The risk management concept of value-at-risk (VaR) is a well-known and accepted framework which has importance in all aspects of financial analysis and trading desk operations.

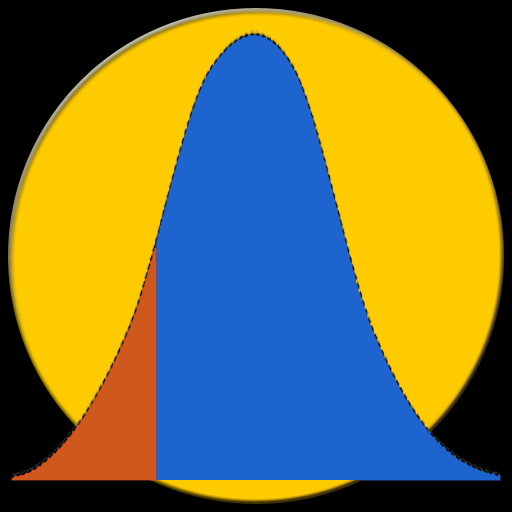

The purpose of this concept is to examine near worst cases and to establish the level of loss that could occur. The simplest every day way to measure risk is volatility (standard deviation). This applies to mainstream instruments such as indices, stocks and bonds through to funds or portfolios created from them. Its popularity lies in its easy calculation and its universal usage dating back to the origins of Modern Portfolio Theory and before. However, volatility is a central and symmetri