Nvidia-linked equity-linked investments (ELIs) continue to gain traction.

The Hong Kong structured products market has seen a strong start to the year.

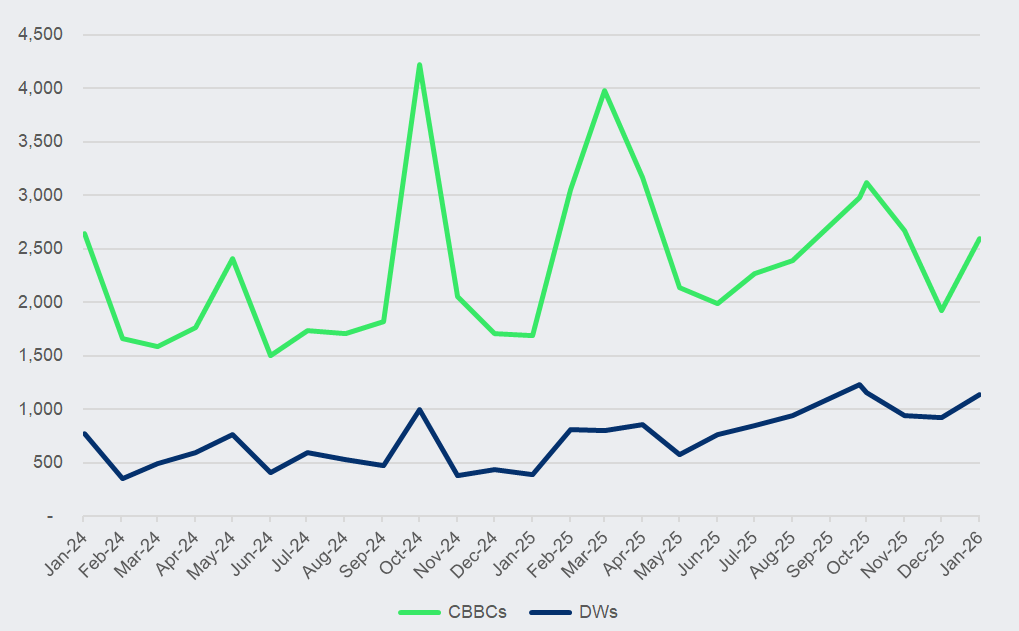

The average daily turnover for listed products – consisting of derivative warrants (DWs) and callable bull/bear contracts (CBBCs) – surged 91% to HK$22 billion (US$2.8 billion) in January compared with last year’s same period, the Hong Kong Exchanges and Clearing (HKEX)’s monthly statistics report shows.

DWs’ average daily turnover rose more than 77% year-on-year to HK$7.8 billion in January, while CBBCs’ doubled to HK$14.2 billion.

Listings for DWs surged two times to 1,141 products in January compared with a year ago, according to SRP data. CBBCs’ listings also grew to over 2,500 products from some 1,600 in the prior year’s same period.

Hong Kong SAR: listed structured product monthly listings - January 2024 to January 2026

Source: SRP

On the unlisted structured products front, over 7,500 equity-linked investments (ELIs) and 2,100 structured deposits were issued in January that sold to the city’s retail segment.

Underlyings, payoffs

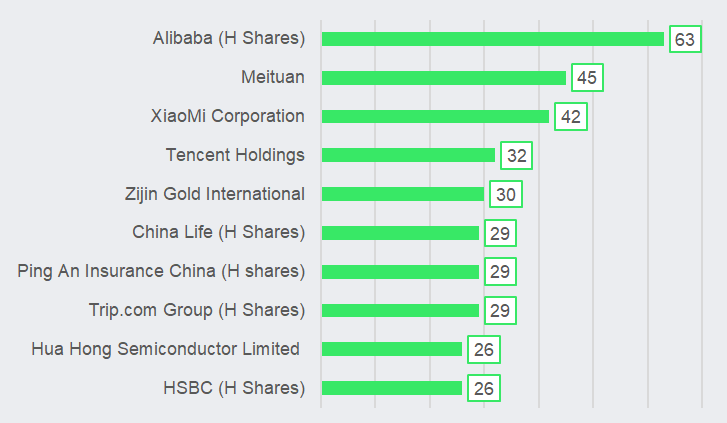

Alibaba (H Shares) topped the underlying league table for DWs, with warrants tracking the Chinese e-commerce stock seeing 63 listings in January, up from 16 in the prior year’s period and 24 in the prior month.

Shares of the Chinese tech giant were also the most-traded stock underlying for warrants in January, HKEX’s data revealed, recording an average daily turnover of over HK$1 billion. Roughly 80% of these turnovers came from call warrants.

Meituan and Xiaomi followed closely, with 45- and 42-linked warrant listings, respectively.

Hong Kong SAR: top 10 underlyings used in DWs in January 2026

Source: SRP

Zijin Gold International, which went public in Hong Kong SAR at the end of last September as the world’s largest gold mining listing of 2025, saw 30 related DW listings in January, which consists 24 call and 6 put warrants.

Another gold-related exposure, SPDR Gold Shares, recorded 25-exposed warrant listings – 14 of which were call warrants. The latest listings also reflected an increase from just two products last year’s same period.

For CBBCs, Hong Kong’s benchmark Hang Seng Index continued to dominate as the most-used asset, recording over 1,600 issuances in January. This is followed by Chinese tech stocks such as Alibaba (163 products), Tencent (143), Xiaomi (76), and Baidu (65).

By average daily turnover, Hang Seng Index-linked CBBCs accounted for over 93% of this product’s overall turnover in January, according to HKEX’s data.

Looking at unlisted products, Nvidia maintained the most-used underlying for ELIs sold in January, gathering over 2,400 issuances. Around 60% of the issuances were in a basket of stock structures, alongside other semiconductor-focused stocks like Advanced Micro Devices and Broadcom.

These ELIs are most commonly structured as autocallable reverse convertibles or autocallable barrier reverse convertibles. There were also 21 Nvidia-exposed worst-of products featuring uncapped participation, and one of which featured partial principal protection.

The US chipmaker’s stock was also the most-used underlying for ELIs’ single stock structures, 972 products. This is followed by Alibaba (H Shares) (650), HSBC (H Shares) (184), and Meituan (180).

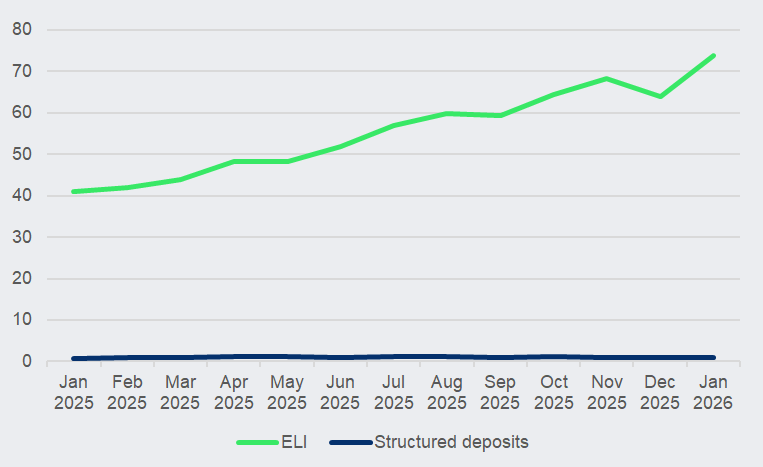

Data from the Securities and Futures Commission shows that the outstanding notional of the city’s ELIs reached nearly HK$74 billion by the end of January, soaring 80% YoY.

Hong Kong SAR: ELI’s net notional amount in outstanding (HK$ billion)

Source: Securities and Futures Commission

Meanwhile, the outstanding notional for structured deposits rose 18% YoY to HK$930m by the end of January. During the month, FX rates continued to gain traction as the top asset class for structured deposit issuances, led by the AUD/USD pair, which logged 799 issuances.

The GBP/USD (263), USD/CAD (224), and USD/CNH (208) pairs were also popular assets.

Issuers

J.P. Morgan led both DWs and CBBCs’ issuances in January, listing 162 warrants and 410 CBBCs, respectively.

Bank of China International Asia (BOCI Asia) and Huatai also followed closely on the warrant front, with each Chinese issuer listing 119 and 115 DWs, respectively.

Hong Kong SAR: top 5 DW and CBBC issuers by number of issuances in January 2026

| DWs | Product issuances | CBBCs | Product issuances |

| J.P. Morgan | 162 | J.P. Morgan | 410 |

| Bank of China International Asia | 119 | UBS | 400 |

| Huatai Financial Holdings (Hong Kong) | 115 | Société Générale | 367 |

| Morgan Stanley | 106 | HSBC Bank | 338 |

| HSBC Bank | 97 | BNP Paribas | 273 |

Source: SRP

UBS and Société Générale were among the CBBC top issuers by number of issuances, listing 400 and 367 products, respectively.

HSBC led the league table for ELIs, with over 4,400 issuances during the month, while Hang Seng Bank issued the most structured deposits among its peers, logging 897 products sold to the city’s retail segment.

Looking ahead

SRP database recorded over 4,900 ELIs and 2,100 structured deposits that expired in February.

Fears over a growing artificial intelligence bubble have kept markets buzzing. Structured product market participants in Asia showed a split when speaking with SRP in January, with some exploring tactical strategies to navigate rising valuations in Wall Street’s AI-exposed companies, while others emphasised diversification to manage short-term volatility.

Image/Adobe Stock

Do you have a confidential story, tip or comment you’d like to share? Contact Us | SRP (structuredretailproducts.com)

Disclaimer: While SRP's aim is to provide accurate and up-to-date information, the data provided is gathered from third parties. SRP does not take responsibility for the accuracy of the data and will not be held liable for any errors or omissions contained in the information provided. The information and data included on SRP's market reports uses sources believed to be reliable. SRP assumes no liability or responsibility for the quality, content, accuracy or completeness of the information, text, graphics, links, and any other items contained on this report.