Australia's structured products market remained broadly limited to open architecture distribution and bespoke spaces in September, with only Citi active in the closed end, issuing the latest iterations of its MLI Coupon Plus series.

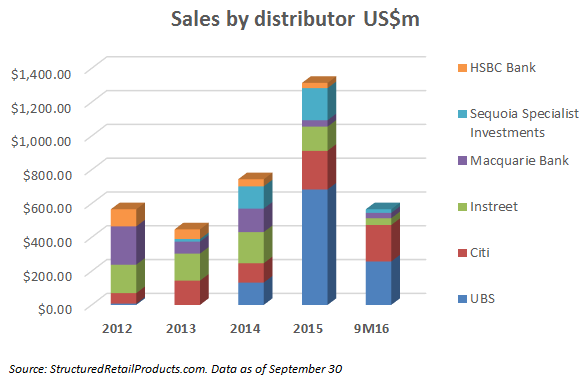

Citi continued edging closer to UBS, the leader in the closed-end products. As of the end of September, Citi has accounted for 47% of the total number of products issued this year, and 38% of the aggregate sales volume. These compare with 32% and 14%, respectively, for the same period of 2015. In comparison, UBS had accounted for over 50% of sales in 2015, but is down to just over 45% in the first nine months of this year.

The modest line-up in September, consisting only of Citi's MLI Coupon Plus 22 through 24 offers, in both Australian and US dollars, comes after a more diverse range in August, when 12 products were added to the SRP Australia database.

While September's offers had few exciting names, in August Sequoia Specialist Investments launched two boutique products that offer leveraged bets on companies involved with the clean-energy disruption in the energy and transportation sectors. The Sequoia Accelerated Return Units Series 1 is a three-year growth product linked to the performance of Tesla Motors and offers 200% participation in the upside of the electric car manufacturer. The Sequoia Launch Series 23 is a three-year growth and income product based on an equally-weighted basket of five clean-energy stocks: lithium miner Albemarle Corp, electric car makers BYD (H Shares) and Tesla Motors, and battery manufacturers Panasonic and Samsung SDI. The product features 100% capital protection and annual coupons of up to 6.3%, subject to the basket's performance for the first two years, in addition to a final coupon of up to 50%.

Capital protection remained off the radar in the closed-end part of the market. As of September 30, only 16% of the products added to the SRP Australia database this year have had full capital protection, with the remainder enjoying zero protection. This compares with 19% of products having full protection in the previous comparable period.

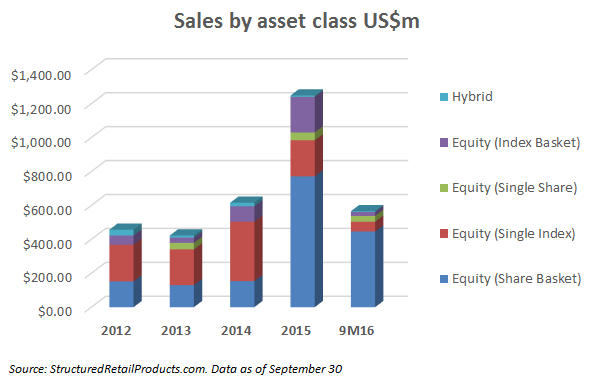

Similarly, the breakdown of sales by asset classes continued to favour equities, particularly share baskets, which accounted for 83% of the aggregate sales volume in the nine months ended September. This compares with 62% for the same period of 2015.

Investment terms for products added in September remained in line with the strong local trend of medium terms of between two and six years. In the year-to-date, over 95% of all product terms have been in this range, as compared with 87% for the same period in 2015.

On the regulatory front, the Australia Securities and Investments Commission (Asic) noted in its new four-year plan, published in early September, that the disconnect between structured products' designs and retail investors' understanding of the structures remains one of its primary concerns. 'Traditional' complex products (such as margin lending and capital protected products) have been on the decline since the 2008 financial crisis, according to Asic. This dynamic, however, has been counterweighted by an increase in demand for hybrids, as investors hunt for higher yields amid low interest rates and providers seek to cover buffed up capital requirements.

'As products and services become more tailored, there is a risk that consumers may not understand them or will be unable to adequately compare them to alternatives due to increased complexity,' stated the report. 'Our challenge is to support the benefits of financial innovation - such as lower costs and more tailored products - while managing the risk that products may not align with consumers' needs or understanding.'

A new 'retail structured products sales and advice practices' surveillance project will be launched, covering hybrids, complex structured products, and over-the-counter derivatives. The commission will also set out on fresh initiatives to monitor exchange-traded funds issuers' liquidity and the mis-selling of add-on insurance products.

In warrants, the Australia Exchange (ASX) saw the average daily turnover fall a further 11.5% to A$6m (US$4.6m), for a total monthly figure of A$133m in September. The S&P/ASX 200 remained the most popular underlying with 17.9% of trade, up from 14.3% in August, ahead of the Australia/US dollar forex pair at 10.2% and Commonwealth Bank of Australia at 9.8%, which were at 10.7% and 11.0% in August, respectively.

The full Australian market review for September will appear shortly.

Asic points at misalignment between product design and client needs

Asic releases digital advice framework

Trading activity pre-Brexit drives better ASX results in FY16