The sales volume of equity-linked structured products in South Korea last month dropped as redemption volume remains sluggish amid the increased market volatility.

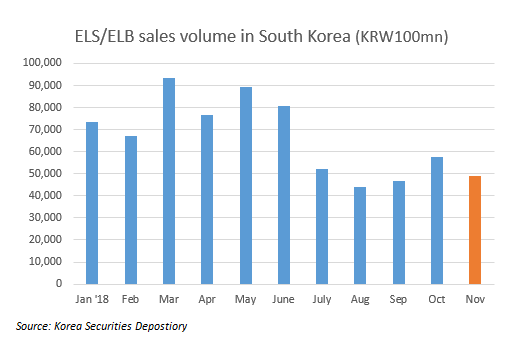

The new issuance volume for November came in at KRW4.89 trillion, down from October’s KRW5.76 trillion, according to Korea Securities Depository (KSD). The figure involves both equity-linked securities (ELS) and equity-linked bonds (ELBs).

The sales volume for new ELS issuance in November dropped over 35% from the previous month to KRW3.4 trillion, dragging down the overall sales growth of equity-linked products.

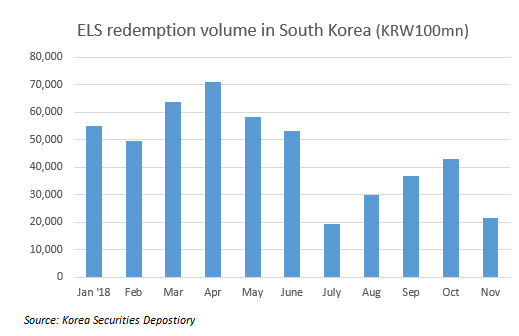

The drop mainly stems from the faltering redemption volume that stood at KRW2.1 trillion last month, halving from October’s KRW4.3 trillion. The drop in the amount of redemption means investors are less likely to make new investments as their cash is ‘locked in’ with the products that failed to mature.

“The Q4 sales volume will drop drastically from the first half of this year as investments are not being redeemed, limiting the amount of funds that can be re-invested in new ELS products,” said Gyun Jun, a derivatives analyst at Samsung Securities in Seoul.

South Korea is the world’s largest market for products with autocall structures that track the worst performance of two or more equity indices. The Hang Seng China Enterprises index (HSCEI) and Hang Seng Index (HSI) are benchmarks that are typically included in the index basket because of their volatility.

After dropping sharply in June this year, both HSI and HSCEI continued to be on a downward trend, resulting in structured products linked to the indices to miss their upside barriers or the so-called ‘knock-out’ levels.

The autocallables in South Korea generally have a three-year maturity. Issuers as well as investors of the products, however, expect the products to expire before their actual tenors, usually within a year, as they have an upside and a downside barrier that enables the product – as the name indicates – to be automatically called or expire.

Investors will rake in coupons on top of their principal if the upside barrier is breached but may lose the capital invested if the lower barrier is touched.

Sluggish H2 ELS/ELB sales compared to H1

November’s decline in ELS sales also ends a short-lived rebound posted a month earlier. In October, the sales volume of ELS products climbed to KRW5.3 trillion, up around 30% from September and surpassing the KRW5 trillion mark for the first time in the second half of this year.

Although the redemption volume was on the rise in October to boost the new issuance, industry sources mainly attributed the uptick to a local securities firm’s aggressive sales practices to raise its market share. Mirae Asset Daewoo issued almost KRW1 trillion worth of ELS products in October, becoming the largest issuer during the month, according to data from KSD. Mirae had a market share of around 18% in October.

Still, the rise in October fell short to match the average monthly sales volume reached in the first half of this year that came in at over KRW7 trillion. The figure for March stood at close to KRW9 trillion.

Last month’s drop in overall sales of equity-linked products also came despite an increase in the sales volume of ELBs, which rose to KRW1.4 trillion from KRW0.4 trillion in October. The rise is attributed to the local retirement pension funds generally rolling over to new products at the end of the year.

“The ELB sales volume spike in November and December will partially compensate the drop in sales of ELS products,” said Jun. “The sales volume for ELBs in December last year came in at KRW1.3 trillion.”

On the back of this trend, Kospi 200, by itself, became the third most popular underlying asset across the globe in November, according to SRP data. The South Korean benchmark is a widely cited single underlying index for the ELB products.

Declining ELS redemption

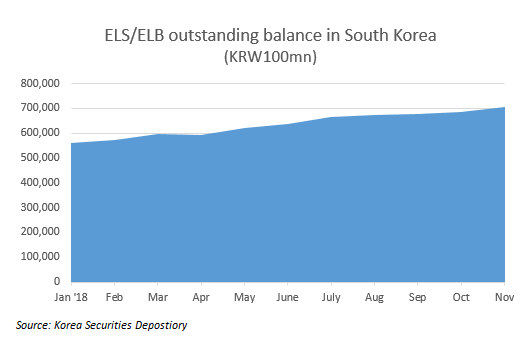

Despite the sluggish growth in the new issuance during the second half of this year, the outstanding balance of equity-linked structured products – ELS and ELBs – in South Korea is on a steady rise. The amount exceeded KRW70 trillion as of December 14, 2018.

“It’s a positive development if the outstanding balance is rising on the back of new funds flowing into the market,” said Jun. “But if the rise in the balance is coupled with a declining new issuance volume, that means early redemption is not triggered, resulting in rising hedging costs for the issuers.”

The early redemption volume for ELS products dropped to under KRW2 trillion in November, from over KRW4 trillion and KRW3.4 trillion in October and September, respectively. In July, right after both HSCEI and HSI plunged, the figure sunk to KRW1.7 trillion from KRW4.7 trillion posted in June.

When breaking down the outstanding balance of all equity-linked structured products by company, Mirae held the largest amount with KRW12.4 trillion, followed by Korea Investment & Securities, NH Investment & Securities, Samsung Securities and KB Securities.

Around 60% of the products that local securities firms issue in South Korea source the ELS swap from global investment banks.