Single indices were the dominant asset class with decrement indices alone responsible for 70% of the total issuance.

Some C$10.5 billion (US$7.6 billion) was collected from 3,151 structured products in the first half of 2022. Despite an increase in issuance, sales volumes were down 17% compared to the prior year period (H1 2021: C$12.5 billion from 2,932 products).

Average volumes, at C$3.3m, were also down compared to H1 2021 when products sold on average C$4.3m.

Products were linked to nine different asset classes, of which the top five claimed a combined market share of 98.8% (H1 2021: nine).

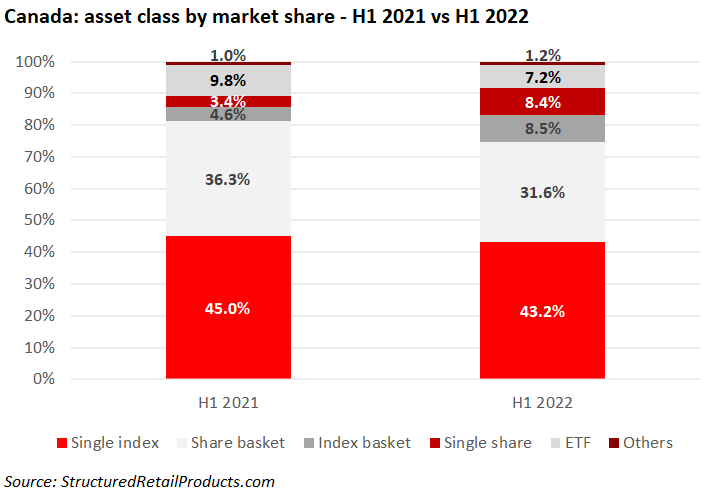

The single index was the number one asset class with a 43.2% share of the Canadian market, slightly down on H1 2021.

The 1,756 products tied to a single index sold a combined C$4.5 billion. Thirty different indices were used during the semester – including 14 decrement indices, nine of which were sponsored by Solactive.

Decrement indices were used in 70% of all products linked to a single index (H1 2021: 79%) with the top three comprising of Solactive Canada Bank 40 AR Index (390 products), Solactive Equal Weight Canada Banks 5% AR Index (204) and Solactive United States Big Banks AR Index (132).

Structures linked to a basket of shares collected C$3.3 billion from 568 products – the equivalent of a 31.6% market share – while baskets of indices achieved sales of C$885m from 298 products (8.5% market share).

Products linked to a single stock saw their market share increase to 8.4%, up five percent YoY. They accumulated sales of almost C$880m (212 products) with the share of Tesla (78) frequently used.

Exchange-traded funds captured 7.2% of the market (H1 2021: 9.8%). A total of 278 products worth C$755m were linked to exchange-traded funds. Of these, iShares S&P/TSX 60 Index ETF was the most popular, seen in 72 products.