J.P. Morgan remained the number one issuer in a quarter which saw BBVA and Nomura return to the US market after a lengthy absence.

Some US$33.6 billion was collected from 9,741 structured products in the third quarter of 2023 – up 13% from the prior year period (Q3 2022: US$29.9 from 8,325 products).

Average volumes, however, at US$3.5m per product, were slightly down on the same quarter last when products sold on average US$3.6m.

Twenty issuer groups were active in the quarter (Q3 2022: 19). BBVA and Nomura were new issuers this quarter. The former made its first appearance on the SRP US database since March 2020 while Nomura was seen for the first time since January 2016.

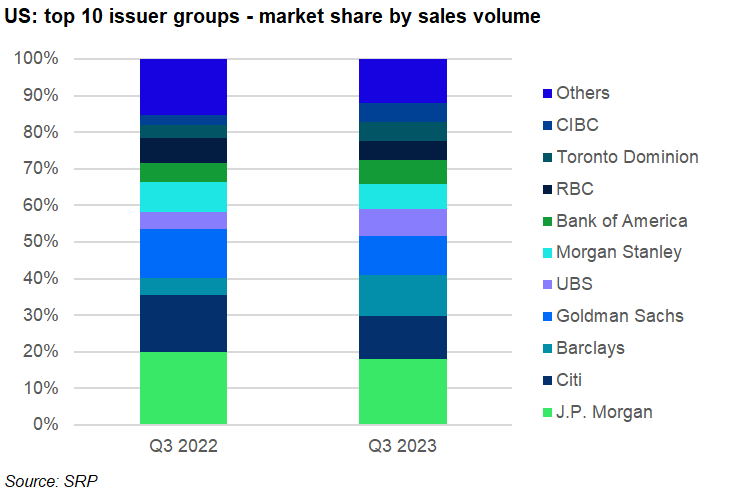

The top two issuers remained unchanged with J.P. Morgan once again the most prolific issuer during the quarter followed by Citi in second.

JPM claimed an 18% share of the US market with sales of US$6.1 billion from 2,158 products – an increase of 1.7% by sales volume year-on-year (YoY) – while Citi held 12% of the market as it accumulated US$4 billion from 1,194 structured products.

A large chunk of J.P. Morgan’s sales, at US$4.2 billion, came from 1,599 products linked to an equity index, with the S&P 500 the most frequently used, either on its own (US$1.6 billion from 400 products) or as part of a basket – often in combination with the Russell 2000, Nasdaq 100, or DJ Industrial Average (US$1.2 billion from 601 products).

Citi saw its market share fall by 3.75 percentage points YoY. Like JPM, more than half of its sales came from products tied to equity indices, with the S&P again the preferred option (US$1.6 billion from 555 products).

Barclays completed the top three, claiming an 11.2% market share (Q3 2022: 4.8%) from 917 products worth a combined US$ 3.8 billion. Its preferred index was the Russell 2000, mostly as part of a basket (US$1.7 billion from 510 products). Barclays’ offering included the Synthetic Convertible Notes (06741W7A2) on the Class A common stock of Alphabet, which, with sales of US$450m, was the best-selling US product of the quarter.

Goldman’s market share dropped to 10.7%, while that of UBS, at 7.4%, was up by 2.8 percentage points. Morgan Stanley and Bank of America both held a 6.7% share of the US market.

Three Canadian banks made the top 10: Royal Bank of Canada (RBC), Toronto Dominion Bank and Canadian Imperial Bank of Commerce (CIBC). Each collected sales of around US$1.8 billion, which translates in a market share of 5.2%.