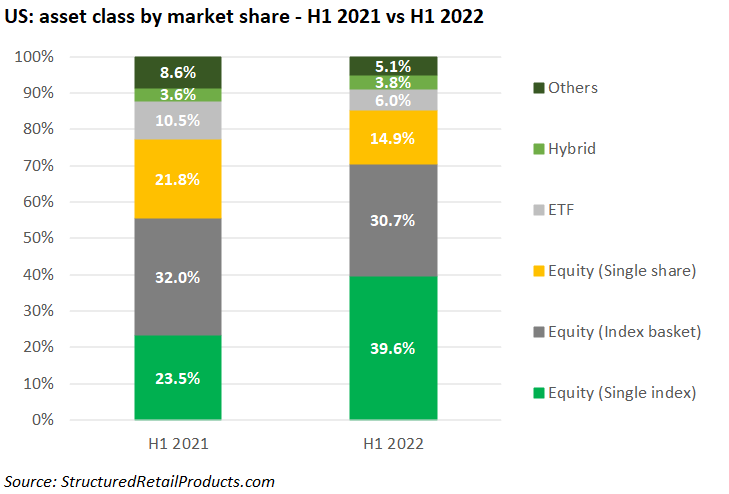

There was a significant shift towards products linked to single indices in H1 2022.

Some $48.9 billion was collected from 16,330 structured products in the first half of 2022 – a 5.3% decrease in sales volumes compared to the prior year semester (H1 2021: $51.6 billion from 15,832 products).

Products were linked to 14 different asset classes, of which the top five claimed a combined market share of 95% (H1 2021: 15).

The single index was the dominant asset class with a 39.6% share of the US market – up 16.1% year-on-year (YoY).

The 4,012 products linked to a single index sold a combined $19.4 billion, with 72% of the total volume tied in products on the S&P 500 ($14 billion from 2,471 products). Some $1.5 billion was collected by 342 products linked to the Eurostoxx 50 while the 266 products on the Russell 2000 also sold north of $1 billion.

And it wasn’t just the household names that performed well. Newcomers such as the MerQube US Tech+ Vol Advantage Index and MerQube US Large-Cap Vol Advantage Index collected $58m and $33m, respectively, while the proprietary Citi Dynamic Asset Selector 5 ER Index also held its own, accumulating $150m from 70 products – level on H1 last year.

The excellent performance of single index-linked products came at the expense of structures linked to index baskets, single stocks and, to a lesser extent, exchange-traded funds (ETFs).

The former saw its market share drop to 30.7%, down 1.3% YoY, while products linked to a single claimed 14.9% of the US market at the end of the semester, a decrease of 6.9% from the prior year period. The share of Tesla was the most popular, with sales of $625m from 302 products, followed by Apple ($605m) and Nvidia ($303m).

ETFs captured six percent of the market (H1 2021: 10.5%) with SPDR S&P 500 ETF Trust by far the dominant fund, collecting $1.3 billion from 256 products.