The US electrical vehicle company achieved its best-ever net income, operating profit and gross profit in the third quarter of 2021. However, as underlying for structured products its fortunes were mixed during that period.

In this article we dive into the SRP database to see how structured products linked to the Tesla share fared in Q3 2021. We review the main markets, top issuers, payoffs and take a closer look at the listed products in Germany.

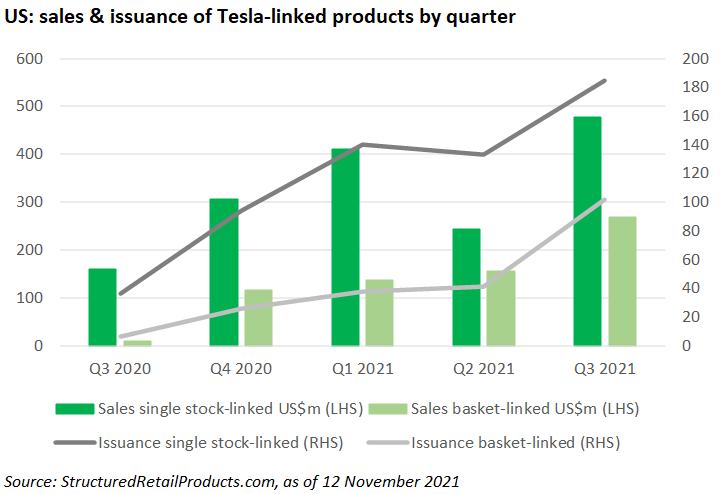

In the US market, sales volumes of structured products linked to the Tesla stock increased by 260% YoY in Q3 2021.

Some US$617m was collected from 217 Tesla-linked Tesla-linked products that were issued between 1 July and 30 September 2021, compared to US$170m from 42 products in the prior year quarter.

Although the bulk of the sales, at US$405m, came from 140 structures linked to the Tesla share on its own (Q3 2020: US$159m from 36 products), the biggest increase – both by issuance and sales volumes – was provided by products where the share was part of a worst-of basket: US$212m from 77 products in Q3 2021 compared to a US$10m from just six products in Q3 2020.

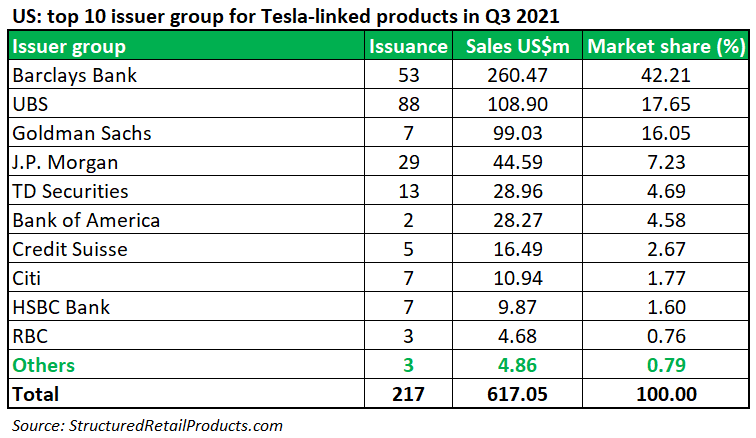

Barclays was the number one issuer of Tesla-linked products in the quarter, collecting US$260.5m from 53 structures. These included the bestselling contingent income autocallable securities, which were distributed via Morgan Stanley Wealth Management and accumulated sales of US$48.5m.

Mid October, Barclays reiterated an underweight call on Tesla (TSLA) as it hiked the electric vehicle maker's price target to US$300 from US$230. ‘Despite our scepticism around Tesla’s sky-high market cap of US$800 billion, we are constructive on the stock going into the Q3 EPS (earnings per share) release due to the combination of the delivery beat driving operating leverage and strong pricing,’ said analysts led by Brian Johnson.

Other active issuers in Q3 were UBS (US$110m from 88 products), J.P. Morgan (US$45m from 29 products), and Goldman Sachs (US$100m from seven products). The latter raised Tesla’s price target to US$1,125 (from US$905m) after Hertz said it had ordered 100,000 electrical vehicles by the end of 2022.

‘We believe that it will help the company to sustain strong growth and margins when considering the order in the context of other dynamics,’ stated Goldman Sachs analyst Mark Delaney.

Outside the US, there was strong issuance of Tesla-linked products in Taiwan, although none of the 171 products issued in Q3 were tied to the single stock, with investors preferring a worst-of basket comprising up to three shares instead.

The Taiwanese products, which were issued via DBS Bank (150) and Société Générale, were targeted at private banking investors.

The 57 Tesla-linked products in South Korea were fairly evenly split between baskets (30) and single stocks (27) while in Germany, 42 out of a total of 45 primary market products were linked to Tesla on its own, compared to no products at all in Q3 2020. The share was also in demand as underlying for structured products in Switzerland (31), Canada (26), and Italy (17).

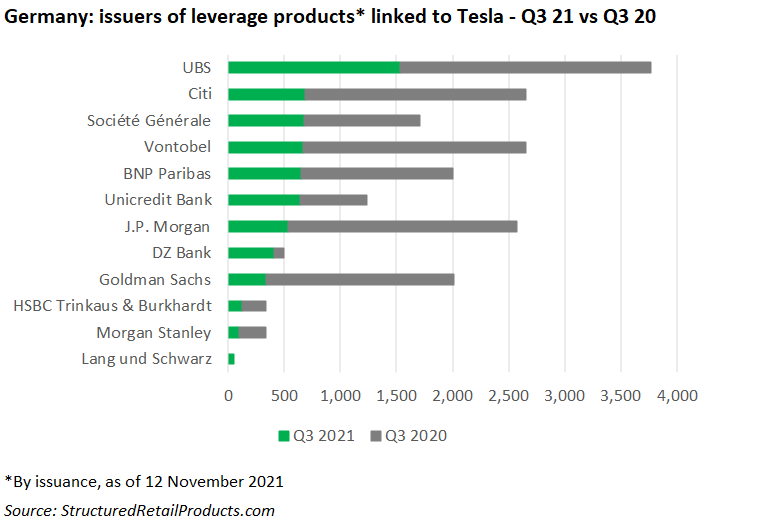

However, despite the success of the traditional tranche products, leverage certificates linked to Tesla fared less well during the quarter.

In Germany, where more than 90% of these certificates are listed, there were 6,418 Tesla-linked turbos issued in Q3 2021, a decrease of 52% YoY (Q3 2020: 13,438).

Of the 12 providers active in the quarter, only DZ Bank and Unicredit increased their issuance compared to Q3 2020 – by 320 and 51 products, respectively.

UBS remained the number one issuer, with 1,532 products (Q3 2020: 2,239), followed by Citi (684) and Société Générale (679), whose issuance was down by 1,283 and 356 products, respectively, from the prior year quarter. Vontobel (669) and BNP Paribas (646) completed the top five.

Tesla’s total revenue, at US$13.8 billion, grew 57% YoY in Q3 2021, while its operating income improved to US$2 billion compared to the same period last year, resulting in a 14.6% operating margin.

The company’s quarterly results really caught the eye, according to Jean-Paul van Oudheusden, owner, Markets Are Everywhere.

‘Many people still see Tesla as a car manufacturer, but it actually is a big technology company and that explains its high rating,’ stated Van Oudheusden, in his weekly Turbo Journal.

According to Van Oudheusden, car manufacturers generally have margins of around 10% while tech companies on the other hand have much bigger margins of around 50%.

‘Investors want to see Tesla valued as a tech company and not as a car company, and this is a strong signal that it's really heading in that direction,’ he said.

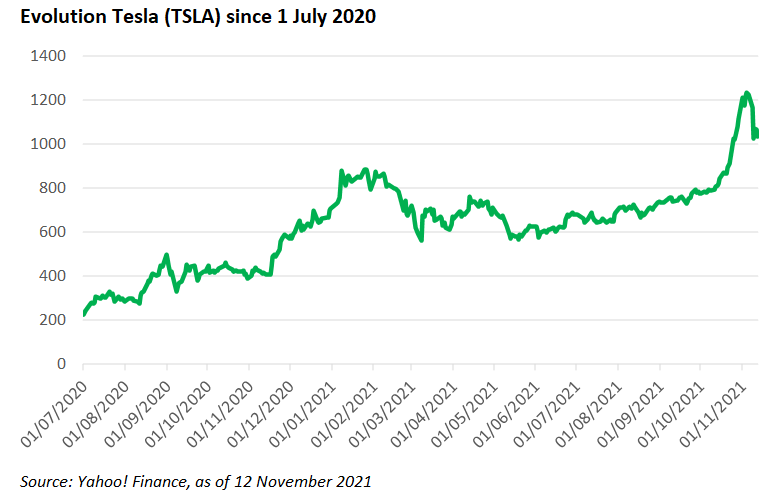

As of 12 November, when it closed at 1,033 points, the Tesla share had increased by 41.6% since the start of the year.

Click the link to read the full Tesla Q3 2021 results.

SRP is the leading source of data intelligence on structured products globally, enabling you to plan for the future, gain market insights and compete strategically. Contact us to try a free a demo.

Image: Austin Ramsey/Unsplash