Market players talk about how implied volatility is managed by trading desks, and its role in triggering the shift away from traditional equity index-linked autocallables and reverse convertibles structures.

Issuers of structured products use several ways to offload implied volatility. The easiest way is to go into the inter-dealer broker market and see if there are any matching interest within hundreds of participants - these can be other banks but also market makers, and hedge funds, according to Pierre Roussel, head of EIS stocks trading, Crédit Agricole CIB.

“Liquidity will mainly depend on underlying and maturities, but trades will always be listed derivatives,” he said. “For less liquid underlyings, it is possible to macro hedge the volatility exposure with more liquid ones - main indices in general.”

Another way is to structure products that can help to mitigate the volatility risk, said Roussell. “We can think about simple payoff diversification with usual clients to more sophisticated products that can be traded with more advanced clients such as hedge funds.”

The structured products market is a very interesting space for hedge funds because it offers opportunities - Tom Karlsson, Dunn Capital

Active investors like hedge funds and market makers want to see where the structured products flow is as this can affect the dealers option positioning.

Trading desks look at S&P 500 index flows, for instance, to see if dealers are short or long gamma - if there's a level where dealers are short gamma, and the index goes down, issuers need to start hedging their gamma if they're short.

The selling pushes the market even lower and escalates the need to sell even more which adds some volatility to the markets. When dealers are long gamma that dampens the volatility because they start buying when the market goes lower, and they start selling when the market goes higher.

“Hedge funds are looking at where the flows are, what kind of products are sold, where are the strikes and the peak Vega – the level at which knocking puts are set,” said Tom Karlsson (right), director of volatility strategies at Dunn Capital.

“The structured products market is a very interesting space for hedge funds because it offers opportunities – the flow may be so one sided that some volatility becomes very cheap to buy and some volatility becomes very expensive to sell. It’s not only the arbitrage opportunities but also about having good trade entry points.”

Hedge funds and market makers are always seeking opportunities to buy cheap volatility so they tend to look a the longer dated implied volatility levels of an index and “where the structured product flow is pushing the volatility down too much and there is little liquidity to hedge in longer dated maturities”.

Dividend risk

If there is a lot of option activity this might affect the implied volatility and dividend levels which in turn may open attractive trading opportunities for these firms as the market flows are not always balanced.

“Longer dated dividends have had constant selling pressure as banks need to hedge their long dividend risk exposure. In times of risk-off market this risk can trade very attractive levels and you can earn a good yield carrying this illiquid risk,” said Karlsson.

“That is what happened with the Covid crisis of 2020 when companies stopped paying dividends, and it became a real risk for the market, but also an opportunity. Issuers reacted quickly and addressed the problem with decrement or synthetic dividend indices - clearly a good way for banks to hedge that risk and pass some of that premium on to investors.”

The dividend risk generated by structured products has become a key theme since 2020, according to Conor McCann (right), equity derivatives trader, Susquehanna International Group.

“There was certainly a lot of stress in March 2020 and the structured products market has been an area of the marketplace where we've had to step into in a more serious manner,” said McCann, during the volatility panel discussion at SRP Europe 2022. “The introduction of decrement indices is a good example of the innovation triggered by the industry which moved fast to come up with ways to manage and reduce these risks.”

According to McCann, the dividend risk has been reduced across the marketplace, on average, but there are still occasions when dividend risk is coming under stress.

“I think that is still very much an important risk for us all to manage,” he said. “A lot of the work that has gone into the last two years and being more focused on this risk has also provided a better framework to manage the risk and have an orderly market in terms of the dividend risk compared to 2020.”

Indices v stocks

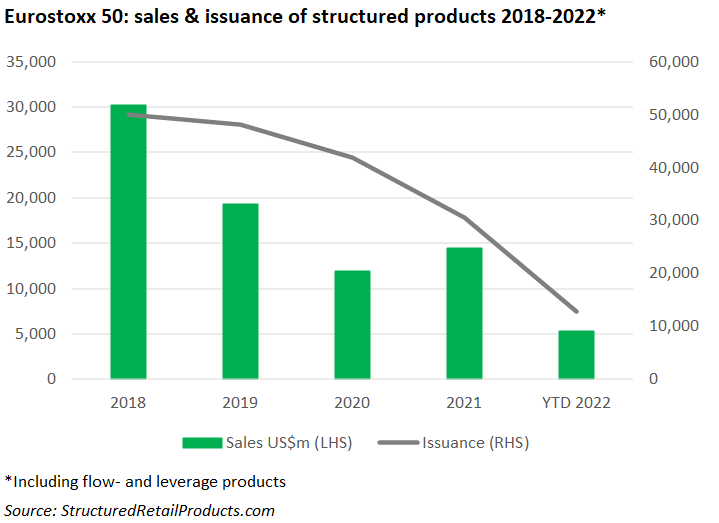

The shift away from traditional market cap indices for autocallables or reverse convertibles began before Covid as very low long dated index implied volatility was already seen in benchmark indices such as the Eurostoxx 50 which was declining through the back end of 2018.

Coming out of Covid there's been an industry-wide switch towards trading single names, which in turn has meant the stock-to-stock correlation levels are more important nowadays, than the index-to-index correlation levels might have been in the past.

The impact of structured products issuance moving away from indices and more towards single stocks over the last couple of years has left an environment where index skews have been very steep and stock skews have been a lot flatter, which is conducive to looking for risk adjusted ways to buy downside vol and skew on single names.

“You end up with a trade that is long on the single name vols, in the region where the vol is more accessible,” said a senior banker who preferred to remain anonymous.

By mirroring the underlying autocallable risk issuers can recycle their spot to dependent Vega and offer competitive and quite attractive trades in terms of the underlying risk premium.

“We generally recommend trading it in an equal Vega format,” said the banker. “Normally when you do a correlation trade, you'll tend to sell more Vega and more vol exposure on the index leg than you buy on the stock legs and that just represents the difference in the strikes that you're trading it turns into more of a pure correlation trade.”

Outlook

As of today, the Russia-Ukraine conflict remains the main cause for realised volatility in the market, but central bank policies, economic data (jobs, ISP, PMI) and company results are contributing to the shift in the volatility regime.

This realised volatility, according to Roussel, is also a big driver of the implied volatility “we observe every day”.

“The war may have consequences for growth and will increase the issues we already had in the past six months with inflation likely to be a big challenge all over this year,” he said.

Karlsson believes the current volatility comes from higher inflation and interest rates as opposed to geopolitical events like the war.

“Those are going to be more persistent,” he said. “history suggests that there is a high risk of a recession, and obviously in this kind of environment volatility and uncertainty will be high. We should also consider how the markets are going to take the projected rate hikes if the inflation continues to be high.”

In this environment the best products are those that can get a carry and can earn some yield selling that high volatility. Barrier strategies can be hard to structure because it is difficult to time the market going down, but in the current market they provide enough buffer to cope with sharp moves as long as investors manage their risk and trade small enough, according to Karlsson.

“Market neutral type of structures and bullish structures specially with Asian assets by selling up puts and buying multiple call options to have a nice leverage on the upside would probably add value to any portfolio,” concludes Karlsson. “Similarly, in Europe, you can probably benefit from selling short-term downside puts to get a good yield, and in the longer dated maturities replacing the long stock portfolio with call options could build a nice payout profile.”

Like volatility the structured products market moves quickly and those manufacturers that can keep up and react with opportunistic trades will have an edge with investors as long as they have the risk appetite to hedge those volatile positions or find someone externally willing to cover the risk.

SRP is the leading source of data intelligence on structured products globally, enabling you to plan for the future, gain market insights and compete strategically. Contact us to try a free a demo.

Image: Engdao/AdobeStock