more focused Barclays", and to eliminating the drag on the performance of its "strong core business".

Barclays sold its Asia Wealth business in Singapore and Hong Kong earlier this month to the Oversea-Chinese Banking Corporation (OCBC), as part of its non-core disposal which also includes the sale of its retail banking, wealth and investment management and part of its corporate banking business in Portugal to Spain's Bankinter for about €175m (£128m), and to CaixaBank (formerly La Caixa) in Spain. Other recent non-core disposals include the sale of its Barclays Risk Analytics and Index Solutions (Brais) to Bloomberg for approximately US$790m (£520m). Barclays also announced in December 2015 that it was exiting its Bmarkets business in Europe which operated in France, Italy, Germany and Switzerland.

"Barclays' French retail and wealth and investment management business is attractive, but no longer fits with our strategic ambitions," said Staley, in a statement. "This transaction, once completed, would effectively finish our exit from Continental European branch-based retail banking."

The bank's non-core risk-weighted assets (RWAs) started at £110bn two years ago and had been reduced to £47bn by the end of 2015. Staley also said that as the bank concludes its restructuring, "we are taking the opportunity to exit other marginal businesses and regions, including elements of the investment bank in nine countries, our Egyptian and Zimbabwean businesses, Southern European cards and wealth management in Asia". As a result, our non-core RWAs increased to approximately £55bn as at the end of 2015, while the banks expects that those one-time additions will add approximately £600m to underlying non-core costs, and plans to exit the majority of these in the course of 2016.

Barclays also announced in its Q1 2016 results that it will operate as two clearly defined divisions, Barclays UK and Barclays Corporate & International, and reported a 25% slump in Q1 profits and losses on oil-related loans. Despite the bank currently undergoing a restructuring it reported Q1 profits of £793m and a 15% rise in bad debts, on the back of client difficulties in the oil and gas sector. Barclays has announced that its corporate & international business will "ultimately become our non-ring-fenced bank".

The UK banking group reported that profit before tax in its investment banking operations increased 17% to £1,611m. Income remained flat despite reductions in RWAs while 'costs decreased as a result of improved cost efficiency and a reduction in costs to achieve'. Total income was broadly flat at £7.5bn (2014: £7.5bn), including the appreciation of the average USD rate against GBP.

Banking income was flat at £2.5bn (2014: £252bn). Investment fee income reduced 1% to £2,093m driven by lower equity underwriting fees, partially offset by higher financial advisory and debt underwriting fees. Lending income increased to £436m (2014: £417m) due to lower losses on fair value hedges.

Markets income was broadly flat at £5.03bn (2014: £5,04bn). Credit income decreased 5% to £995m driven by lower income in securitised products as a result of the accelerated strategic repositioning in this asset class and lower income from distressed credit. This was partially offset by higher income as a result of client driven credit flow trading.

Equities income decreased 2% to £2bn driven by lower client activity in Europe, Middle East & Africa (Emea) in equity derivatives, partially offset by higher performance in cash equities. Macro income increased 4% to £2bn due to higher income in rates and currency products reflecting increased market volatility and client activity.

Credit impairment charges of £55m (2014: release of £14m) arose from a number of single name exposures. Total operating expenses decreased 5% to £5.9bn reflecting a 5% reduction in compensation costs to £3.4bn and lower costs to achieve. Derivative financial instrument assets and liabilities decreased 25% to £114.3bn and 24% to £122.2bn respectively, due to net trade reduction and increases in major interest rate forward curves.

The investment bank's trading portfolio assets decreased 31% to £65.1bn primarily driven by balance sheet deleveraging, resulting in lower securities positions. Overall, total assets decreased 18% to £375.9bn due to a decrease in derivative financial instrument assets, trading portfolio assets, and settlement and cash collateral balances within loans and advances to banks and customers.

Barclays also reported that investment banking RWAs decreased 12% to £108.3bn mainly due to a reduction in securities and derivatives, and improved RWA efficiency.

Click in the link to read the full report.

Barclays completes sell-out of Iberian retail and insurance businesses

Barclays' reports progress offloading non-core businesses

Barclays targets insurers with CPPI module

Barclays unplugs European listed structured products business

Barclays assets increase due to derivatives, but profits fall

Barclays enters new phase for structured products