Model used for hedging the products was not sufficient enough under current market conditions

Natixis has set €160 million aside to cover losses from managing ‘specific products traded with clients in Asia’ in the fourth quarter of this year. The French investment bank did not elaborate on which ‘specific products’ but industry sources pointed to autocallable structures widely sold in South Korea.

Natixis has actively increased its market share since late last year in the Asian country – the largest structured products market globally – by partnering up with the Korea Exchange to develop new indices for autocallables and inventing a new payoff structure, known as ‘lizards'.

“Natixis has been particularly aggressive compared to other banks; it built up its book a lot quicker, so I think there is definitely an element of, maybe, expanding a bit too quickly,” said an equity derivatives strategist at a European bank in Hong Kong.

The question, now, is whether the amount is actually sufficient enough to cover the losses Natixis suffered since around June this year when both the Hang Seng China Enterprises Index (HSCEI) and Hang Seng Index (HSI) nose dived.

“It seems like a lot of the losses that they’ve announced were probably more of taking a one-off hit,” said the source. “I’m surprised by the scale of the provision, in particular. I think they are being very conservative in that respect.”

Apart from the €160 million that Natixis has set aside to cover its hedging losses, it also said the products with a deficient hedging strategy will result in a €100 million cut in Natixis’ net revenues in the fourth quarter.

“Bear in mind that [implied] volatility moves have not been huge. We haven’t had the necessary [implied] volatility moves in order to justify those losses,” said the banker.

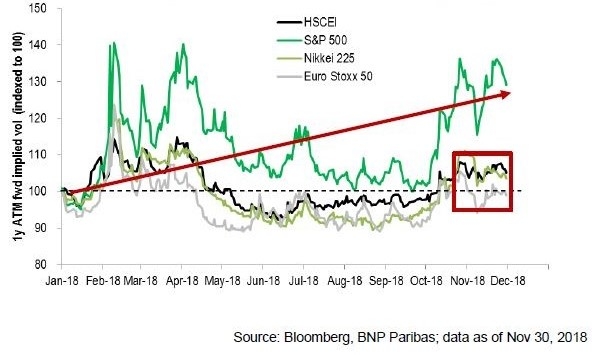

The one year at-the-money-forward implied volatilities of all HSCEI, Nikkei 225 and Eurostoxx 50 indices have been trading within a relatively tight range this year, while that of the S&P 500 rose over 20% during the same period, according to Asia equity and derivative strategy outlook for next year by BNP Paribas.

The report added the implied volatility moves remained subdued as derivative dealers were accumulating volatility inventory during market sell-offs.

Autocallables in South Korea generally track the worst performance of two or more equity indices and have a three-year tenor. The HSCEI and HSI are benchmarks that are typically included in the index basket because of their volatility.

After dropping sharply in June this year, both the HSI and HSCEI have kept a downward trend, resulting in many products linked to the indices missing their upside barriers or so-called ‘knock-out’ levels. The structure of autocallables, which involves an upside and a downside barrier, enables the investment to be automatically redeemed, or the product to mature, when the underlying asset of the product touches the barrier.

While investors will rack in coupons and banks will see higher revenues on the back of investors entering into new products with their redeemed investments once the upside barrier is breached, they may lose the principal if the lower barrier is breached.

Lizard autocallables has another layer of barriers apart from the upside and downside during the tenor of the product. Given that the 2015 equity market crash in Asia is still fresh in investors’ mind, the lizard payoff structure which offers additional safety in exchange for lower coupon has seen grown in popularity in South Korea.

The 40% drop in the Hang Seng China Enterprises Index (HSCEI) from its peak three years ago triggered the products to touch the lower barrier.